- Strong steel prices, demand in US support domestic scrap prices

- European dockside prices fall even as suppliers resist lower bids

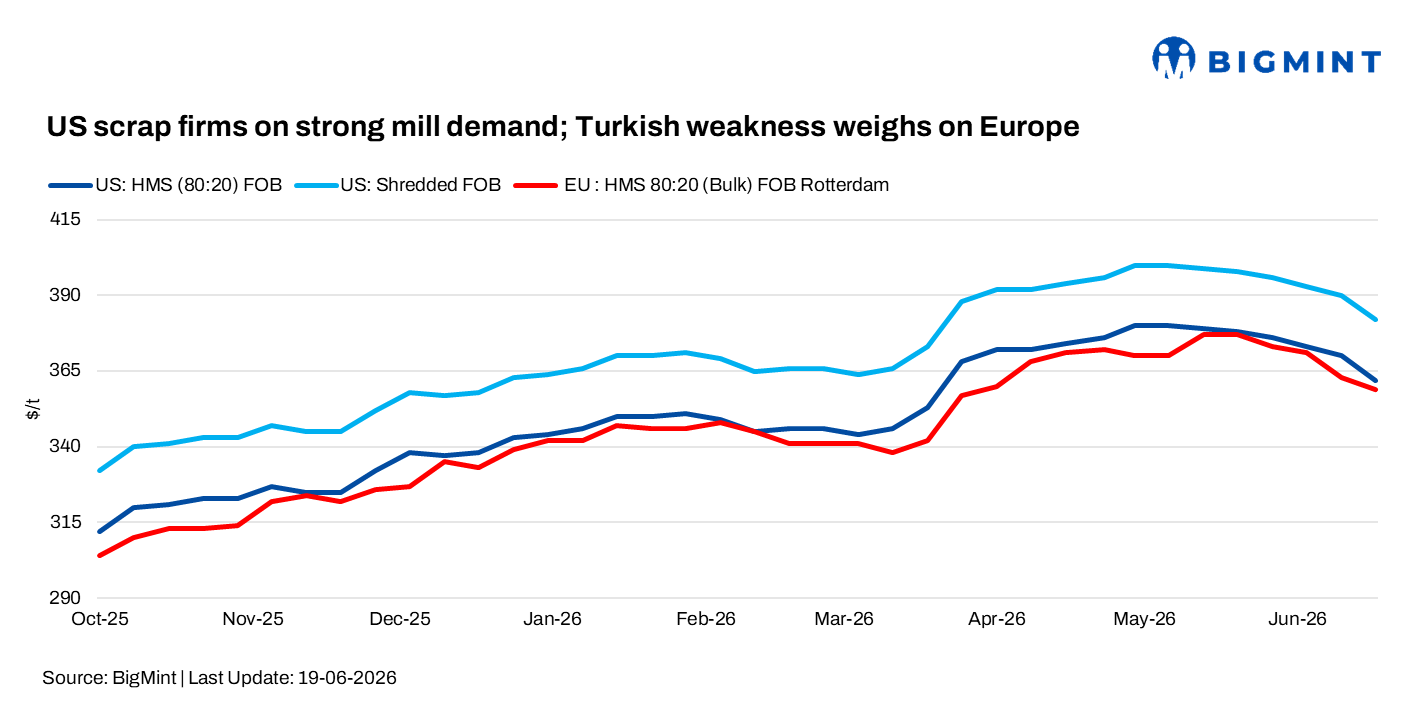

Ferrous export scrap markets across the Americas and Europe presented a mixed picture during the week ended 19 June. Strong domestic steel demand, high mill utilisation rates, and firm finished steel prices supported sentiment in the US, while weaker Turkish buying interest and subdued export activity continued to pressure European scrap markets. Meanwhile, Mexico remained stable despite seasonal demand concerns, and Brazil recorded modest domestic gains driven by rising operating costs.

