- Strong demand and weak hydro output continue to support thermal coal reliance

- Lower coal stocks and firm power prices indicate tighter market conditions

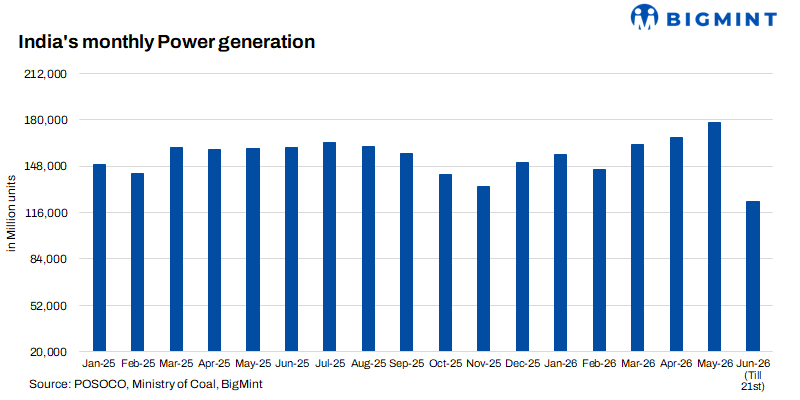

India’s power sector successfully met record electricity demand during the first three weeks of June 2026, although underlying market indicators point to a system operating with tighter margins.

Peak demand increased 7.4% year-on-year to 260.5 GW, while total electricity generation rose 8.6%, supported by an 11.3% increase in coal-fired generation and a 21.6% rise in renewable output. However, a sharp 23.5% decline in hydro generation, falling coal inventories at power plants and elevated electricity exchange prices indicate growing operational pressures.

The ability to meet record demand despite weaker hydro generation highlights the increasing importance of resource adequacy planning, procurement strategies, transmission infrastructure and weather-related risks in shaping market outcomes.

Demand continues to break records

Electricity demand remained strong throughout the first three weeks of June, supported by sustained industrial activity, commercial consumption and higher cooling requirements.

India’s power demand recorded a significant year-on-year increase during 1-21 June 2026 compared with the corresponding period in 2025. The maximum peak demand rose to 260,487 MW from 242,493 MW, marking a growth of 7.4%. The minimum daily peak demand also increased sharply by 11.1%, reaching 231,115 MW compared with 207,975 MW last year. Meanwhile, the average daily peak demand climbed to 248.3 GW, up 10% from 225.7 GW in June 2025, reflecting stronger electricity consumption and higher system load requirements.

The increase in minimum demand suggests India’s base-load electricity requirement continues to rise, pointing to structural growth rather than isolated weather-driven demand spikes.

Generation keeps pace despite hydro weakness

Despite concerns over supply shortages, total electricity generation increased 8.6% year-on-year during the first 21 days of June.

Coal contributed the largest increase in absolute generation, while renewables and nuclear offset much of the hydro shortfall.

Gas-fired generation continued to lose market share as relatively higher fuel costs limited dispatch.

Coal continues to underpin grid reliability

Despite rapid renewable capacity additions, coal remains the backbone of India’s electricity system.

Coal-fired generation increased by more than 8,400 MU, accounting for almost the entire increase in total generation and offsetting the significant decline in hydro output.

The data reinforces a key market reality. While renewable generation continues to expand rapidly, coal remains the principal balancing fuel during periods of sustained peak demand and variable renewable output.

Weak hydro generation emerges as the biggest supply risk

The most significant change in India’s generation mix came from hydroelectric power.

Hydro generation declined by 23.5% year-on-year, reducing output by nearly 2,900 MU.

The decline reflects weaker reservoir inflows and a delayed southwest monsoon, highlighting the growing exposure of hydro-dependent systems to weather-related disruptions.

Kerala’s recent power restrictions illustrate this challenge. Poor rainfall has reduced reservoir storage and hydro generation, forcing the state to rely more heavily on imported electricity and exchange purchases while introducing peak-hour demand restrictions.

The situation highlights the growing role of weather variability in shaping India’s electricity market.

IEX reflects a tighter power market

The Indian Energy Exchange (IEX) provided one of the clearest indicators of tightening market conditions.

