- Soft cargo demand drags Capesize freight lower

- Atlantic subdued, Pacific cargo volumes disappoint

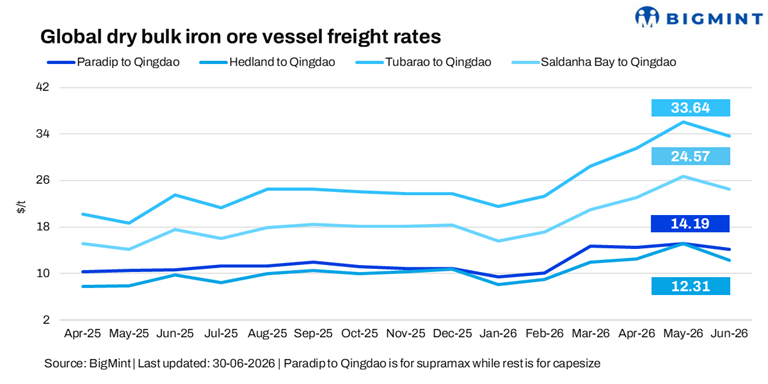

Dry bulk iron ore freight sentiment remained under pressure on 30 June. Market activity remained sluggish due to limited fresh Pacific cargoes, while forward laycans reflected a lack of urgency among charterers. Bearish sentiment persisted across both basins amid weak physical market fundamentals.

A shipbroker stated, “The dry bulk market remains mixed, with Capesize sentiment weakening on subdued demand, while Panamax is showing initial signs of recovery. Supramax continues to face mild pressure, whereas the Handysize segment remains resilient, supported by steady cargo demand.”

Capesize freight sentiment remained weak during the week, with rates declining across all major iron ore routes amid sluggish cargo demand and ample vessel availability. Limited fresh cargo enquiries and subdued Chinese iron ore demand kept chartering activity muted, while bearish sentiment across both the Atlantic and Pacific basins continued to pressure freight rates.

In the Pacific, subdued iron ore demand and limited prompt cargo availability weighed on the Hedland-Qingdao route. Meanwhile, in the Atlantic, rising ballaster supply for H2 July loadings and thin cargo volumes kept the Tubarao-Qingdao and Saldanha Bay-Qingdao routes under pressure, as increased vessel competition continued to weigh on fixture levels.

Following the suite, Supramax freight sentiment remained slightly soft during the week, with limited fresh cargo enquiries and cautious chartering activity weighing on rates across key trading regions. “No shipments were reported over the past five days, as market participants cited an absence of genuine cargoes, with most enquiries considered non-firm”, a source told BigMint.

Route-wise update

Outlook

Near-term dry bulk iron ore freight rates are expected to remain under pressure amid ample vessel supply and subdued cargo demand. Although higher Brazilian exports may lend some support, weak Chinese steel demand and cautious chartering activity are likely to limit any significant recovery in Capesize rates.

Leave a Reply