- Indonesia and India emerge as the world’s next aluminium growth hubs

- China shifts from expanding domestic capacity to exporting capital and technology

- Secondary aluminium becomes the industry’s fastest-growing source of new supply

Data Deep Dive: The global aluminium industry is entering its most significant structural transition in more than two decades. For much of the past 20 years, supply growth was driven by China’s rapid smelter expansion, abundant coal-fired electricity and rising domestic demand. That model is now approaching its limits. China’s primary aluminium capacity has effectively reached its government-imposed ceiling of 45 million tonnes (mnt), forcing producers to look beyond its borders for future growth.

The next supply cycle will therefore be shaped by a fundamentally different set of forces. Production capacity is shifting towards Indonesia and India, secondary aluminium is becoming the largest source of incremental supply, and electricity rather than bauxite is emerging as the industry’s principal constraint. At the same time, carbon regulations and higher operating costs are steadily reshaping the economics of aluminium production, making the next decade less about expanding volumes and more about securing reliable, competitive energy.

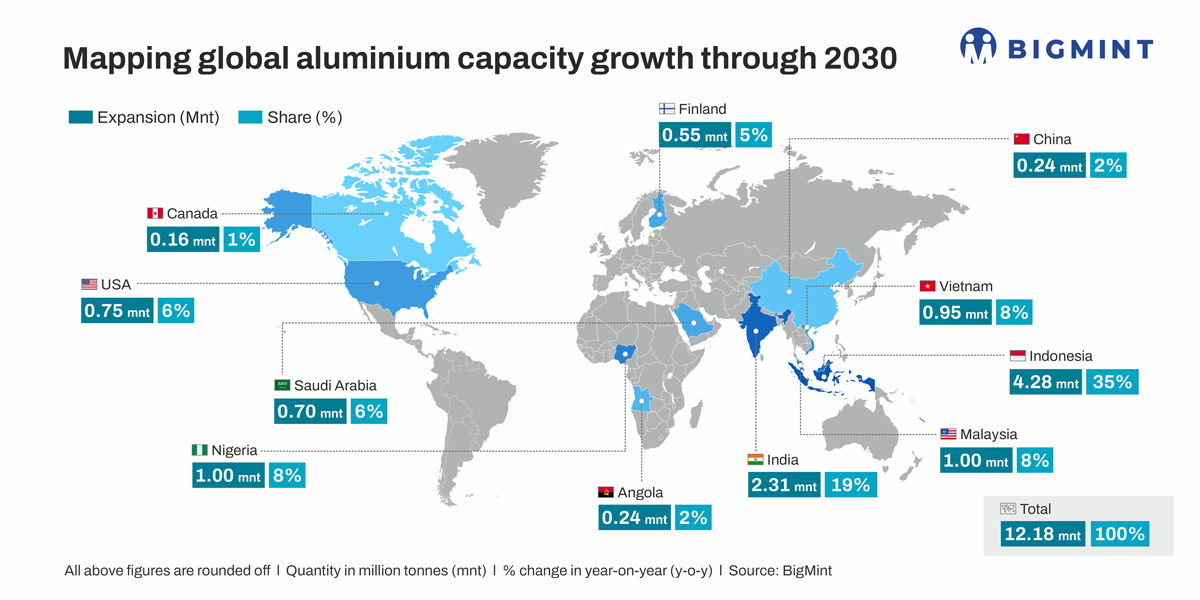

Global producers have announced around 12.2 mnt of new primary aluminium capacity through 2030. Unlike previous investment cycles, however, the pipeline is concentrated in only a handful of countries. Indonesia alone accounts for approximately 4.28 mnt, or 35%, of announced capacity additions, while India contributes another 2.31 mnt, representing 19% of the global pipeline. Together, the two countries account for more than half of all identified primary aluminium expansion, signalling an increasingly concentrated supply landscape.

Asia represents nearly 78% of announced capacity additions, reinforcing its position as the centre of gravity for global aluminium production. New projects in Malaysia, Vietnam and the Middle East complement expansion plans in Indonesia and India, while Africa is gradually emerging as a longer-term investment destination through projects in Nigeria and Angola. By contrast, capacity additions across Europe and North America remain limited, constrained by high energy costs, environmental regulations and ageing smelting infrastructure.

China exports its aluminium industry

China’s influence over the aluminium market is unlikely to diminish simply because domestic capacity growth has slowed. Instead, the country’s role is evolving from expanding production at home to exporting capital, technology and industrial expertise overseas.

Many of Indonesia’s largest aluminium developments already involve Chinese participation through financing, engineering partnerships and integrated industrial parks. Rather than building new smelters within China, producers are increasingly relocating capital-intensive operations to countries offering cheaper electricity, abundant mineral resources and more favourable industrial policies.

Chinese producers are therefore maintaining their influence over global aluminium supply chains without breaching domestic production limits. The country’s aluminium industry is becoming increasingly international even as domestic primary production plateaus.

Indonesia’s current primary aluminium production stands at less than 1 mnt annually, but announced projects could lift capacity to around 3.5 mnt over the coming years, placing the country among the world’s largest producers. Much of this investment is closely aligned with Indonesia’s downstream strategy of processing domestic mineral resources rather than exporting raw materials.

India is pursuing a markedly different expansion strategy. Instead of relying primarily on large greenfield developments, domestic producers are focusing on phased brownfield expansions built around existing alumina refineries, captive power assets and integrated production facilities. The approach lowers execution risk while strengthening India’s position as one of the few countries capable of meaningfully increasing primary aluminium output over the medium term.