US

The US ferrous scrap market remained stable during the week ended 19 June, supported by strong domestic steel demand, firm finished steel prices, and mill utilisation rates above 80%. Busheling held at around $460-462/t DAP, shredded scrap at $430-435/t DAP, plate and structural at $405/t DAP, and HMS at $375/t DAP across the Midwest and Southeast. Midwest shredded scrap was heard at $425-435/t DAP, while busheling remained at $455-465/t DAP.

Strong steel market fundamentals pushed Midwest HRC prices up, marking a fresh three-year high. Export activity remained subdued, with Turkish HMS 80:20 import prices declining to $395-398/t CFR amid weak rebar demand and cautious buying. Meanwhile, the partial reopening of the Strait of Hormuz and softer oil prices below $80/bbl provided some support to overall market sentiment by easing concerns over energy and freight costs.

Europe

European ferrous scrap markets remained under pressure in the week ended 19 June, weighed down by weak Turkish buying interest and subdued export activity. HMS 80:20 dockside prices declined by EUR 5/t w-o-w to EUR 285-290/t ($325-330/t), while HMS 80:20 export values eased to around $359-360/t FOB Rotterdam.

Similarly, UK shredded scrap export prices softened to $380/t (EUR 330/t) FOB, down from about $390/t (EUR 340/t) earlier in the month.

Despite weaker export sentiment, the UK domestic scrap market remained largely stable in June. HMS prices were heard at around GBP 165-185/t (EUR 195-220/t; $220-250/t) DAP, while plate and structural scrap traded at GBP 195-215/t (EUR 230-255/t; $260-290/t). Lower-grade light scrap was assessed at GBP 120-140/t (EUR 140-165/t; $160-190/t).

Market participants indicated stable domestic settlements, comfortable mill inventories, and balanced scrap flows. While a handful of transactions were concluded at discounts of up to GBP 5/t ($7/t) in regions with surplus availability, most contracts were rolled over unchanged from May. Suppliers largely resisted lower bids, citing processing costs and export alternatives, although weakening dockside values continued to weigh on overall sentiment.

As a result, market sentiment across Europe remained cautious, with limited appetite from buyers and no significant pressure from sellers to move prices aggressively in either direction.

Mexico

Mexico’s ferrous scrap market remained largely stable in the week ended 19 June, despite signs of a seasonal slowdown. HMS prices in Northeast Mexico edged down by around MXN 100/t ($6/t) to MXN 6,500-6,600/t ($375-380/t) FOB, while busheling remained steady at MXN 7,300-7,500/t ($420-430/t) FOB. In the Bajío region, HMS was heard at around MXN 6,700/t ($385/t) DAP, while busheling held at MXN 7,900-8,000/t ($455-460/t) DAP.

A major steelmaker announced a MXN 400/t ($23/t) reduction in scrap procurement prices for Bajío deliveries, citing lower steel production and softer downstream demand. Market participants remained cautious, with summer seasonality expected to weigh on trading activity in the coming weeks. However, current scrap prices continue to remain well above year-ago levels, supported by relatively firm domestic market fundamentals.

Brazil

Brazil’s ferrous scrap market recorded modest gains during the week ended 19 June, supported by higher operating, logistics, and fuel costs. Market participants reported mixed pricing trends, with some steelmakers raising procurement prices while others lowered bids based on individual inventory requirements.

Domestic scrap prices edged up during the week, with HMS 80:20 at BRL 925-930/t ($180-181/t) FOT, turnings at BRL 825-830/t ($160-161/t) FOT, and clean steel scrap at BRL 1,005-1,010/t ($195-196/t) FOT, supported by higher operating and logistics costs.

Meanwhile, export sentiment weakened, with HMS export prices declining by $5/t to $310-315/t FOB, while shredded scrap fell by $5/t to $325-330/t FOB, pressured by the depreciation of the US dollar and subdued export demand.

Leave a Reply