- Chinese market closed due to festival

- Discount hovers at a similar range w-o-w

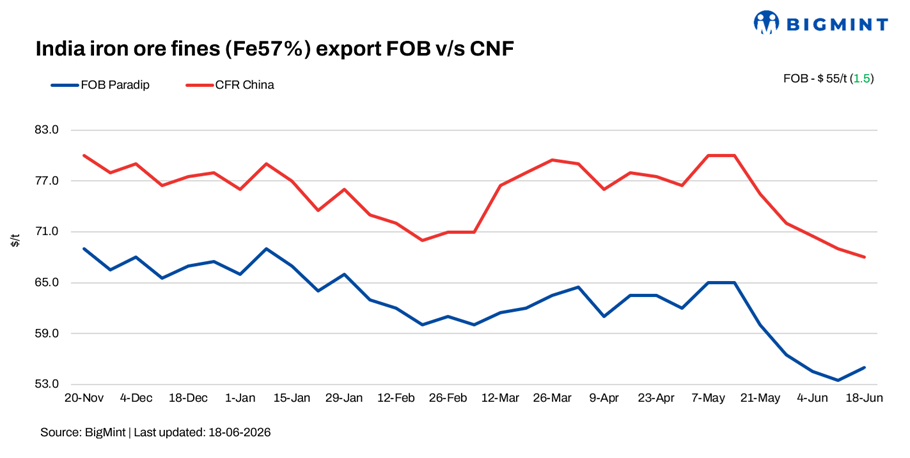

India’s iron ore export prices on an FOB basis witnessed improvemnet around $1-2/t this week, primarily supported by the decline in vessel freight rates in the seaborne market. Lower freight costs improved export realisations for suppliers, offering some relief amid otherwise subdued market conditions. The seaborne market will remain closed tomorrow due to the Dragon Boat Festival holiday in China.

Rationale

- No deals for Fe 57% were recorded during this publishing window and not taken under prices calculation. Therefore, T1 trade was given 0% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received twenty two (22) indicative prices in the current publishing window, and fifteen (15) were considered for price calculation as T2 inputs and given the rest 100% weightage.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index at $55/t FOB (equivalent to $68/t CFR China) east coast on Thursday, 18 June. No export deal was recorded this week from India amid weak market sentiments.

Discounts for Indian Fe 57% fines were assessed at around 24-26%, while lower-grade Fe 55% fines were heard at 30-32% discount during the week.

Iron ore inventories at 34 major Chinese ports stood at 152.5 (excluding pellets) mnt as of 17 June, rising 1 mnt w-o-w against 10 June.

Market scenario

Despite the improvement in Indian FOB offers, the broader global iron ore market remained under pressure due to weakening fundamentals and cautious sentiment ahead of China’s Dragon Boat Festival holiday. Market participants noted that buying activity in the international market slowed significantly as traders and steelmakers adopted a wait-and-watch approach before the holiday period.

An exporter commented, “Spot market transactions remained largely absent during the week. Sellers continued to hold their offers firm in anticipation of improved pricing, while buyers maintained similar discount expectations, resulting in a significant gap between bid and offer levels.”

Another exporter said, “FOB prices have improved slightly due to softer freight rates, but the domestic procurement cost of iron ore remains elevated. Current export realisations are still not providing attractive margins for fresh deals.”

Another market participant mentioned that most exporters were refraining from aggressive sales and closely monitoring developments in the Chinese market. He added, ” There is limited urgency among sellers. Many exporters are waiting for clearer demand signals from China before committing to new cargoes.”

Meanwhile, several miners and traders who concluded export deals a few weeks ago are currently focused on executing and shipping those cargoes to China. As a result, fresh spot market offerings have remained limited.

The recent freight correction has improved export competitiveness to some extent; however, uncertainty surrounding Chinese steel demand and iron ore consumption continues to weigh on market sentiment.

Looking ahead, market participants expect greater clarity to emerge after the Dragon Boat Festival.

Chinese iron ore fines prices fall w-o-w: The benchmark iron ore fines Fe 61% index dropped by $3/dmt w-o-w to $99/dmt CFR China on 17 June. Prices lost strength amid growing pressure from weak steel demand and shrinking mill margins in China. The decline was mainly linked to continued weakness in China’s steel sector, which is currently in its seasonal off-season period. Heavy rainfall across southern China disrupted construction activity and slowed finished steel consumption, reducing demand for raw materials. Moreover, chances of a near-term recovery in steel demand remain low, keeping iron ore sentiment weak.

DCE iron ore futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract decreased by RMB 20/t ($3/t) w-o-w to RMB 746/t ($110/t) on 18 June.

Outlook

BigMint expects greater clarity to emerge after the Dragon Boat Festival. Buying interest could gradually return if Chinese steel production remains stable and freight rates continue to support export economics. Consequently, some spot deals are expected to materialise over the next couple of weeks as buyers and sellers reassess market conditions.

Leave a Reply