- Revised safeguard uncertainty keeps EU demand muted

- Logistical disruptions continue to weigh on Middle East trade flows

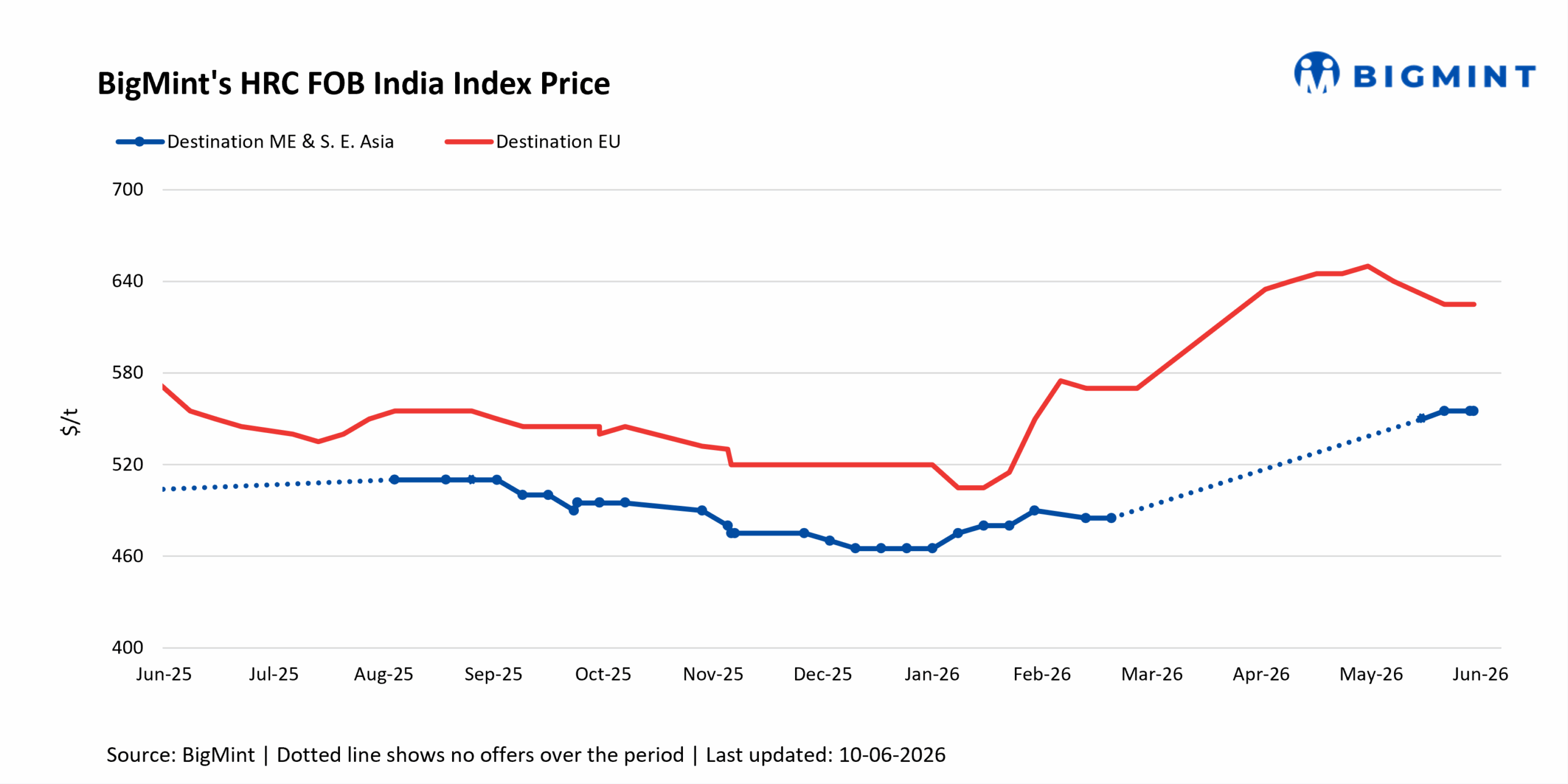

Indian HRC export activity remained subdued during the week ended 9 June 2026, as buying interest from Europe stayed muted amid uncertainty surrounding the allocation of country-specific quotas under the EU’s revised steel safeguard framework. Meanwhile, demand from the Middle East remained weak due to ongoing geopolitical tensions, elevated freight costs, and shipping disruptions, which continued to weigh on market sentiment and limit trading activity across the region.

Indian HRC export offers to the EU: Indian HRC export index to the EU remained stable w-o-w at around $625/t FOB. However, no fresh bookings were reported during the assessment period, as buyers remained cautious ahead of the implementation of the EU’s revised steel trade defence framework from 1 July 2026.

The European Council has formally approved the EU’s new steel trade defence framework, which will replace the existing steel safeguard measure from 1 July. The move is aimed at protecting the region’s steel industry from persistent global overcapacity and follows the European Parliament’s approval of the regulation last month.

Under the new framework, overall steel import quotas will be reduced by around 47% to approximately 18.3 million tonnes (mnt) compared with 2024 levels, while out-of-quota duties will increase from 25% to 50%. The revised tariff-rate quota (TRQ) system also introduces a “melt and pour” requirement to enhance traceability and prevent circumvention. In addition, a strengthened review mechanism will allow the European Commission to adjust the measures in response to evolving market conditions.

A EU-based source indicated that, “buying interest remains limited due to country wise quota-related uncertainty, and market sentiment remains cautious. Domestic market conditions are also weak, although demand is expected to recover in the coming weeks.”

HRC export offers to the Middle East: Indian HRC export index to the Middle East and Southeast Asia remained unchanged w-o-w at around $555/t FOB, with freight to Fujairah estimated at approximately $45-50/t. Similarly, Chinese HRC export offers to the region remained stable w-o-w at around $590/t CFR Jeddah.

A regional source indicated that, “market sentiment remained cautious amid persistent uncertainty in the region. Rising freight costs, delayed vessel berthing, and frequent port rerouting continued to disrupt shipments and complicate trade flows. Recent escalations between Israel and Iran have heightened concerns, with market participants closely monitoring developments amid uncertainty over the future course of the conflict and its potential repercussions for regional trade flows and logistics.”

Meanwhile, a UAE-based source noted that, “domestic market conditions remain firm, supported by restricted inflows of imported material and a steady pipeline of government-backed construction projects, which have helped sustain market confidence and foster a robust market environment.”

Outlook

Indian HRC export activity is expected to remain under pressure in the coming week, as buying interest from the EU is likely to stay subdued until greater clarity emerges regarding country-specific quota allocations. In the Middle East, ongoing logistical disruptions and elevated freight costs may continue to restrict a meaningful recovery in market activity. Overall, a gradual recovery in export activity is likely only if regulatory uncertainty eases and regional supply conditions normalise.

Leave a Reply