- Canada, South African, Chile witness rise in shipments

- Panamax and Supramax outperform weaker Capesize segment

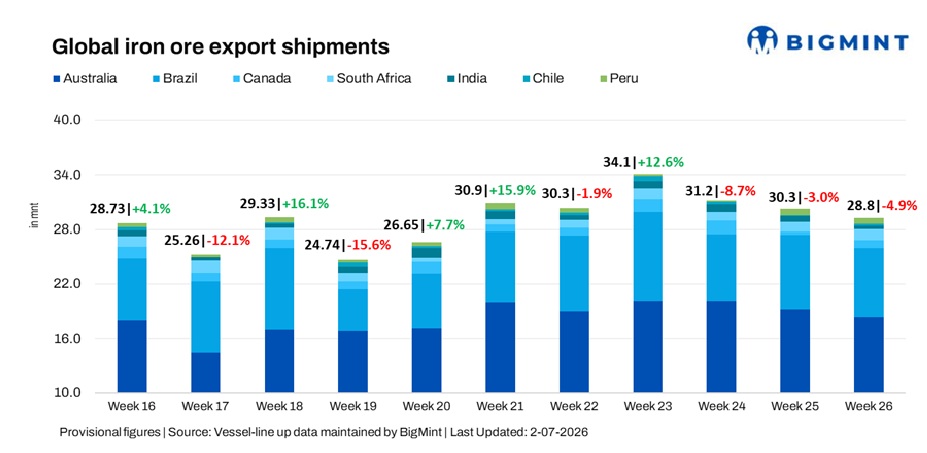

Global iron ore export shipments declined 4.9% w-o-w to 28.8 million tonnes (mnt) in the week ended 26 June, marking a third consecutive weekly decline, according to BigMint data.

Weaker shipments from Australia, Brazil, India and Peru outweighed stronger cargo flows from Canada, South Africa and Chile. Australia remained the largest exporter despite softer Pilbara loadings, while Brazil’s exports eased amid weaker Vale loading programmes and lower activity at key export terminals.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 11.1 mnt, followed by Port Walcott (4.1 mnt) and Dampier (2.5 mnt). Rio Tinto exported 6.6 mnt, followed by BHP (6.0 mnt) and FMG (3.9 mnt). China remained the largest importer at 13.9 mnt, followed by South Korea (2.4 mnt) and Japan (0.8 mnt).

- Brazil: Ponta da Madeira handled 2.2 mnt, followed by Tubarao (1.8 mnt) and Itaguai (1.5 mnt). CSN exported 3.3 mnt, followed by Vale (3.1 mnt). China remained the largest importer at 3.8 mnt.

- Canada: Port Cartier handled 0.5 mnt, followed by Sept-Iles (0.4 mnt). AMNS exported 0.5 mnt, while IOC shipped 0.3 mnt. The Netherlands remained the largest importer at 0.3 mnt.

- South Africa: Saldanha handled 1.2 mnt, with China importing 0.2 mnt.

- India: Paradip handled 0.2 mnt. Rungta Sons exported 0.1 mnt, while China remained the largest importer at 0.1 mnt.

- Chile: Totoralillo handled 0.2 mnt, with China importing the entire volume.

- Peru: San Nicolas handled 0.2 mnt. Shougang Hierro exported 0.2 mnt, with China importing the entire volume.

Freight market remains mixed

The dry bulk freight market remained mixed as the Capesize segment stayed under pressure from softer Pacific cargo demand, limited iron ore enquiries and ample vessel availability. Weaker Pilbara loading programmes further weighed on sentiment, while softer Brazilian cargo volumes offered limited support to Atlantic activity.

Panamax and Supramax markets remained comparatively resilient, supported by steady Atlantic cargo demand and healthy minor bulk activity.

Outlook

Global iron ore shipments are expected to remain mixed as loading programmes in Australia and Brazil, South Africa’s rail performance and Chinese steel demand continue to influence seaborne trade. Freight sentiment is likely to stay divided, with Capesize rates dependent on fresh cargo enquiries, while Panamax and Supramax segments are expected to remain relatively supported.

Leave a Reply