- Lower export realisations keep exporters cautious

- Indian exporters wait for Australian miners’ July discounts

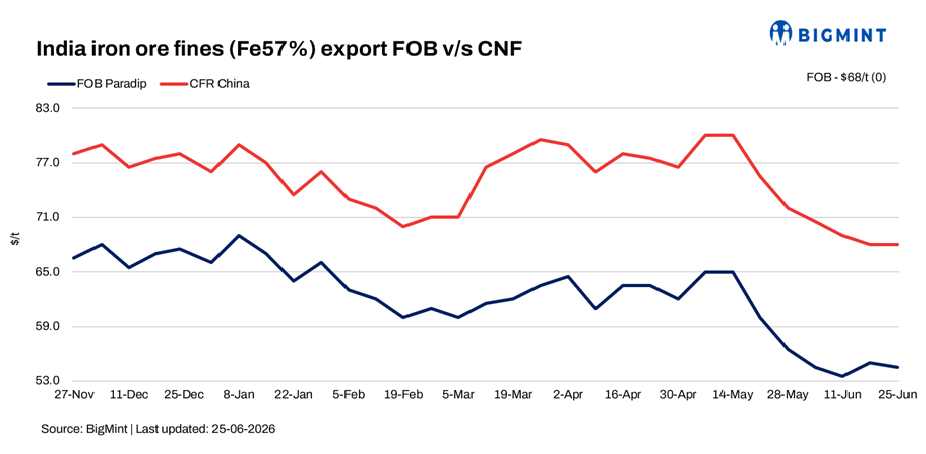

Indian iron ore export prices remained largely rangebound this week as buying interest from overseas markets continued to stay weak, particularly for lower-grade fines. Market activity remained muted with no significant transactions reported during the assessment period, reflecting cautious sentiment among both exporters and buyers.

Rationale

- One deal for Fe 57% was recorded during this publishing window and taken under prices calculation. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received twenty (20) indicative prices in the current publishing window, and fifteen (15) were considered for price calculation as T2 inputs and given the rest 50% weightage.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index at $54.5/t FOB (equivalent to $68/t CFR China) east coast on Thursday, 25 June. One export deal of 65,000 t iron ore fines (Fe57%) export deal was recorded at 25% discount on global index this week from India amid weak market sentiments.

Trading activity was largely absent as exporters adopted a wait-and-watch approach while buyers continued to seek steeper discounts. Several miners were heard offering cargoes at discounts of around 22% to benchmark prices; however, overseas buyers were unwilling to conclude deals above the 25% discount level. As a result, no major transactions were reported during the week.

Iron ore inventories at 34 major Chinese ports stood at 152.5 (excluding pellets) mnt as of 24 June, remained stable w-o-w.

Market scenario

According to market participants, demand for Indian low-grade fines in China remains subdued as Chinese steel mills continue to focus on cost optimization. Mills are increasingly sourcing iron ore from alternative origins where higher discount levels are available, making Indian cargoes comparatively less attractive in the current market environment.

An international trader stated, “Chinese buyers are maintaining a cautious procurement strategy amid uncertain steel market fundamentals and ample raw material availability. Lower-grade iron ore demand remains under pressure, particularly as mills prioritize cost-effective feedstock to protect margins.”

Meanwhile, market sources indicated that seaborne market participants are closely monitoring the discount announcements for July deliveries from Australian miners. The upcoming pricing decisions are expected to provide fresh direction to the low-grade iron ore market and could influence the competitiveness of Indian export cargoes in the coming weeks.

Due to rising coke prices, Chinese steelmakers are increasingly favoring low-alumina pellets and lump ore, as higher-quality raw materials help reduce coke consumption and improve blast furnace efficiency. Lump ore imports continue to offer relatively healthy margins, supporting demand.

However, export realizations for Indian iron ore fines have weakened amid the recent decline in seaborne iron ore prices. A persistent gap between buyer bids and seller expectations has limited trade activity, making exports less attractive. As a result, many Indian miners and traders are shifting their focus toward the domestic market, where returns remain comparatively better.

A miner said, “We are waiting for the market to recover. We receive inquiries daily, but current index levels do not support viable transactions.”

Domestic vs export market

The price gap between export and domestic realisations was recorded at INR 550/t this week,. Export realisations (Fe 57%) were at INR 2,800/t ($30/t) this week while domestic realisations (Fe 57%) remined stable w-o-w at INR 3,350/t ($35/t) exw.

Chinese iron ore fines prices fall w-o-w: The benchmark iron ore fines Fe 61% index dropped by $1/dmt w-o-w to $98/dmt CFR China on 24 June. Market activity gradually resumed following the Dragon Boat Festival holidays, supported by a recovery in domestic Chinese iron ore values and higher domestic coke prices. Trading activity also picked up in the seaborne market. Blending fines are being offered at higher discounts in the secondary market now due to higher phosphorous content, further relaxing the market transections level.

DCE iron ore futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract remained stable w-o-w at RMB 746/t ($110/t) on 25 June.

Outlook

BigMint expects iron ore export prices to remain under pressure in the near term. With buyers continuing to seek aggressive discounts and month-end trading activity typically slowing, market sentiment is likely to remain cautious, resulting in limited deal-making across the export market.

Leave a Reply