- Five-year duties proposed to offset injury to domestic producers

- Malaysia emerges as most aggressive pricing source

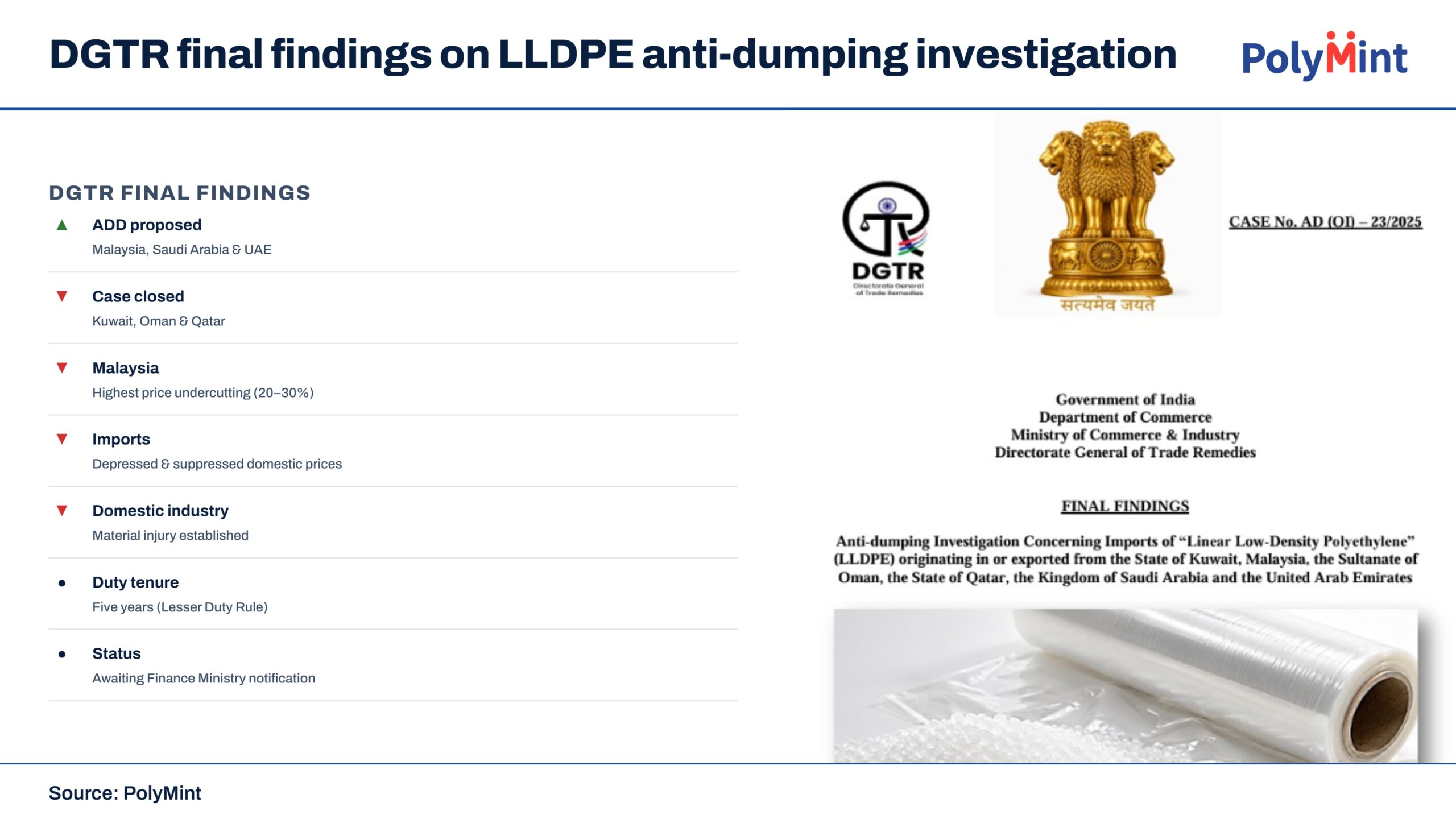

The Directorate General of Trade Remedies (DGTR) has issued its final findings in the anti-dumping investigation concerning imports of Linear Low-Density Polyethylene (LLDPE), recommending anti-dumping duties on imports originating in or exported from Malaysia, Saudi Arabia and the United Arab Emirates (UAE).

The DGTR has terminated the investigation against Kuwait, Oman and Qatar under Rule 14 of the Anti-Dumping Rules, 1995. The recommendations have been forwarded to the Central Government, which will take the final decision on the imposition of duties through a customs notification.

The investigation was initiated following an application filed by the Chemicals and Petrochemicals Association of India (CPMA) on behalf of Haldia Petrochemicals Ltd. (HPL) and HPCL-Mittal Energy Ltd. (HMEL), supported by Reliance Industries Ltd. The investigation covered imports during 1 January-31 December 2024, while the injury assessment covered FY2021-22, FY2022-23, FY2023-24 and the period of investigation.

Scope of investigation

The product under consideration comprises Linear Low-Density Polyethylene (LLDPE) having a density of 908.4-940.4 kg/m³, primarily classified under HS Codes 3901 10 10 and 3901 40 10.

