- Thermal coal inventories at Indian ports drop w-o-w

- Indonesia’s domestic obligations to state utility PLN continue to limit exports

Indian portside prices for Indonesian-origin thermal coal declined during the week ended 26 June 2026, as subdued buying interest and adequate domestic coal availability continued to weigh on imported coal demand.

Market participants indicated that “Indonesian exports have not been completely halted, miners are facing increased pressure to prioritise domestic supply commitments, particularly to state utility PLN.”

Premium-grade coal availability remained relatively comfortable, limiting upside potential despite supply-side concerns from Indonesia. The 5,000 GAR Indonesian coal prices remained stable week-on-week at around INR 11,000/t at Kandla and INR 10,900/t at Vizag, supported by steady demand for higher calorific value coal.

Meanwhile, 4,200 GAR coal prices witnessed a marginal correction of around INR 50/t, settling near INR 9,100/t at Kandla and INR 9,000/t at Vizag. Lower-calorific 3,400 GAR coal declined further by around INR 100/t to approximately INR 7,000/t at Navlakhi, reflecting weaker demand for lower-grade imported coal.

Freight rates ease on improved geopolitical sentiment

Freight rates for Supramax vessels from East Kalimantan to Navlakhi corrected sharply during the week, declining by around $1.2/t w-o-w to approximately $20.8/t. The decline was primarily driven by easing geopolitical tensions, particularly improving sentiment around US-Iran relations and expectations of a potential peace agreement, which reduced risk premiums in the freight market.

Lower freight costs provided some relief to delivered coal prices; however, weak spot demand and sufficient inventories limited any significant market recovery.

Rising port inventories reduce import buying appetite

India’s imported coal inventories at major ports increased by around 11.4% w-o-w to 15.07 million tonnes (mnt) during Week 25, compared with 14.72 mnt in Week 24. The inventory build-up was mainly due to higher vessel arrivals combined with slower evacuation at key ports.

With domestic coal availability remaining adequate and competitively priced, consumers continued to favour domestic supplies over imported coal, which remained comparatively expensive. This inventory accumulation has further reduced immediate procurement requirements from the seaborne market.

Global thermal coal prices remain under pressure

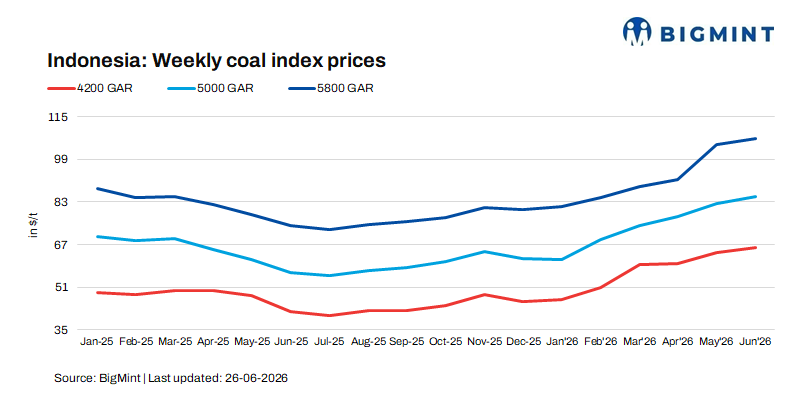

International thermal coal markets remained under pressure during the week, with Indonesian benchmarks declining across key grades. Indonesian 5,800 GAR coal prices decreased by approximately $1-2/t week-on-week, while 4,200 GAR prices also declined by around $1-2/t. Lower calorific value 3,400 GAR coal prices softened by nearly $0.5/t.

The weakness was attributed to muted demand from major buyers, particularly China and India, along with cautious purchasing behaviour amid sufficient inventories.

Indonesia domestic obligation tightens export availability

Indonesia’s thermal coal market continues to face supply allocation challenges as PLN focuses on securing sufficient coal volumes for power generation. Market sources indicated that PLN has been experiencing shortages of mid-CV coal availability at stockpiles due to reduced RKAB production quotas, stronger export economics compared with domestic pricing, and extended payment cycles impacting smaller miners.

To address the supply gap, the Indonesian government has directed major coal producers to prioritise prompt deliveries to PLN, especially for June requirements. Several producers are reportedly finalising additional domestic supply agreements, limiting spot export availability.

Although international export markets remain more attractive from a pricing perspective, domestic market obligations are absorbing a significant share of available production. Market participants also indicated that Indonesia may temporarily restrict certain export volumes to ensure sufficient coal availability for domestic power generation.

Outlook

The Indian imported thermal coal market is expected to remain subdued in the near term as high domestic coal availability, elevated port inventories, and cautious buying continue to restrict import demand. However, tighter export availability from Indonesia due to increased PLN commitments may provide support to higher-CV Indonesian coal grades.

Premium grades are likely to remain relatively stable, while lower-CV coal may continue facing pressure due to weaker demand and higher inventory levels. Freight corrections may provide limited downside support, but a meaningful price recovery is unlikely unless import demand improves or Indonesian supply restrictions intensify.

Overall, the market is expected to remain range-bound, with domestic supply dynamics in India and PLN-driven allocation priorities in Indonesia remaining the key factors influencing price direction.

Leave a Reply