- Sponge iron slips while finished steel prices inch higher

- Weak buying interest, regional competition cap market momentum

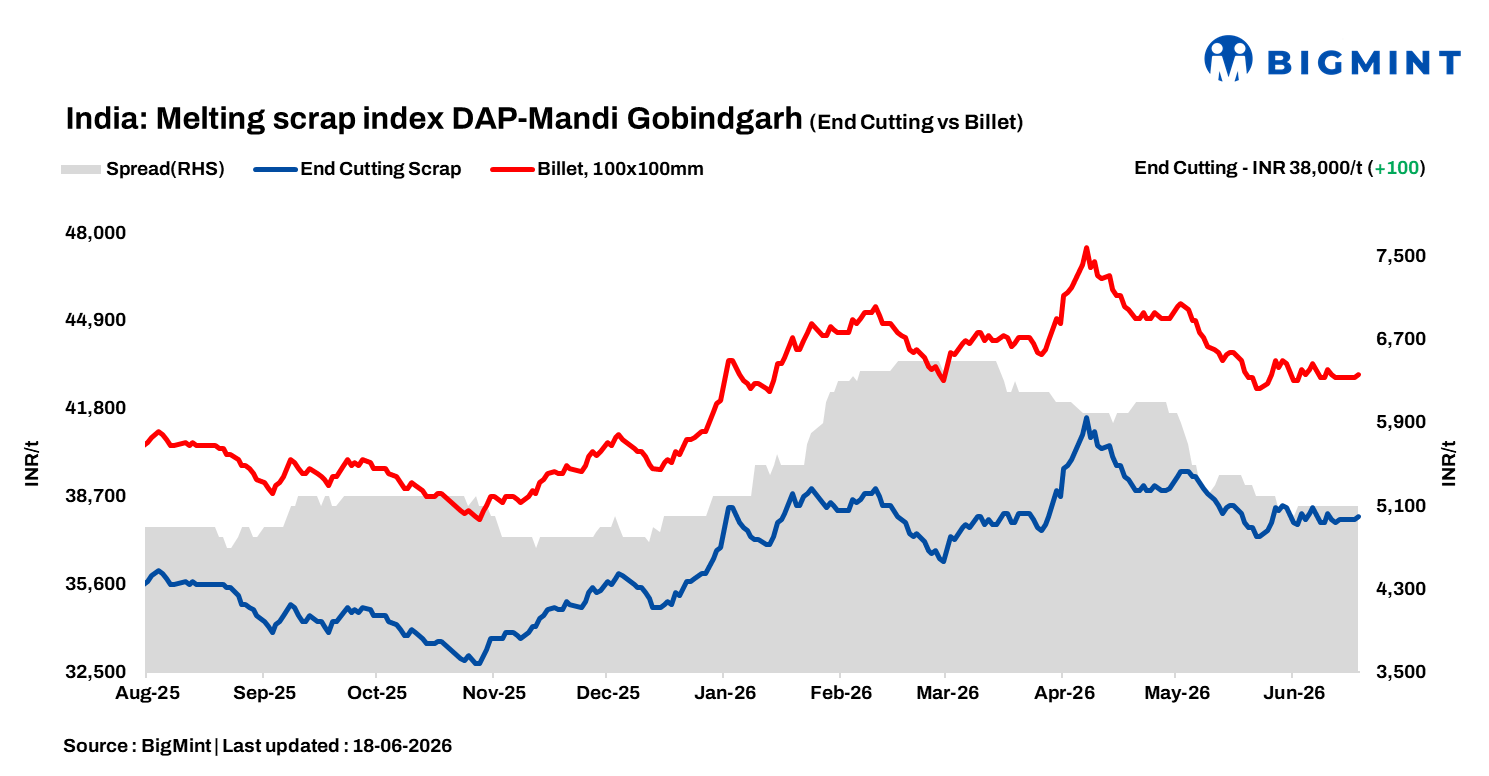

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by INR 100/t d-o-d to INR 38,000/tonne (t) DAP on 18 June 2026.

Mandi Gobindgarh, a key secondary steel hub in northern India, saw a marginal price uptick across most steel segments today, though large-volume deals remained absent from the market. Scrap-to-finished steel prices inched up by INR 100/t d-o-d, while sponge iron prices declined by INR 100/t.

Local steelmakers are hoping for a near-term pickup in both demand and prices, but buying remains subdued with limited transaction volumes and no major bulk deals reported. The viability of semi-finished and finished steel supplied from neighbouring regions is constraining demand in the local Mandi market, and mill owners report pressure on pricing as buyers are unwilling to chase higher prices amid weak finished steel demand.

Alternative raw material prices

Sponge iron (CDRI) in Mandi Gobindgarh fell by INR 100/t to INR 30,000/t DAP, while steel-grade pig iron in Ludhiana remained at INR 41,400/t DAP.

Steel market

The Mandi steel market recorded a modest price increase today, with semi-finished steel prices rising marginally by INR 100/t day-on-day to reach INR 43,000/t DAP, while other major production centres reported minor upticks ranging between INR 100-400/t. In Mandi Gobindgarh, rebar (Fe500) prices moved up by INR 100/t to INR 47,600/t ex-works, reflecting cautious optimism in the key secondary steel hub, whereas HR strip (patra) prices remained unchanged at INR 46,800/t exw, indicating stable demand in the flat products segment.

Overview of western India

The Jalna steel market saw HMS (80:20) scrap prices dip by INR 300/t to INR 33,000/t DAP, while semi-finished steel prices inched up by INR 200/t d-o-d to INR 41,000/t DAP; finished steel prices remained stable at INR 45,300/t exw amid limited buying. Jalna mills are facing margin pressure as billet prices fell sharply by approximately INR 1,400-1,500/t during May-June, while scrap prices declined by only INR 600-700/t, creating a cost-structure mismatch that has squeezed the profitability of local producers.

Scrap prices remained relatively firm despite the dip due to heatwave-related labour shortages and loading/unloading delays that restricted scrap collection and supply. Meanwhile, improved railway rake availability has eased sponge iron procurement from Raipur and nearby regions, prompting many mills to increase sponge iron usage from 15-20% to 30-40% of their metallic mix, with mills having sponge iron production facilities in Chandrapur and Nagpur are using up to 50% sponge iron in their charge mix as a cost-optimisation strategy amid billet price decline.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,900-5,300/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $345/t, approximately INR 34,800/t (inclusive of freight). HMS (80:20) prices in Mumbai remained steady for the fourth consecutive day at INR 33,250/t DAP. Indicative prices of shredded from Europe stood at $388/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,800/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply