- Monsoon restricts beaching activity but outlook remains positive

- Pakistan loses wartime freight advantage as Hormuz reopens

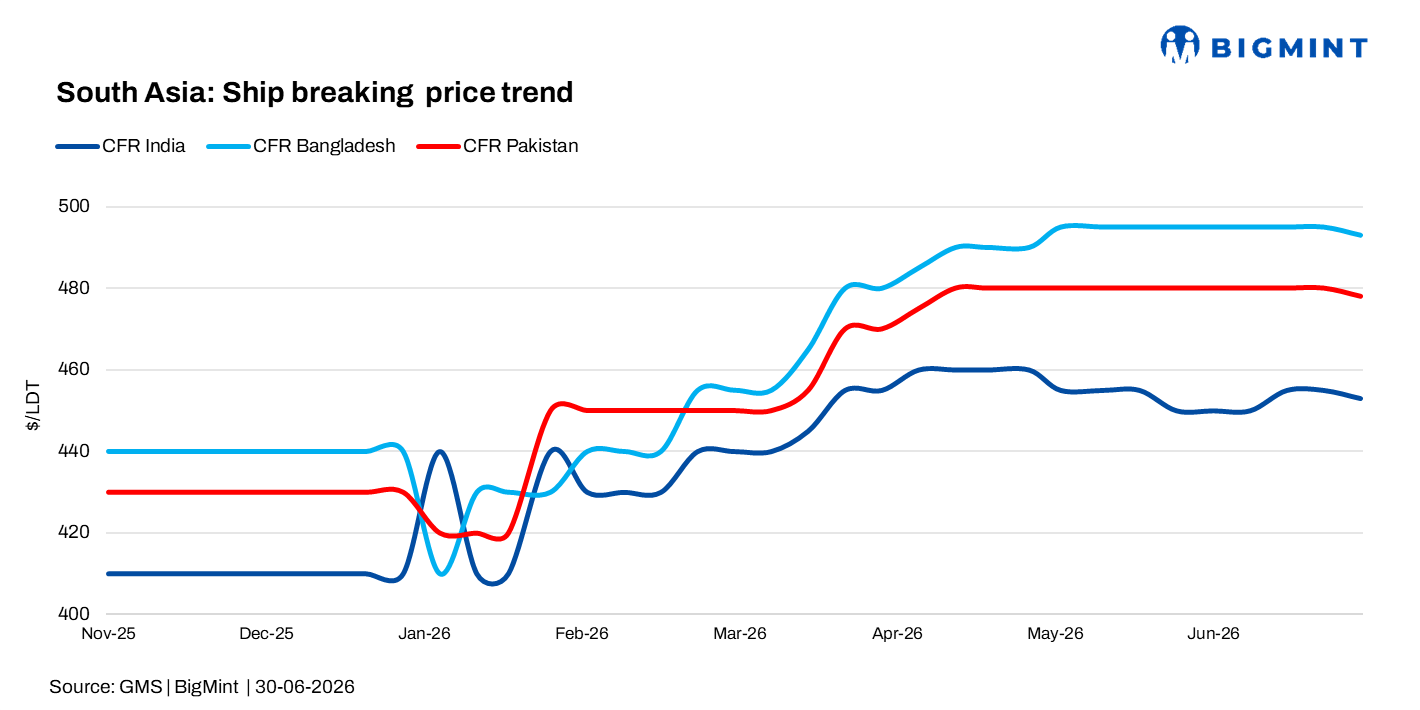

The South Asian ship recycling market entered Week 26 (22-26 June 2026) with improving fundamentals following the reopening of the Strait of Hormuz and easing geopolitical tensions in the Middle East. Lower crude oil prices, stabilising regional currencies, and the gradual return of deferred vessel supply supported market confidence, although monsoon conditions and holidays continued to limit near-term recycling activity.

Indian plate prices soften but stronger rupee sparks optimism

India’s ship recycling market remained subdued this week as monsoon conditions continued to restrict beaching activity and no fresh vessel arrivals were reported, with the last vessel beached being a 10,509-LDT passenger ship on 18 June. However, multiple deliveries during the previous fortnight, including the 41,478-LDT Octans tanker, indicate that deferred tonnage is gradually returning following the reopening of the Strait of Hormuz.

Domestic steel plate prices at Alang softened to INR 36,500-37,000/t ($387-392/t) as weaker global scrap sentiment outweighed currency gains. This has kept India the lowest-priced recycling destination in the Indian subcontinent.

However, India’s ship recycling market continued to benefit from lower international oil prices, with the rupee strengthening against the US dollar. Lower crude prices have eased pressure on the country’s import bill, while improving debt inflows have supported currency stability despite a stronger US dollar and continued foreign equity outflows. With strong yard capacity and regulatory compliance, India remains well positioned to capture higher recycling volumes once seasonal disruptions ease.

Bangladesh plate prices rise amid firm demand

Bangladesh’s ship recycling market remained largely quiet, with no market sales heard during the week as the Ashura holiday and monsoon conditions continued to slow beaching activity and cash-buyer interest. Despite the temporary slowdown, the market received its first post-conflict vessel, with the 9,369-LDT bulker Andhika Paramesti sold at $460/LDT on an as-is Sambu basis, signalling that deferred recycling candidates are beginning to re-enter the market.

Domestic steel plate prices increased to BDT 67,000/t ($543/t) from BDT 65,000/t ($527/t) a week earlier, supported by firm domestic demand. The first signs of delayed vessel supply also emerged, with a 9,369-LDT bulker reportedly sold at $460/LDT. With full yard availability, healthy letter of credit (LC) availability, and stable financing conditions, recyclers expect vessel arrivals to improve during the third quarter once seasonal disruptions ease. Stable foreign exchange reserves and lower oil prices continued to provide a supportive backdrop for the recycling sector. Stable foreign exchange reserves and lower oil prices continued to provide a supportive backdrop for the recycling sector.

Pakistan’s prices remain stable, highest in South Asia

Pakistan’s ship recycling market remained stable during the week, with three HKC-certified recycling yards continuing operations and the 21,502-LDT Ron progressing through Gadani. Domestic steel plate prices held at around PKR 195,000/t ($701/t), the highest among South Asian recycling destinations.

However, the reopening of the Strait of Hormuz has reduced the freight advantage Gadani enjoyed during the regional conflict, shifting competition back toward pricing and environmental compliance. As deferred vessel supply gradually returns to the market, participants expect future allocations to depend increasingly on recyclers’ commercial competitiveness rather than wartime logistics. Lower oil prices and a stronger rupee continued to support market stability but were secondary to evolving recycling fundamentals.

Leave a Reply