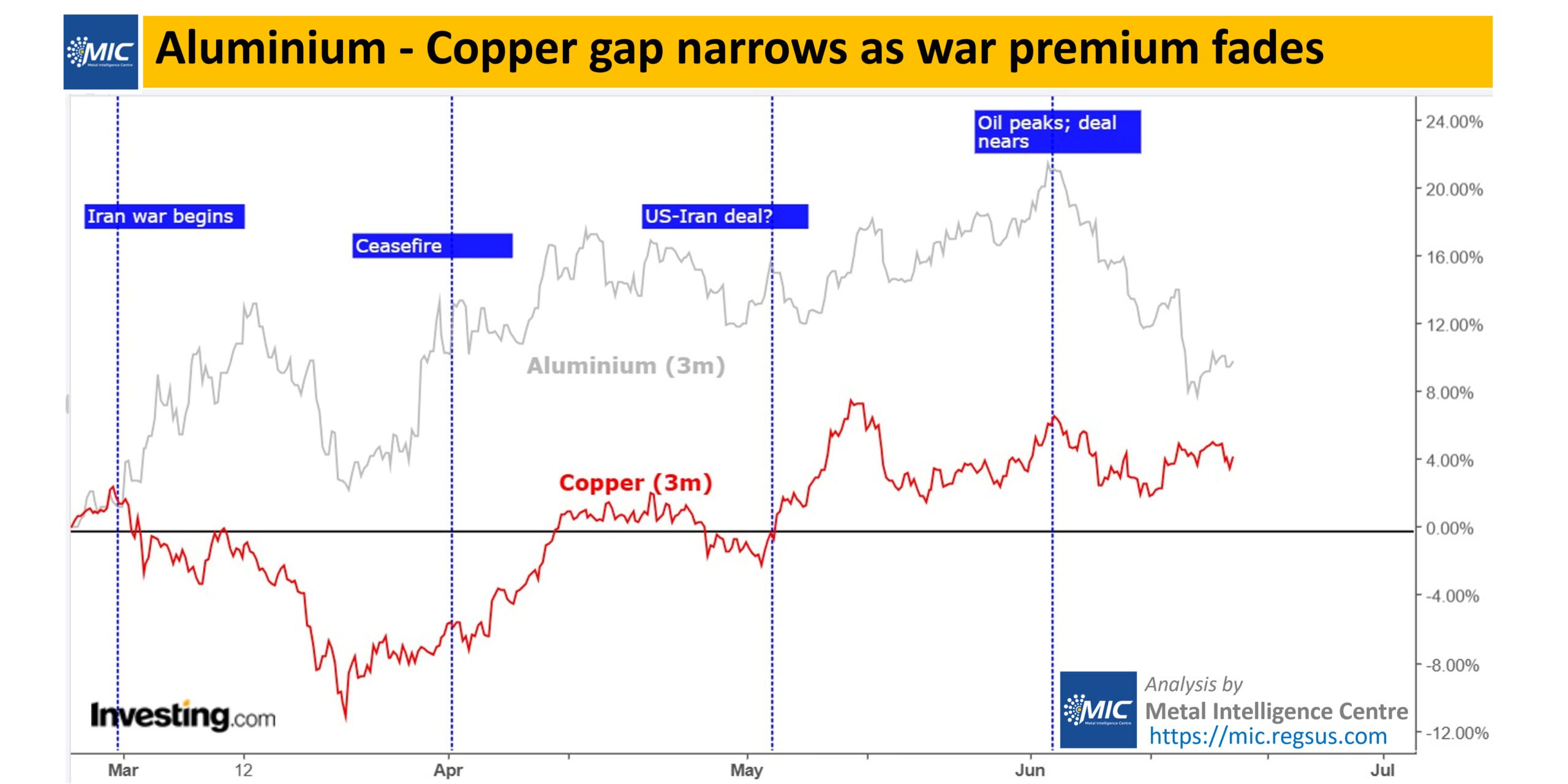

- Supply risks boost aluminium above copper

- Aluminium corrects nearly 10% from highs

Metal Intelligence Centre: Aluminium and copper, which generally move in tandem, diverged sharply after the Iran conflict as geopolitical risks and macroeconomic concerns pulled the two metals in opposite directions. However, the gap narrowed in June following the signing of a US-Iran MoU, as easing concerns over regional supply disruptions weighed on aluminium’s risk-driven gains.

In March, following the outbreak of the war, London Metal Exchange (LME) copper prices weakened amid concerns over slowing global growth and heightened market uncertainty. Aluminium, meanwhile, rallied strongly as fears of supply disruptions gripped the market. The closure of the Strait of Hormuz and attacks on regional smelters threatened exports from the Gulf region, which accounts for nearly 9% of global aluminium production. As a result, aluminium significantly outperformed copper, with the performance gap widening to around 15-17% by late April.

The trend began to reverse as ceasefire discussions emerged and prospects of a broader US-Iran agreement improved. Copper recovered steadily, supported by expectations of US refined copper tariffs, a tightening copper concentrate market, and concerns over sulphur shortages that raised production costs for copper producers. Aluminium, however, struggled to extend gains as fears of an extended supply disruption gradually subsided.

The shift accelerated in early June as oil prices peaked and optimism surrounding a US-Iran deal strengthened. With the reopening of the Strait of Hormuz and easing concerns over Middle Eastern supply disruptions, aluminium surrendered a significant portion of its geopolitical premium, correcting by nearly 10% from its highs. Copper, in contrast, remained relatively resilient and continued to outperform on improving market fundamentals.

As a result, the performance gap between the two metals has narrowed substantially from its peak. Looking ahead, the aluminium market is likely to face renewed scrutiny over demand conditions and rising supply prospects from Indonesia and restarted smelting capacity in the US and Iceland. Unless fresh supply disruptions emerge, aluminium may continue to relinquish its remaining war premium, allowing copper and aluminium to re-align more closely.

Note: This article has been published as part of a content partnership between MIC and BigMint.

Leave a Reply