- Domestic coal prices stable amid improved sentiment

- Falling steel prices pull down India coking coal index

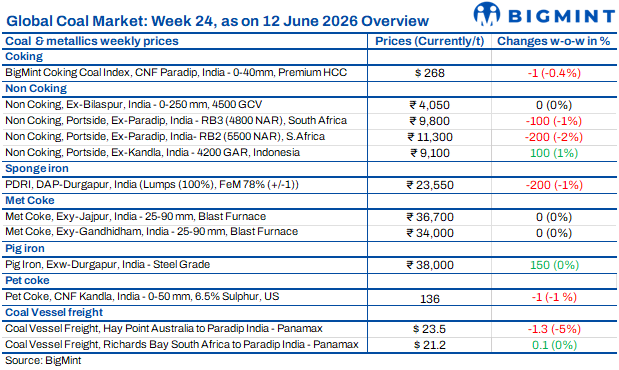

Indian coal market sentiment remained cautious during the week ended 12 June 2026. Firm global fundamentals, supply-side tightening, and elevated freights failed to translate into stronger buying interest in India. Industrial consumers largely restricted purchases to immediate requirements amid weak steel and sponge iron demand, while cement buyers stayed selective ahead of the monsoon. Domestic availability remained comfortable, and buyers across segments focused on preserving margins rather than building inventories, keeping overall trade activity subdued despite selective spot transactions.

Indonesian coal prices edge higher

Indian portside Indonesian coal prices increased marginally, supported by limited Indonesian spot availability and steady Asian demand. Kandla 5,000 GAR rose by INR 100/t to INR 11,000/t, while Visakhapatnam increased to INR 10,900/t. Kandla and Vizag 4,200 GAR gained INR 100/t to INR 9,100/t and INR 9,000/t, respectively. Navlakhi 3,400 GAR climbed INR 250/t to INR 7,100/t amid tighter ready stocks. Freights edged up to around $22/t. Indian port inventories declined to 15.31 mnt, while power plant stocks fell to 47 mnt. However, buyers remained cautious, preferring domestic coal over costly imports.

South African demand remains weak

South African thermal coal sentiment remained subdued despite firmer global cues. BigMint assessed ex-Paradip RB2 at INR 11,300/t, down INR 200/t w-o-w, while RB3 declined by INR 100/t to INR 9,800/t. Ex-Vizag RB2 dropped by INR 300/t to INR 10,800/t, while RB3 remained stable at INR 9,800/t. India’s portside thermal coal inventories declined by 1.9% w-o-w to 15.31 mnt, indicating a slight drawdown. Limited RB3 deals were concluded at INR 9,700-9,900/t, while vessel offers remained firm at $115-118/t CFR, supported by freights of $21-22/t and RBCT maintenance concerns. However, weak sponge iron economics, cautious procurement, and poor finished steel demand kept buyers away from fresh bookings. C-DRI Durgapur prices fell by INR 100/t w-o-w to INR 26,200/t DAP, with several sponge producers reporting margin pressure and operating at reduced capacities.

Domestic coal sentiment improves

BigMint assessed domestic 5,000 GCV non-coking coal stable at INR 5,500/t and 4,500 GCV coal unchanged at INR 4,050/t, both exw-Bilaspur. Market sentiment improved during the week as the recent SECL auction recorded healthy premiums, particularly for G11 coal, attracting participation from sponge iron, cement, and power sector buyers. Traders also reported a pick-up in enquiries, suggesting improving procurement interest despite the onset of the monsoon and continued requirement-based buying.

NAPP demand loses momentum

US Northern Appalachian (NAPP) coal sentiment in India weakened as cement buyers adopted a cautious approach ahead of the monsoon. Ex-wharf NAPP prices at Kandla and Tuna were heard at INR 13,500-14,000/t, while buying interest remained limited. Retail stocks stood at 349,244 t as of 8 June, including 159,704 t at Kandla and 189,540 t at Tuna, despite declining from 587,805 t in mid-May. Weekly lifting eased to 95,640 t in Week 23, compared with 99,486 t in Week 22 and 122,876 t in Week 21, indicating adequate inventory cover and requirement-based procurement. Market participants noted that cement producers preferred flexible fuel strategies and delayed fresh bookings amid slowing seasonal demand and expectations of further price clarity.

Coking coal index eases

BigMint’s premium hard coking coal (PHCC) index eased by $1/t w-o-w to $268/t CNF Paradip as sufficient inventories and falling steel prices limited aggressive bidding from Indian mills. Market participants reported limited India-specific deals, although a July-loading cargo was concluded at $243/t FOB Australia. Australia-India Panamax freight declined by $1.3/t to $23.5/t, offering some relief. Meanwhile, Indian HRC prices stayed largely stable at INR 56,200-59,400/t, reflecting cautious, need-based buying and continued pressure on steel demand.

Imported met coke extends gains

India’s imported met coke market strengthened during the week ended 11 June, with BigMint’s assessment for Indonesian BF-grade coke (65/63 CSR) rising by $2/t w-o-w to $315/t CFR India, supported by firm Indonesian FOB offers and strong Chinese buying following coal supply disruptions. China’s sixth round of coke price hikes and tighter coking coal availability further boosted sentiment. Domestically, BF-grade coke remained stable at INR 36,700/t ex-Jajpur, western prices also stable at INR 34,000/t ex-Gandhidham. Australian PHCC prices rose to $245/t FOB, although softer pig iron demand capped upside, with Durgapur pig iron prices declining by INR 200/t to INR 37,800/t ex-works.

Petcoke market stays buyer-led

Imported petcoke prices into India softened further in June as weak cement demand, ample spot availability, and lower US Gulf Coast values weighed on sentiment. CFR India offers were heard at $132-138/t, while buyers targeted $125-130/t. Cement producers remained adequately covered and delayed purchases until August or post-monsoon periods, preferring hand-to-mouth buying. FOB USGC high-sulphur petcoke declined to the high-$70s/t amid weaker Indian demand. Meanwhile, US NAPP coal at low-to-mid $130s/t CFR continued to cap petcoke upside, prompting flexible fuel-switching decisions. Softer domestic petcoke prices added competition, although elevated freight costs and Middle East shipping risks prevented a sharper decline.

Domestic petcoke prices remain mixed

India’s domestic petcoke market witnessed mixed trends in June 2026 as refiners adopted different pricing strategies. IOCL cut prices sharply after rolling them over in May, while Nayara and CPCL also reduced offers following improving supply conditions. In contrast, BPCL raised prices due to tighter availability, and MRPL increased rates marginally. IOCL reduced road prices by INR 1,440-1,720/t, while Nayara cut prices by INR 1,670/t to INR 19,330/t. BPCL Bina and Kochi increased prices by INR 2,000/t and INR 1,500/t, respectively. MRPL raised prices by INR 270/t.

Freight market shows mixed trends

India’s dry bulk coal freight market remained mixed. Pacific sentiment weakened, with Hay Point-Paradip Panamax freight declining by $1.3/t w-o-w to $23.5/t amid limited cargo visibility and ample tonnage. In contrast, RBCT-Paradip freight edged up by $0.1/t to $21.2/t, supported by tighter prompt vessel availability and firmer South African enquiries. The East Kalimantan-Navlakhi Supramax route increased by $0.6/t to $22.4/t on balanced cargo flows and steady vessel demand. Meanwhile, the BDI fell 10.1% to 2,729, bunker prices dropped by $79/t to $713/t, Brent crude eased to $87.11/bbl, while DCE September coke futures stood at RMB 2,078/t ($306.66/t), reflecting stable sentiment in China’s steel sector.

Leave a Reply