- Buyers continue to procure material only against immediate requirements

- Finished secondary zinc prices decline even as Tukdi scrap prices edge higher

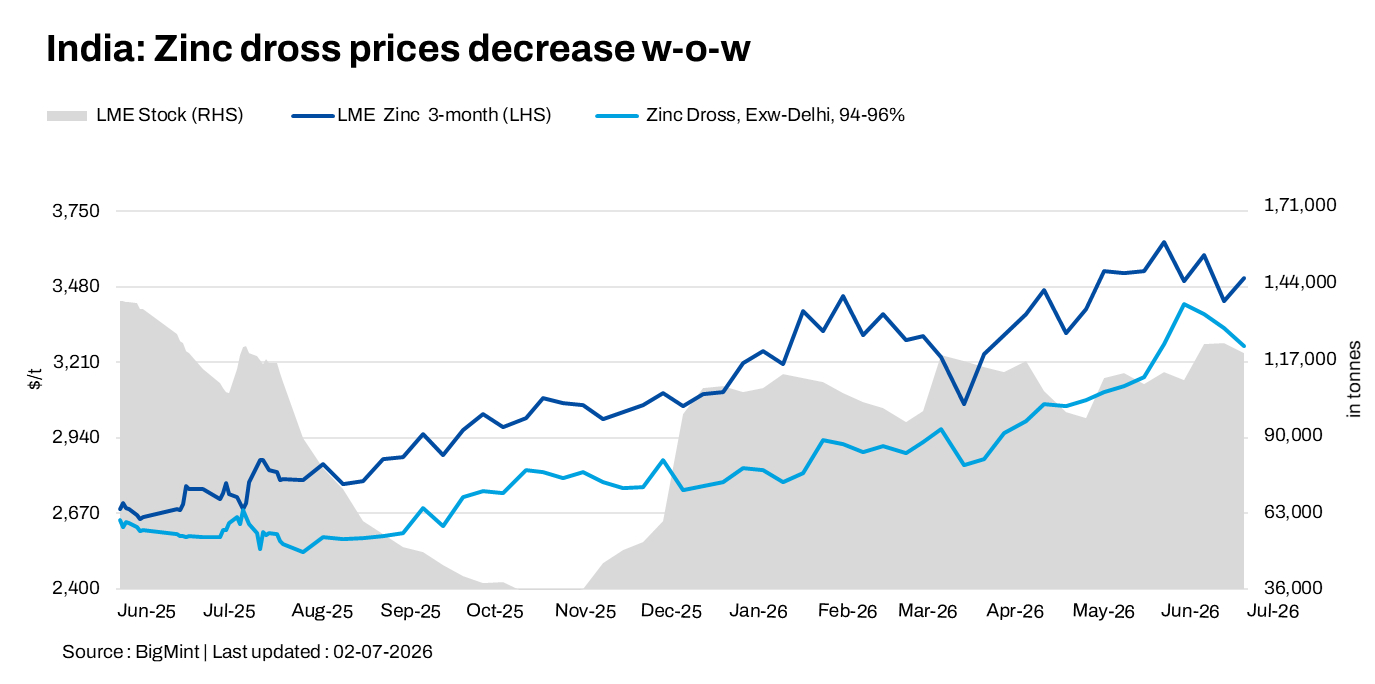

India’s zinc dross and zinc oxide prices declined further w-o-w as of 1 July 2026, tracking weaker London Metal Exchange (LME) zinc prices and subdued downstream procurement. Market activity remained largely need-based, with consumers restricting purchases to immediate production requirements amid cautious demand visibility.

Benchmark three-month LME zinc prices averaged around $3,473/t during the assessment week ended 1 July, compared with approximately $3,553/t in the previous week. Meanwhile, LME zinc inventories declined to 119,200 t on 1 July from 122,825 t recorded on 24 June, reflecting continued warehouse drawdowns.

The sharp correction in LME zinc during the assessment period weighed on replacement costs and kept domestic secondary zinc prices under pressure. Procurement activity remained measured, with most transactions concluded only against confirmed orders.

Zinc dross, oxide price movements

Domestic zinc dross prices declined by around INR 2,800/t w-o-w to INR 310,400/t ex-Delhi from INR 313,200/t a week earlier.

Meanwhile, zinc oxide (99% Zn) prices fell by around INR 3,900/t w-o-w to INR 300,300/t ex-Delhi, compared with INR 304,200/t in the previous week.

The decline reflected lower replacement costs following the correction in international zinc prices, while downstream procurement remained largely aligned with immediate production requirements.

Scrap segment trends

In the north Indian zinc scrap market, regular-grade Tukdi was heard at around INR 301,000-302,000/t ex-Delhi, marginally higher than INR 300,000-301,000/t a week earlier. Small-sized Tukdi was assessed at INR 299,000-300,000/t, compared with INR 298,000-299,000/t in the previous week.

Despite the decline in finished secondary zinc products, scrap values edged up slightly during the assessment period, indicating steady procurement by processors and balanced material availability.

Market sentiments

The domestic secondary zinc market maintained a cautious tone during the week as lower LME zinc prices continued to influence replacement costs. Consumers largely refrained from inventory building and continued purchasing material only to meet immediate production requirements.

Trading activity remained moderate, with transactions taking place at prevailing market levels. The divergence between softer finished secondary zinc prices and slightly firmer scrap values kept processing margins under pressure during the assessment period.

Outlook

In the near term, zinc dross and zinc oxide prices are expected to remain stable to slightly weaker, depending on the direction of LME zinc prices and domestic procurement activity. While lower exchange inventories may provide some support to global prices, cautious downstream buying and the absence of inventory accumulation are likely to limit any significant recovery in the domestic secondary zinc market.

Leave a Reply