- Around 100,000 t each of G6, G10 grades also on offer

- G11 was among most actively traded grades in last auction

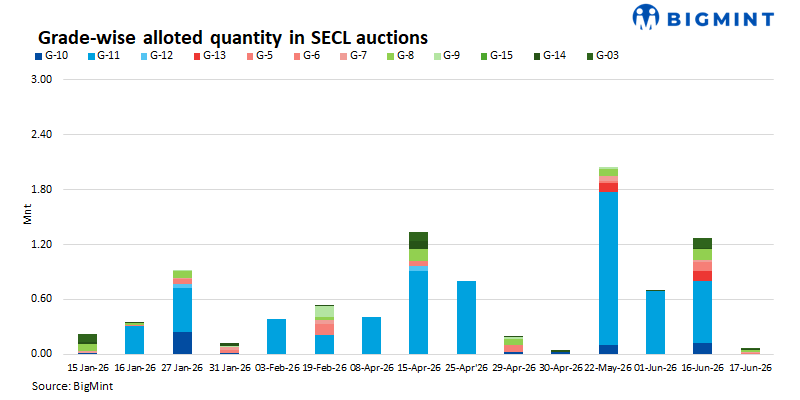

South Eastern Coalfields Ltd (SECL) will auction 1.122 million tonnes (mnt) of non-coking coal on 29 June 2026 under Coal India Ltd’s (CIL) Single Window Mode Agnostic (SWMA) e-auction scheme, following strong buyer participation in its previous auctions held on 16-17 June.

The upcoming sale comes after SECL allocated 1.33 mnt against an offered quantity of 1.79 mnt in the mid-June auctions, achieving an absorption rate of 74%. Demand was led by aluminium, cement, power, and industrial consumers, with several premium grades attracting substantial premiums over notified prices.

G11 coal accounts for bulk of offered volume

G11 coal will dominate the upcoming auction catalogue, with around 908,000 t offered from the Gevra and Dipka clusters at a notified price of INR 1,184/t. The grade was also the most actively traded category in the previous auction, accounting for more than half of total allocations at around 680,100 t.

In the 16-17 June auction, G11 coal cleared at premiums of around 20-21% over notified prices, indicating stable demand from large industrial consumers despite comfortable domestic coal availability.

Premium grades likely to attract attention

SECL has offered 100,000 t of G10 coal from Saraipalli OC in the upcoming auction at a notified price of INR 1,360/t. The grade is expected to remain closely watched after G10 coal from Amadand OC emerged as the best-performing category in the previous auction, fetching a premium of nearly 146% over its notified price.

The company has also offered 114,000 t of G6 coal from Amera OC and Sharda OC, with a notified price of INR 2,761/t. In the previous auction, G6 coal attracted premiums of 34-52%, reflecting healthy demand for higher-grade fuel coal from industrial consumers.

Market outlook

The upcoming auction will provide an indication of whether the stronger procurement sentiment seen in mid-June can be sustained through the monsoon period. While downstream steel market conditions remain mixed, demand from aluminium, cement, and power sectors is expected to continue supporting participation.

Market participants will closely monitor bidding trends for G10 and G6 coal, while the large G11 offering is likely to test the depth of demand from bulk consumers. Strong participation could help sustain premiums across premium grades, although comfortable coal availability may limit aggressive price escalation in lower-grade categories.

Leave a Reply