Higher purchase bids, stronger market clearing volumes and elevated electricity prices suggest utilities increasingly relied on short-term procurement to meet rising demand.

Unlike June 2025, when daily Market Clearing Prices (MCPs) generally remained between INR 2,250-4,000/MWh, June 2026 witnessed sustained pricing in the INR 4,000-6,000/MWh range, with frequent volatility during evening peak hours. Purchase bids consistently exceeded available sell bids during peak periods, while elevated prices persisted across multiple evening time blocks rather than isolated spikes. Higher scheduled volumes also indicated greater dependence on exchange-based procurement.

The exchange is increasingly functioning as a procurement platform rather than solely a balancing mechanism.

Procurement is becoming more important than capacity

India today possesses more than 530 GW of installed generation capacity, with renewable capacity continuing to expand rapidly.

Yet elevated exchange prices and procurement stress suggest the challenge is shifting from generation adequacy to resource adequacy.

Many DISCOMs continue to rely heavily on day-ahead markets instead of advance contracting and bilateral procurement. When multiple buyers simultaneously enter the market during high-demand periods, prices rise sharply despite adequate national generation capacity.

The result is a system in which procurement strategy is playing an increasingly important role in determining market outcomes.

Power plant coal stocks continue to decline

Higher thermal generation has been accompanied by a steady drawdown in coal inventories.

Coal stocks at power plants declined between 31 May and 21 June, falling from 49.2 million tonnes (mnt) to 46.1 mnt. The stock coverage level also reduced from 65% of the normative requirement to 60%, indicating a gradual drawdown in inventory levels amid sustained power demand. During the same period, the number of critical coal stock plants increased from 22 to 31, reflecting tighter fuel availability concerns at several power stations.

Several state utilities, including Haryana, Telangana and Tamil Nadu, recorded further inventory deterioration.

Nevertheless, the broader supply outlook remains relatively comfortable.

Coal India and SCCL entered the monsoon with record pithead inventories and have implemented comprehensive monsoon preparedness measures to minimise disruptions from heavy rainfall, strengthen mine drainage and ensure uninterrupted dispatches.

These inventories should provide an important buffer against temporary logistical disruptions during the rainy season.

Renewable growth Is beginning to hit the grid wall

Renewable generation increased by nearly 22%, but transmission infrastructure is struggling to keep pace with capacity additions.

Grid congestion and delayed evacuation infrastructure are increasingly constraining renewable utilisation, particularly in Rajasthan, Gujarat and Tamil Nadu.

As a result, thermal generation continues to provide balancing services even when low-cost renewable electricity is available, reinforcing the importance of transmission investment, battery storage and grid flexibility.

The challenge is no longer adding renewable capacity, but ensuring that every megawatt generated can be delivered efficiently to consumers.

Monsoon outlook will shape second-half market dynamics

The southwest monsoon has progressed across much of the country but remains below normal, with both IMD and Skymet forecasting a weaker-than-average season influenced by evolving El Niño conditions.

A subdued monsoon could result in lower hydro generation, continued reliance on coal-fired generation, elevated electricity exchange prices, greater pressure on power plant coal inventories and increased operational risks for open-cast coal mining and transportation.

While strong domestic coal inventories reduce the likelihood of an immediate fuel shortage, weather uncertainty is likely to remain the dominant driver of India’s power market over the coming months.

Outlook

The first three weeks of June indicate that India’s electricity sector is entering a new phase. Generation capacity is keeping pace with demand, coal production remains robust and renewable additions continue at record levels. Yet hydro generation has weakened sharply, power plant coal inventories are tightening and electricity exchanges are playing an increasingly important role in balancing the grid.

The challenge for India’s power sector is therefore evolving from building additional capacity to ensuring that existing capacity is contracted, transmitted, fuelled and dispatched efficiently.

For coal markets, the message is equally clear. Despite rapid renewable growth, coal continues to provide the reliability, flexibility and scale required to support India’s expanding electricity demand. Unless hydro conditions improve significantly and transmission bottlenecks ease, thermal generation is likely to remain the anchor of India’s power system through the remainder of the monsoon season and beyond.

Leave a Reply