- HZL price cut weighs on domestic sentiment

- South Korean premiums steady, but import activity remains limited

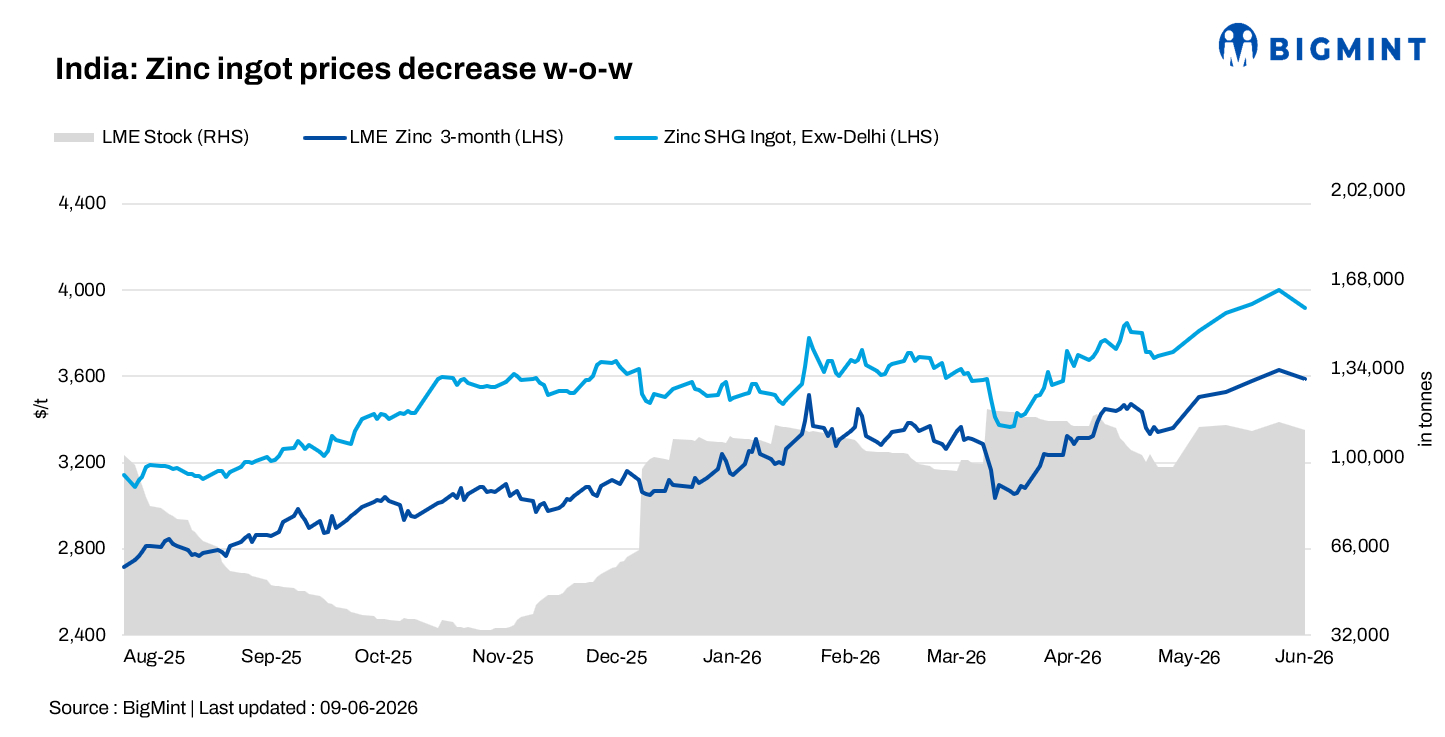

India’s zinc ingot (99.995%) prices declined w-o-w by around INR 7,700/t ($90/t) to INR 376,300/t ($4,395/t) ex-Delhi on 9 June 2026, pressured by softer global zinc prices and weaker producer pricing. Demand from galvanisers and alloy manufacturers remained largely need-based, with buyers limiting purchases to immediate requirements amid sluggish downstream consumption.

Domestic sentiment weakened after Hindustan Zinc Ltd (HZL) reduced zinc ingot prices by INR 2,300/t ($27/t) on 8 June. HZL’s benchmark SHG zinc prices were lowered to INR 381,300/t ($4,451/t), narrowing the gap with spot market levels. Meanwhile, LME three-month zinc prices eased to $3,588/t on 9 June from $3,630/t on 3 June, while cash settlement prices declined to $3,576/t. Exchange inventories fell marginally to 110,400 t from 113,300 t during the same period.

Trading activity remains cautious

Market participants reported continued need-based buying, with downstream consumers avoiding large inventory positions amid uncertain demand conditions. Domestic spot activity remained subdued despite adequate material availability across major consuming regions.

South Korean SHG zinc import premiums were heard around $250/t; however, import activity remained limited, with only a handful of traders offering overseas-origin material. Most spot transactions continued to be concluded against HZL-linked pricing, reflecting the dominance of domestic supply in the market.

Australian-origin zinc ingots were heard at around INR 380,000/t ex-Delhi, while South Korean-origin units were indicated near INR 370,000/t ex-Delhi. PMI-grade zinc was reported at around INR 331,000-332,000/t.

Alloy prices track lower zinc market

Downstream alloy prices softened in line with weaker primary zinc trends. Zamak 3 was assessed at around INR 381,000-382,000/t, while Zamak 5 was heard at INR 389,000-390,000/t ex-works.

Coated steel demand remains weak

India’s coated steel market continued to face demand pressure during the week. GP coil prices declined INR 200/t w-o-w to INR 76,500/t, while PPGI prices fell by a similar margin to INR 85,200/t. BGL prices also slipped INR 200/t to INR 89,300/t. Market participants reported sluggish bookings and weak enquiry levels, indicating limited support from zinc-consuming sectors.

Outlook

India’s zinc ingot prices are expected to remain range-bound to weak in the near term, influenced by softer LME trends and subdued downstream demand. While lower exchange inventories may provide some support to global prices, cautious buying behaviour, ample domestic availability and weak coated steel consumption are likely to cap any significant upside in the domestic market.

Leave a Reply