- India remains sidelined as cheaper domestic feedstock erodes import viability

- Geopolitical tensions prompting a cautious approach among buyers

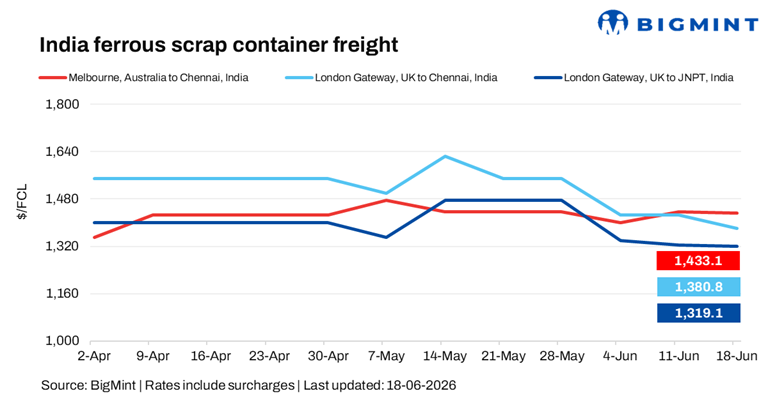

India-bound ferrous scrap container freights remained under pressure in the week ended 18 June across regions. Persistent geopolitical tensions continue to cloud market sentiment, prompting buyers to adopt a cautious approach amid uncertainty over trade flows and energy costs.

Imported ferrous scrap sentiment remained subdued as weak steel demand, poor import viability, and the availability of cheaper domestic alternatives such as sponge iron and DRI continued to suppress buying interest. Indian buyers largely stayed on the sidelines, with a wide gap between bids and offers limiting fresh transactions.

UK-origin ferrous scrap sentiment remained weak, with exporters facing persistent downward pressure amid soft demand from key destinations and lower workable price levels, BigMint noted.

Meanwhile, Australia-India container freight sentiment remained rangebound, with market activity staying sluggish amid limited cargo enquiries and balanced vessel availability. Market participants largely adopted a wait-and-watch approach, keeping rates stable despite easing bunker costs.

Route-wise update

Market highlights

- Geopolitical risks and tight capacity underpin CFI: CFI increased by 136.47 points w-o-w to 3,121.69 points on 18 June from 2,985.22 points on 12 June, reflecting firm container freight sentiment. Strong peak-season demand, cargo front-loading, and continued Red Sea-related disruptions supported rates despite easing bunker prices.

- Bunker prices drop w-o-w: Bunker prices decreased by $158/t w-o-w to $658/t on 18 June, as easing geopolitical tensions and the expected reopening of the Strait of Hormuz weighed on crude prices. Lower fuel costs are providing relief to shipping expenses and supporting a softer freight outlook, although lingering security concerns continue to keep market participants cautious.

Outlook

Ferrous scrap container freight rates are expected to remain range-bound in the near term. Shipment backlogs may continue to provide some support, but easing bunker prices, improving equipment availability, and subdued scrap demand are likely to cap any significant upside. Market sentiment is expected to remain cautious amid geopolitical uncertainties and weak steel sector fundamentals.

However, a gradual recovery in trade activity and overall market sentiment could lend support to freight markets over the coming months as a UK-based shipbroker mentioned, “Seasonal labour shortages during the upcoming UK/EU summer holiday period are expected to tighten logistics capacity further, keeping rates elevated.”

Leave a Reply