- High Finished Steel Inventories Continue Pressuring Mill Prices

- Narrow Conversion Spread Impacts Steel Producers’ Profitability

Steel prices in the southern market continued to remain range-bound during the week, with no major changes observed in pricing levels.

Steel manufacturers have largely maintained their existing offers despite weak demand conditions, primarily due to limited conversion margins.

Sponge Iron & Melting scrap

Bellary sponge iron prices witnessed a marginal correction of around INR 200-300/t week-on-week (w-o-w) and were assessed at approximately INR 25,000/t as on 26 June 2026.

Prices remained under pressure in the merchant market as steel manufacturers were not accepting the prevailing sponge iron rates. On a month-on-month (m-o-m) basis, sponge iron prices have declined by nearly INR 700/t.

Trading activity in the merchant market remained limited during the week. Steel manufacturers showed low interest in booking fresh material due to weak demand for downstream steel products and liquidity constraints prevailing in the market.

During the week, around 10,000 tonnes of pellet-based DRI transactions were recorded. Sponge iron manufacturers in the Bellary region are currently operating at around 60-70% of their installed capacity, mainly due to poor conversion margins.

Bellary sponge iron producers are largely dependent on demand from nearby consumption centres such as Hyderabad, Chennai, Hindupur, and parts of Maharashtra. However, buyers in these regions are currently preferring material from competing markets due to more competitive pricing.

Meanwhile, Chennai HMS 80:20 scrap prices also witnessed a correction during the week as mills were unwilling to accept higher prices amid weak conversion margins.

As a result, HMS 80:20 prices were assessed at around INR 31,300/t FOR Chennai as of 26 June 2026.

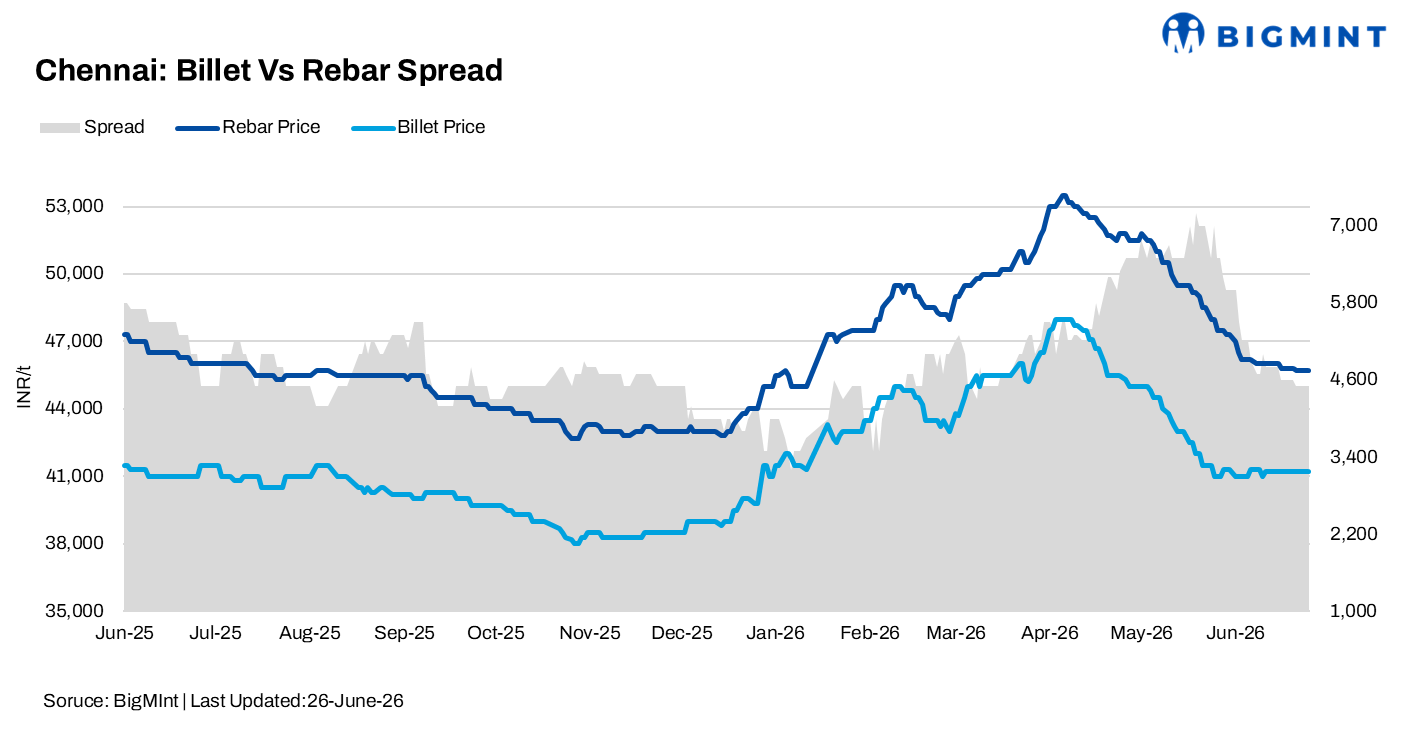

Billet :

MS billet prices across southern markets remained largely stable during the week, with some regions witnessing a slight correction.

As of today, billet prices in the Hyderabad market were assessed at around INR 40,000/t Ex-Works, while prices in Chennai were assessed at approximately INR 41,200/t Ex-Works.

On the demand side, merchant billet suppliers continued to face weak buying interest. Re-rolling mills were reluctant to book fresh material due to sluggish demand for finished steel products and higher inventory levels at mills.

Current rebar inventories are estimated to be around 50% higher than normal maintenance levels, which has further reduced the urgency for fresh billet procurement.

According to market participants, southern steel manufacturers have been receiving healthy enquiries for billet exports from African countries. However, no major export deals have been concluded so far due to the price gap between buyers and suppliers.

Meanwhile, the current billet-to-rebar conversion spread in the Hyderabad market is estimated at around INR 3,000-3,500/t, limiting profitability for re-rolling mills.

Rebar:

Rebar prices across most markets in South India remained largely stable during the week, while a few locations witnessed slight corrections.

Demand from the construction and infrastructure sectors remained weak, with no major movement from new project segments. Most of the material is currently being supplied only to ongoing projects.

High inventory levels at steel mills continue to put pressure on manufacturers to increase sales. This could lead to further price corrections in the near term if demand does not improve.

The price of induction route Fe 500 rebar (12-25 mm) in the Hyderabad market is currently assessed at around INR 43,000/t Ex-Works.

Meanwhile, blast furnace route rebar prices in Hyderabad are currently assessed at approximately INR 52,500/t on an ex-yard basis.

The price gap between induction route and blast furnace route rebar has narrowed slightly compared to previous weeks, mainly due to softer prices in the blast furnace segment.

Outlook:

Steel prices are expected to remain largely stable or witness a slight correction in the near term due to a couple of key factors.

Firstly, higher inventory levels of finished steel products at mills are likely to increase sales pressure on manufacturers, which may force them to reduce their offers to improve liquidity and inventory turnover.

Secondly, the monsoon season is gradually gaining pace across South India, which could further impact construction activity and limit trading volumes in the region.

Considering these factors, the near-term outlook for steel prices in South India remains weak to stable, with a possibility of slight downward pressure on prices.

Leave a Reply