- Tight availability keeps aluminium market sentiment firm

- Limited supply may cap further price declines

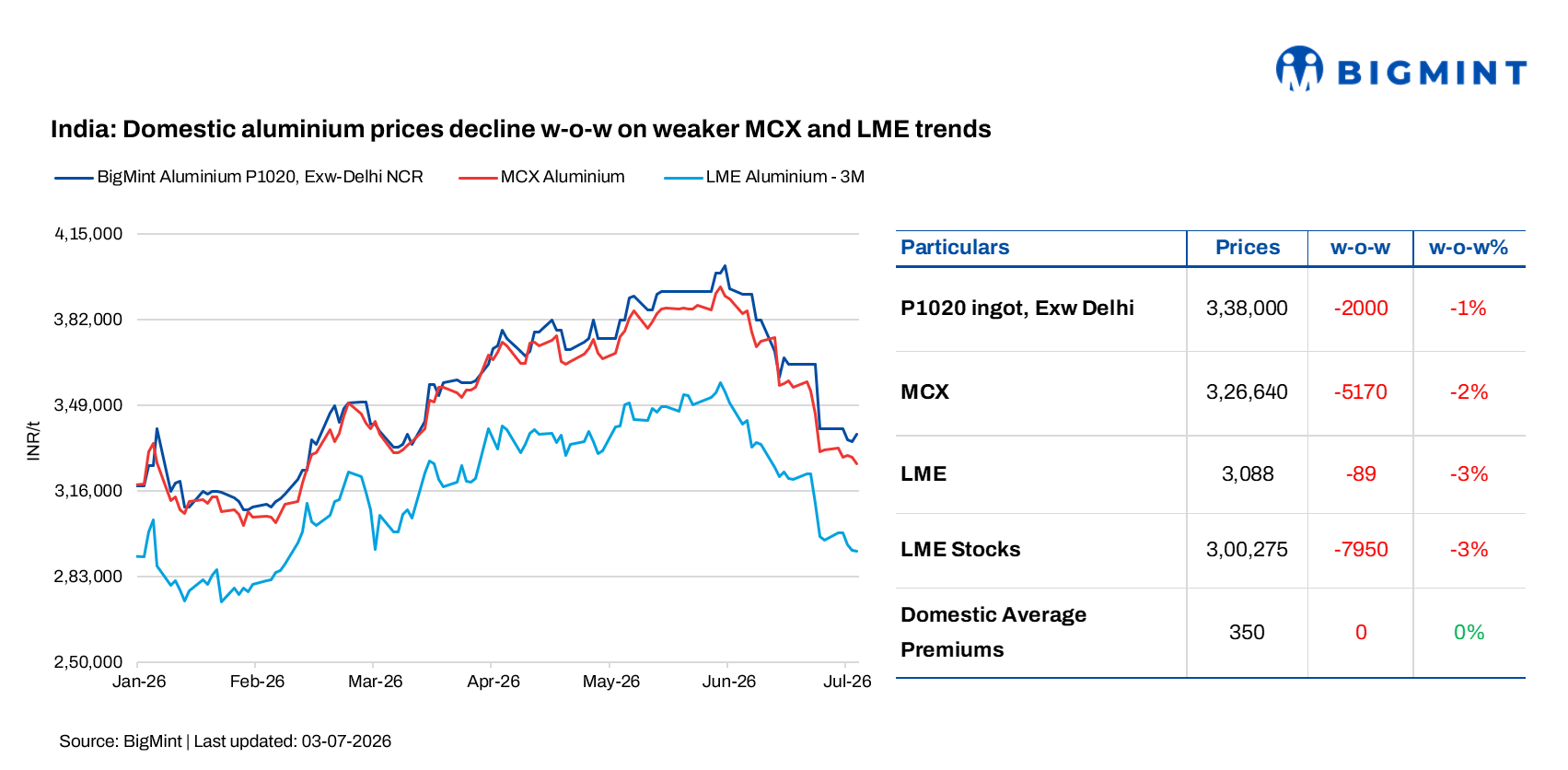

Domestic aluminium prices in India eased marginally w-o-w as of 3 July 2026, tracking weaker trends on both the Multi Commodity Exchange (MCX) and the London Metal Exchange (LME).

According to BigMint’s assessments, P1020 aluminium ingot prices in Delhi NCR fell by INR 2,000/t (1%) w-o-w to INR 338,000/t on 3 July from INR 340,000/t on 26 June. Similarly, ex-Mumbai P1020 aluminium ingot prices declined by INR 1,000/t to INR 339,000/t on 3 July from INR 340,000/t on 26 June.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX declined by INR 5,170/t, or 2%, w-o-w to INR 326,640/t on the latest assessment from INR 331,810/t in the previous week.

Similarly, three-month aluminium prices on the LME fell by $89/t, or 3%, to $3,088/t from $3,177/t. Meanwhile, LME aluminium stocks declined by 7,950 t, or 3%, to 300,275 t from 308,225 t during the same period.

LME aluminium prices declined w-o-w as easing geopolitical tensions in the Middle East reduced the supply risk premium that had supported prices in recent weeks. Improving expectations for aluminium shipments from key Gulf producers, coupled with a stronger US dollar, weighed on investor sentiment and triggered profit-booking, pushing the three-month contract to its lowest level in nearly three months.

Market updates

India’s P1020 aluminium market remains supported by persistent physical tightness despite a recent correction in LME prices.

Current domestic premiums are largely aligned with the QMJP benchmark, hovering around $350/t, as lower LME prices have encouraged buyers to place spot orders and replenish inventories.

While the monsoon season is typically associated with softer demand across several end-use sectors, market participants report improved spot buying activity as consumers seek to capitalize on the recent decline in benchmark prices. This has helped maintain market liquidity despite seasonally weaker consumption trends.

On the supply side, physical metal availability continues to remain constrained. Market sources indicate that some participants have oversold volumes despite ongoing tightness, reinforcing concerns over near-term supply adequacy. As a result, import material, which is generally traded at a discount to prevailing domestic benchmarks, is currently being sold at parity with QMJP levels, reflecting the deficit conditions in the market. Consequently, import parity is estimated to be around QMJP levels at present.

Looking ahead, sentiment remains constructive, with several market participants expecting aluminium prices to recover toward the $3,400/t level

The expectation is primarily driven by continued physical tightness, limited spot availability, and a still-challenging scrap supply environment.

Meanwhile, BALCO recorded a 5% w-o-w decline, with average prices falling to INR 361,542/t from INR 378,708/t. Similarly, Hindalco prices declined by 2% w-o-w to INR 360,167/t from INR 367,750/t during the same period.

Outlook

Despite the recent price correction, the domestic aluminium market is expected to remain fundamentally supported by tight physical availability, steady spot buying, and constrained scrap supply. While monsoon-related demand softness may limit any sharp upside in the near term, a recovery in LME aluminium prices and sustained supply tightness could help domestic prices stabilise and gradually regain lost ground over the coming weeks.

Leave a Reply