During the investigation, exporters requested exclusion of several specialised grades, including C8-based LLDPE, Higher Alpha Olefin (HAO) grades, powder-form LLDPE, Borstar bimodal grades and certain high-performance grades. After examining technical submissions, product specifications and evidence submitted by both exporters and domestic producers, DGTR rejected all major exclusion requests.

The Authority concluded that imported and domestically manufactured products possess closely resembling physical and chemical characteristics, are technically and commercially substitutable, and therefore qualify as “like articles” under the Anti-Dumping Rules. It also retained separate Product Control Numbers (PCNs) for Metallocene and Non-Metallocene grades to account for pricing differences observed during the investigation.

Domestic industry standing

Several exporters challenged the standing of the domestic industry, arguing that other Indian producers, including SEZ-based manufacturers, should have been included while determining industry representation.

After examining these submissions, DGTR held that the application satisfied the requirements prescribed under the Anti-Dumping Rules and proceeded with the investigation using verified information submitted by the participating domestic producers.

Dumping and injury findings

DGTR concluded that dumping margins and injury margins for exporters from Malaysia, Saudi Arabia and the UAE were positive and significant. In contrast, the investigation against Kuwait, Oman and Qatar was terminated.

DGTR found that dumped imports caused material injury to the domestic industry through both volume and price effects.

Price undercutting

DGTR’s analysis showed considerable variation across exporting countries. Malaysia recorded the deepest price undercutting, with a weighted average landed value of INR 78,860/t, undercutting the domestic industry’s net sales realisation by 20-30%.

Imports from the UAE recorded a weighted average landed value of INR 93,659/t, resulting in 0-10% price undercutting. Saudi Arabian imports averaged INR 97,871/t, with price undercutting in the (10)-0% range, indicating prices broadly at par with or marginally above domestic selling prices.

Overall, imports from the subject countries recorded a weighted average landed value of INR 94,075/t, with aggregate price undercutting in the 0-5% range. Beyond price undercutting, DGTR found that dumped imports also depressed and suppressed domestic prices, preventing producers from recovering rising costs despite healthy demand.

Performance of domestic industry

Although India’s LLDPE demand increased during the injury period and the domestic industry expanded installed capacity, the Authority found that a significant portion of available capacity remained idle during the period of investigation.

Production and sales volumes improved following commencement of production by HMEL; however, DGTR noted that this improvement did not offset the deterioration in financial performance. The overall market share of the Indian industry declined, while imported material continued exerting pricing pressure.

The domestic industry:

- incurred financial losses during the investigation period;

- reported cash losses;

- earned negative returns on capital employed;

- failed to earn reasonable returns despite growing domestic demand; and

- experienced deterioration in profitability because of dumped imports.

Causal link

DGTR carried out a non-attribution analysis to determine whether factors other than dumped imports were responsible for the injury.

The Authority concluded that no other known factors—including demand conditions or other market developments—were responsible for the deterioration in the domestic industry’s performance. It established a direct causal link between dumped imports and the material injury suffered by domestic producers.

Public interest assessment

DGTR also evaluated the likely impact of anti-dumping duties on downstream users and the broader public interest.

The Authority observed that no interested party had demonstrated that imposing duties would result in disproportionate adverse consequences. It further noted that anti-dumping duties are intended to restore fair competition rather than restrict imports. Imports may continue provided they enter India at fair, non-dumped prices.

Duty recommendation

Considering the positive dumping and injury margins, DGTR recommended imposition of anti-dumping duties for five years under the lesser duty rule, whereby the applicable duty equals the lower of the dumping margin and injury margin required to remove injury to the domestic industry.

The duty table prescribes producer-specific duties. The visible recommendations include anti-dumping duties of US$75/t for the following Saudi Arabian producers:

Producer recommended duty

- Al-Jubail Petrochemical Company (KEMYA) US$75/t

- Arabian Petrochemical Company (Petrokemya) US$75/t

- Eastern Petrochemical Company (Sharq) US$75/t

- Jubail United Petrochemical Company US$75/t

The recommendation also contains producer-specific duty rates for exporters from Malaysia and the UAE, applicable from the date of notification by the Central Government for a period of five years.

Market implications

The findings are expected to improve the competitive position of domestic LLDPE producers by reducing the pricing advantage of dumped imports from Malaysia, Saudi Arabia and the UAE.

Among the three countries, Malaysian suppliers are likely to face the greatest impact, reflecting the Authority’s finding of 20-30% price undercutting. The recommendations may alter procurement strategies for importers and downstream plastic processors, particularly those dependent on material from the affected countries. Buyers could increasingly evaluate alternative sourcing origins or domestic suppliers once the Ministry of Finance notifies the duties.

For domestic producers, the measures are expected to support improved price realisation and capacity utilisation by addressing unfair pricing practices rather than restricting legitimate imports.

What next?

DGTR’s findings are recommendatory. Anti-dumping duties will become effective only after the Ministry of Finance issues a customs notification accepting the Authority’s recommendations. If notified, the duties will remain in force for five years, unless modified or reviewed earlier under the Anti-Dumping Rules.

Leave a Reply