- Domestic coal remains preferred

- Imports stay requirement-based

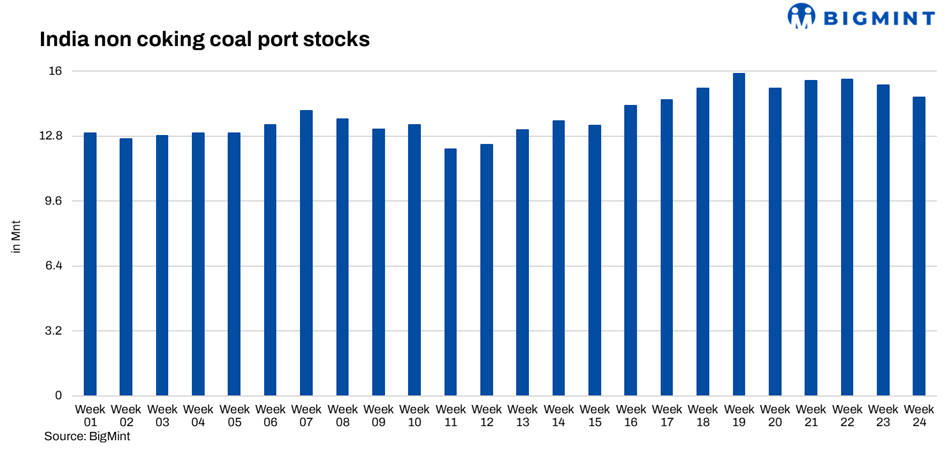

India’s coal inventories at major ports declined by 5.7% w-o-w to 14.72 mnt in Week 24, compared with 15.61 mnt in Week 23, reflecting stronger evacuation across several key ports. Despite the drawdown, imported coal demand remained subdued as consumers continued to rely on ample domestic coal availability and maintained a cautious procurement strategy ahead of the monsoon season.

Major ports witness inventory drawdown

Inventory levels fell across several major imported coal hubs during the week. Mundra recorded one of the steepest declines, with stocks dropping 36.3% w-o-w to 1.27 mnt, while Gangavaram inventories fell 38.8% to 0.19 mnt. Vizag stocks declined 25.9% to 0.61 mnt, while Tuna, Mangalore and Dhamra also registered notable reductions.

The decline suggests steady evacuation of existing cargoes, although market participants indicated that fresh import bookings remained limited. Hazira continued to hold the largest inventory among ports at 2.47 mnt, followed by Paradip at 1.41 mnt and Kandla at 1.32 mnt.

Select ports see higher arrivals

While overall inventories declined, a few ports reported gains during the week. Kakinada inventories increased 62.7% w-o-w, Gopalpur rose 138.7%, while Navlakhi and Karaikal registered increases of 27.7% and 21.3%, respectively. Kandla also witnessed a 16.3% rise in stocks, indicating fresh arrivals or slower evacuation at selected locations.

However, these gains were insufficient to offset the broader decline observed across major coal-handling ports.

Importer-wise trends

Among importers, Adani Enterprises continued to hold the largest inventory position despite stocks declining sharply by 24.4% w-o-w to 3.02 mnt from 4.00 mnt. Agarwal Coal also reported a decline of 11.8% to 0.67 mnt, reflecting steady evacuation and lower replenishment during the week. In contrast, Adani Power’s inventories increased by 14.2% w-o-w to 1.03 mnt, indicating fresh arrivals and stock build-up. Meanwhile, ArcelorMittal maintained stable inventory levels at 1.22 mnt, broadly unchanged from the previous week. The mixed movement across major importers reflected varying procurement and consumption patterns, although overall imported coal demand remained subdued.

Market dynamics

Thermal power plant coal inventories declined week-on-week to approximately 47 mnt as on 11th Jun’26, equivalent to around 16 days of consumption. While the broader supply situation remained comfortable, around 26 power plants continued to report critical stock levels, highlighting uneven distribution and regional supply constraints.

Imported coal sentiment softened during the week as market participants closely monitored developments in the Middle East following signs of easing tensions between the US and Iran. The improvement in geopolitical sentiment reduced concerns over freight escalation and supply disruptions, prompting expectations of softer seaborne coal offers in the near term. Several traders indicated that buyers who had remained on the sidelines due to elevated prices may gradually return to the market if freight rates and imported coal offers continue to ease.

At the same time, domestic coal availability remained comfortable, limiting any urgency for immediate imports. However, market participants reported an increase in enquiries for imported coal, particularly from sponge iron and industrial consumers, as buyers began reassessing procurement opportunities amid softer international sentiment. While actual bookings remained limited, the recent correction in imported coal offers is expected to improve buying interest in the coming weeks if downstream steel and industrial demand stabilises.

Outlook

Coal inventories at Indian ports may continue to witness gradual fluctuations in the coming weeks depending on cargo arrivals and evacuation trends. However, with domestic coal supplies remaining comfortable and industrial demand yet to show significant improvement, imported coal buying interest is expected to remain subdued. Procurement is likely to stay requirement-based unless international prices become more competitive or downstream demand strengthens.

Leave a Reply