- West African demand supported freight sentiment

- Container freight remained firm amid congestion and GRI expectations

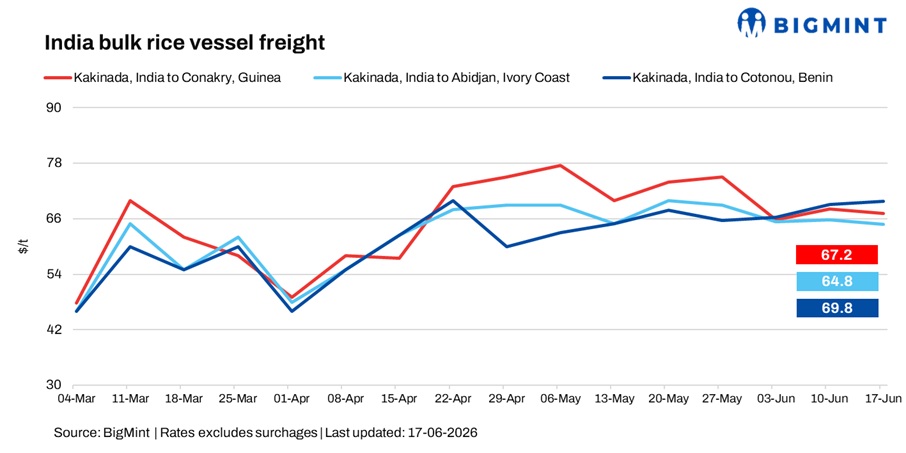

India’s rice freight market showed mixed trends in the week ended 17 June 2026. Strong demand from West Africa continued to support select bulk routes, while container freight remained firm due to port congestion, cautious carrier pricing, and limited equipment availability.

Although the proposed US-Iran truce has boosted confidence in global shipping markets, freight rates have yet to show any significant softening.

West Africa remains the key freight driver

West African demand remained the key market driver, with active fixtures for Benin supporting freight sentiment. However, softer cargo enquiries on some destinations and selective chartering activity limited broader strength despite ongoing congestion at regional ports.

Market participants told BigMint, “Shipping activity through the Strait of Hormuz is expected to recover gradually following the US-Iran truce. However, shipowners are unlikely to resume normal operations until they are confident the route is safe, keeping freight sentiment firm in the near term.”

Another shipbroker added, “Rates for West Africa are broadly in line with last week’s levels, with only marginal variation. However, some shipping lines have temporarily suspended bookings, limiting cargo movement and limiting cargo movement and delaying a broader market recovery.”

Route-wise update

Container market remains cautious

Container freight remained largely stable across East African routes, supported by congestion and limited equipment availability. Shipping lines maintained firm pricing, while market participants awaited fresh freight quotations following the anticipated General Rate Increase (GRI) as one trader noted, “Fresh freight quotations are expected next week as shipping lines are withholding bookings ahead of an anticipated GRI.”

Another rice trader said, “The market outlook remains unclear, and we expect greater clarity over the next week. Shipping lines continue to adopt a cautious approach and have yet to reduce freight rates.”

Outlook

Freight is expected to remain firm in the near term as port congestion and carrier pricing continue to support the market. A shipbroker said, “It could take around two months for congestion to ease, with freight rates expected to remain firm until then before gradually softening.”

The gradual recovery in shipping through the Strait of Hormuz, easing port congestion and post-GRI pricing trends will remain key factors to watch over the coming weeks.

Leave a Reply