Secondary aluminium moves to centre stage

Global secondary aluminium production is forecast to expand by approximately 9.1 mnt by 2030, with China accounting for nearly 6.1 mnt of that increase. As manufacturing scrap availability improves and end-of-life material becomes more accessible, recycled metal is expected to account for an increasingly larger share of future aluminium supply growth, even as industry attention remains focused on primary smelting.

Producing secondary aluminium requires only a fraction of the energy consumed by primary smelting, substantially lowering both production costs and carbon emissions. Rising electricity prices and tightening environmental regulations are therefore making recycled aluminium an increasingly attractive route to expanding supply without incurring the enormous capital and energy requirements associated with new smelters.

Governments are also increasingly treating aluminium scrap as a strategic raw material rather than simply another traded commodity. A growing number of countries have introduced or are considering export restrictions to retain scrap for domestic recycling industries, tightening global scrap availability and increasing procurement risks for scrap-import-dependent producers. Securing access to domestic scrap streams is therefore becoming an increasingly important competitive advantage alongside access to low-cost electricity.

Demand from electric vehicles, renewable energy infrastructure, aerospace and power transmission, however, continues to require high-quality primary metal that recycled aluminium alone cannot fully replace. The industry is therefore entering a period in which primary and secondary aluminium will become increasingly complementary rather than competing sources of supply.

Electricity becomes industry’s new bottleneck

More than 12.2 mnt of primary aluminium capacity has been announced globally through 2030, but translating those projects into operating smelters will require an unprecedented expansion of power generation and transmission infrastructure, particularly across emerging Asia. Access to bauxite is no longer the principal constraint on aluminium expansion. Access to abundant, reliable and competitively priced electricity increasingly is.

Globally competitive aluminium smelters generally require electricity prices of around $40/MWh, a threshold that is becoming increasingly difficult to sustain as electricity itself emerges as a scarce industrial resource. Reliable baseload power, once regarded as a prerequisite for aluminium production, is now a strategic asset as governments and utilities balance competing demands from industry, electrification and digital infrastructure.

Artificial intelligence and hyperscale data centres are increasingly willing to pay well above $100/MWh to secure uninterrupted electricity, substantially exceeding the level at which aluminium smelters remain internationally competitive. Utilities and independent power producers therefore have a growing commercial incentive to allocate new generation capacity towards customers capable of generating significantly higher returns, intensifying competition for affordable industrial power.

Every $10/MWh increase in electricity prices raises aluminium production costs by an estimated $125-150/t, contributing to a rise in the industry’s weighted average cash cost from around $1,600/t in 2014 to more than $2,050/t in 2025. Higher electricity prices, rising capital expenditure and tighter environmental standards are permanently resetting the global aluminium cost curve rather than creating another cyclical increase in operating costs.

Government and industry plans envisage as much as 14.9 mnt of primary aluminium capacity in Indonesia over the longer term, yet achieving that ambition would require an estimated 24 GW of dedicated electricity generation, equivalent to roughly 22% of the country’s installed generating capacity in 2025.

Every large aluminium project now requires parallel investment in power stations, transmission networks, ports and industrial infrastructure, substantially increasing capital requirements and extending commissioning timelines.

Future aluminium supply will increasingly depend on how quickly producing countries can expand reliable, competitively priced electricity generation rather than on the volume of announced smelting projects. Access to affordable power has become the industry’s principal competitive advantage, suggesting that the next aluminium superpower will be determined as much by its energy infrastructure as by its mineral resources.

Carbon regulation reshapes competitiveness

Access to cheap electricity alone will no longer guarantee competitiveness as carbon policies begin reshaping international aluminium trade. Carbon policy is increasingly influencing where aluminium can be sold and how much producers ultimately receive for their metal.

The European Union’s Carbon Border Adjustment Mechanism (CBAM) represents one of the most significant structural changes facing the industry. Producers supplying carbon-intensive aluminium into Europe could face additional costs estimated at $150-230/t, depending on embedded emissions and prevailing carbon prices. Although CBAM is often viewed primarily as an environmental policy, its commercial implications are equally significant.

Rather than simply raising costs, carbon regulation is beginning to differentiate aluminium according to its production footprint. Metal produced using hydroelectricity, renewable energy or low-carbon grids is likely to command an increasing premium in markets with stringent environmental requirements, while coal-based production may become increasingly concentrated in regions where affordability remains a higher priority than emissions.

This suggests the industry may gradually move away from a single global aluminium market towards parallel regional markets with different cost structures, customer preferences and pricing mechanisms. Low-carbon aluminium will increasingly target Europe and other premium markets, while conventional metal continues supplying much of Asia, the Middle East and Africa.

Outlook

The aluminium industry is entering a fundamentally different growth cycle from the one that transformed global supply over the past two decades. Future expansion will be concentrated in a smaller number of countries, led by Indonesia and India, while recycled aluminium assumes an increasingly important role in meeting incremental demand. China’s influence will persist, not through unlimited domestic capacity growth, but through overseas investment, technology and integrated industrial supply chains.

Yet the defining constraint on the industry’s future is unlikely to be bauxite availability, alumina capacity or even capital. It will be electricity.

As artificial intelligence infrastructure, electrification and industrial demand compete for the same power resources, access to affordable and reliable electricity is becoming a strategic advantage in its own right. Producers capable of securing long-term, low-cost energy are likely to enjoy an increasingly durable competitive edge, while higher-cost operations face mounting pressure from rising input costs and carbon regulation.

For aluminium consumers, these structural shifts suggest that the era of abundant low-cost supply is drawing to a close. Although periodic cyclical corrections will continue, the industry’s long-term cost base appears set to remain structurally higher than in the previous decade.

Leave a Reply