- Bunker fuel prices ease on weaker crude, supply risks linger

- Lower bunker costs provide temporary relief to shipowners

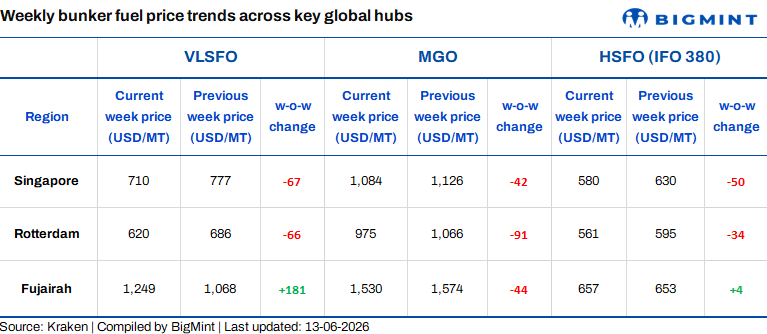

Global bunker fuel prices moved mostly lower in the week ended 13 June 2026, tracking the sharp decline in crude oil markets. Benchmark VLSFO prices in Singapore stood at $710/metric tonne (mt) on 13 June, down by $67/mt w-o-w. Falling WTI and Brent crude prices, driven by easing geopolitical concerns and expectations of improved Middle Eastern oil flows, weighed on bunker fuel values across major hubs.

Consequently, VLSFO and MGO prices declined significantly in Singapore and Rotterdam, while Fujairah remained an exception, reflecting ongoing regional supply tightness and elevated risk premiums.

The correction in bunker prices comes despite continued concerns over fuel availability in Asia. Singapore’s residual fuel inventories recently dropped to multi-year lows, highlighting underlying supply constraints that could limit further downside in marine fuel prices.

Regional bunker markets diverge amid weaker crude

- Singapore: Singapore bunker fuel sentiment weakened w-o-w as declining crude oil prices exerted downward pressure on fuel values. VLSFO prices stood at $710/mt on 13 June, down $67/mt w-o-w. Softer bunker demand from shipowners, coupled with improved fuel availability and comfortable inventories across key Asian supply hubs, further weighed on market fundamentals and led to broad-based price declines across fuel grades.

- Rotterdam: VLSFO prices stood at $620/mt, down by $66/mt w-o-w. Declining crude oil prices and broader weakness in energy markets pressured bunker values in the region. Ample fuel availability across major European hubs, coupled with cautious procurement by shipowners amid uncertain freight market conditions, further weighed on prices.

- Fujairah: Fujairah bunker fuel sentiment remained volatile and mixed w-o-w. VLSFO prices stand at $1,249/mt, up $181/mt w-o-w despite weaker crude oil values, driven by tighter prompt supply, geopolitical risk premiums, and the hub’s strategic role amid regional trade disruptions. HSFO edged higher on steady demand and balanced market conditions, while MGO softened marginally due to weaker distillate fundamentals and ample availability.

Factors influencing the decline in bunker prices

- Brent crude futures drop w-o-w: Brent crude oil (August 2026 contract) was assessed at $87.11/barrel (bbl) on 12 June, down $7.89/bbl w-o-w. The decline was driven by expectations of improved oil supply from a potential US-Iran agreement and weaker demand prospects after Organization of the Petroleum Exporting Countries (OPEC) lowered its 2026 global oil demand growth forecast.

- WTI crude decline w-o-w: WTI (West Texas Intermediate) crude futures declined by 6.25% w-o-w ($5.66/bbl) to $84.88/bbl on 13 June, compared with $90.54/bbl a week earlier. The bearish sentiment was primarily driven by growing expectations of a potential U.S.-Iran agreement, which could ease supply disruptions and improve oil flows through the Strait of Hormuz.

Lower bunker prices ease freight cost pressure

The decline in bunker prices across key global hubs is expected to provide some relief to vessel operating costs and voyage economics. Lower fuel expenses could support freight market activity by reducing cost pressures on owners and charterers, particularly in dry bulk and container segments where earnings remain sensitive to fuel fluctuations.

However, the sharp divergence between Fujairah and other hubs highlights continuing uncertainty in marine fuel markets. Regional supply disruptions and inventory tightness remain key risks that could quickly reverse the recent downward trend in bunker prices.

Outlook

Bunker prices are expected to remain volatile in the near term. While weaker crude oil fundamentals may continue to exert downward pressure on marine fuel prices, supply-side risks in the Middle East and tightening inventories in Asia could limit further declines.

Market participants will closely monitor developments in Gulf shipping routes, regional fuel availability, and global oil demand trends for clearer price direction in the coming weeks.

Leave a Reply