- Easing geopolitical risks drag crude and bunker prices lower

- Fujairah premiums retreat as Hormuz supply concerns subside

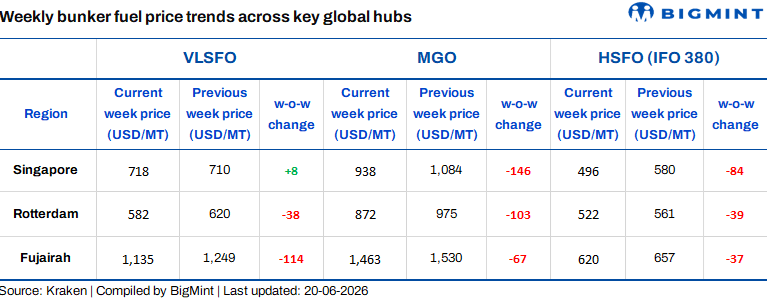

Global bunker fuel prices moved mostly lower in the week ended 20 June 2026, mirroring the sharp correction in crude oil markets. Benchmark VLSFO prices in Singapore stood at $718/metric tonne (mt), up by $8/mt w-o-w, while Rotterdam and Fujairah witnessed steeper declines amid easing geopolitical risk premiums and expectations of improving oil supply flows.

Bunker sentiment remained mixed during the week. Improved prospects for normalization of oil flows through the Strait of Hormuz and easing tensions surrounding the US-Iran conflict have reduced risk premiums across energy markets, pressuring crude and bunker prices.

Increased supplies from major producers and weaker Chinese crude demand have further contributed to the bearish tone in oil markets. Meanwhile, Fujairah premiums softened sharply as fears of supply disruptions in the Gulf region eased.

Despite the recent correction, market participants remain cautious as shipping insurance costs, regional security concerns, and the pace of recovery in Middle Eastern energy infrastructure continue to pose upside risks to bunker prices.

Regional bunker markets

- Singapore: VLSFO prices stood at $718/mt on 20 June, up by $8/mt w-o-w. Sentiment remained firm amid steady bunkering demand and robust vessel traffic, which helped offset weakness in crude prices and supported prompt fuel availability. However, MGO and HSFO softened w-o-w as the US-Iran agreement reduced risk premiums in energy markets, dragging crude and bunker fuel prices lower.

- Rotterdam: VLSFO prices stood at $582/mt, down by $38/mt w-o-w. Rotterdam witnessed broad-based weakness across VLSFO, MGO, and HSFO grades due to ample supply and subdued fuel demand.

- Fujairah: VLSFO prices fell sharply by $114/mt w-o-w to $1,135/mt, with MGO and HSFO also declining in tandem. Bunker fuel sentiment weakened as easing concerns over potential disruptions in the Strait of Hormuz reduced geopolitical risk premiums, following the US-Iran agreement and the subsequent drop in crude oil prices. However, lingering regional uncertainties and elevated insurance costs continued to provide some support to bunker markets.

Factors influencing bunker prices

- Brent crude futures down w-o-w: Brent crude oil (August 2026 contract) was assessed at $79.9/barrel (bbl) on 19 June, down $7.21/bbl w-o-w, reflecting easing geopolitical risk premiums and softer demand expectations, which weighed on overall energy market sentiment.

- WTI crude falls sharply: WTI futures declined by 9.82% w-o-w to $76.54/bbl on 20 June from $84.88/bbl a week earlier. Market sentiment turned bearish amid easing concerns over potential supply disruptions in the Middle East, improving prospects for uninterrupted crude flows through the Strait of Hormuz, and softer demand expectations from major consuming economies.

Outlook

Global bunker fuel sentiment is expected to remain under pressure in the near term amid weaker crude prices and improving oil supply prospects. However, persistent geopolitical uncertainties, insurance premiums, and any renewed disruptions to Middle Eastern export routes could limit further downside.

Singapore bunker prices are likely to remain relatively resilient owing to strong regional demand, while Fujairah premiums may continue to normalize as confidence over uninterrupted Gulf oil flows improves.

Leave a Reply