- Rising costs in Russia, Indonesian regulatory uncertainty support prices

- Chinese demand supports prices but Indian buyers remain cautious

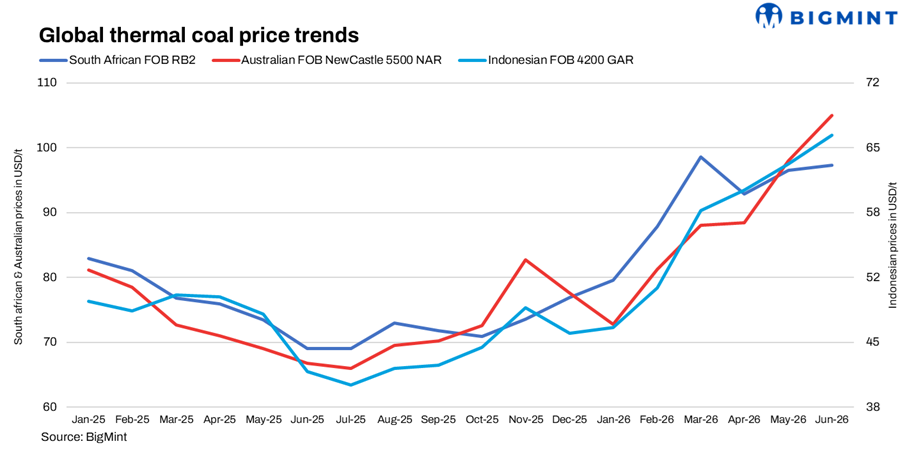

The Asian thermal coal market has shifted from a demand-led recovery to a supply-driven rally, with Australian high-calorific value (CV) coal leading gains, while lower-rank Indonesian grades rise more gradually, price assessments recorded over 8-12 June 2026 show.

Growing concerns over future export availability from major suppliers, particularly Indonesia, Australia, and Russia, have increasingly shaped market sentiment, outweighing relatively subdued demand growth. While Chinese buying continues to underpin prices and India remains largely absent from the market, tightening prompt supply has strengthened bullish sentiment across the seaborne coal trade.

Australian coal drives market higher

The strongest gains have been recorded in Australia’s Newcastle market. Physical FOB Newcastle 6,000 NAR coal traded around $128-130/t in late May before climbing steadily to $152-157/t by the week ending 12 June.

The rally has been accompanied by a significant shift in index-linked trading behaviour. Earlier in the quarter, buyers were seeking substantial discounts to prevailing index levels. By mid-June, however, August cargoes were changing hands at flat index levels while sellers were increasingly seeking premiums of $5-8/t above index references.

This transition is particularly important because it reflects tightening prompt availability rather than merely speculative activity. Market participants report that July-loading cargoes are becoming increasingly difficult to source, while August positions are attracting growing interest from buyers seeking coverage ahead of the third quarter.

The premium for high-energy coal remains substantial. Newcastle 6,000 NAR cargoes continue to command a wide premium over lower-quality products, highlighting strong demand for fuel efficiency and supply security among utilities across North Asia.

Supply uncertainty replaces demand as key market driver

Unlike previous rallies that were primarily demand-led, the current market strength is increasingly linked to supply-side developments.

Indonesia’s transition to the new state-controlled export structure remains a major source of uncertainty. Although the first phase of implementation has begun, market participants remain unsure how production quotas, export approvals, and future cargo availability will evolve during the second half of the year.

At the same time, Indonesian miners continue to face uncertainty over quota revisions. Many market participants believe production increases may be limited, raising concerns that export availability could tighten later in the year.

Russian exporters are contending with rising domestic transportation costs, tariffs and currency pressures.

Individually, none of these factors is sufficient to drive a major market rally. Collectively, however, they are creating a risk premium that is increasingly being reflected in seaborne coal prices.

Indonesia firms, but lags Australia

Indonesian low-rank coal prices have strengthened over the past month, although gains remain significantly smaller than those seen in Newcastle.

Offers for 3,800 NAR equivalent coal have risen from the mid-$60s/t in May to around $70-72/t FOB during June. However, confirmed trading activity remains relatively limited compared with the Australian market.

The slower pace of appreciation reflects a more balanced supply-demand picture. Indonesian producers continue to offer substantial volumes, while Chinese buyers remain highly price sensitive.

Even so, the direction of travel remains upward. Recent Chinese tender awards suggest buyers are increasingly willing to accept higher prices for imported low-rank coal, indicating that the market has likely established a floor after the weakness seen earlier this year.

China supports the market but does not lead it

China remains the single most important source of demand for seaborne thermal coal, particularly for Indonesian low-rank grades.

Recent South China tender activity has shown a clear improvement in buyer participation. Tender awards for Indonesian 3,600-3,800 NAR coal were concluded at offered prices, suggesting that end-users are prepared to secure cargoes rather than wait for lower prices.

However, China’s domestic market may be entering a period of consolidation. Qinhuangdao FOB markers rose steadily through May and early June before recording their first weekly decline during the week ending 12 June.

The pullback has been modest and should not yet be interpreted as a bearish reversal. Instead, it appears to reflect temporary resistance after a strong run-up in prices.

Indeed, the most notable feature of the Chinese market is that import demand has remained resilient despite higher domestic prices. This suggests buyers remain concerned about future supply availability and are unwilling to rely exclusively on domestic coal.

Indian demand remains subdued

While China has provided the immediate support for seaborne prices, India remains the market’s most important wildcard.

Indian import demand has been notably subdued in recent weeks despite firm international prices. Strong domestic coal production, comfortable pithead inventories and the arrival of the southwest monsoon have reduced the urgency for imports.

Yet several indicators warrant close attention.

Coal inventories at thermal power plants have been gradually declining, while power demand remains elevated. At the same time, the monsoon season introduces fresh uncertainty around mining activity, transportation networks and coal movement across the domestic supply chain.

For now, Indian buyers remain largely absent from the international market. However, should domestic logistics tighten or inventories decline more rapidly than expected during July and August, India could re-emerge as a significant buyer, providing additional support to seaborne prices.

Two-speed market likely to persist

The current market increasingly resembles a two-speed system.

High-CV Australian coal continues to outperform, supported by tightening availability and stronger utility demand. Low-rank Indonesian coal is also strengthening but remains constrained by China’s price-sensitive purchasing behaviour.

This divergence is likely to persist through the third quarter unless Chinese domestic prices weaken materially or Indonesian supply expands significantly beyond current expectations.

Outlook: Bullish, but consolidation risks rising

The near-term balance of risks remains tilted to the upside.

Supply uncertainty in Indonesia, tightening availability of Australian prompt cargoes, ongoing logistical challenges in competing export regions and resilient Chinese buying are collectively supporting the market.

However, signs of consolidation are beginning to emerge. Chinese domestic prices have paused after a strong rally, Indian buyers remain largely on the sidelines, and some paper market valuations appear increasingly aggressive relative to underlying physical demand.

As a result, the market may be approaching a period of consolidation rather than another immediate leg higher.

The next four to eight weeks will be critical. Should Chinese utilities continue to procure imports, Indonesian supply remain constrained, and India return to the market during the monsoon period, Newcastle coal could test fresh highs. Conversely, a sustained decline in Chinese domestic prices could cap further gains and encourage profit-taking across the seaborne market.

For now, the market remains firmly supported, with supply concerns continuing to outweigh demand weakness.

Leave a Reply