- Low-vol hard coking coal outperforms benchmark PHCC

- Indian steelmakers remain cautious despite sharp gains

China has re-emerged as the dominant force in the seaborne metallurgical coal market, driving a sharp rally across premium hard coking coal (PHCC), low-volatile hard coking coal (LVHCC), and pulverised coal injection (PCI) products during the first week of June (2-8 June).

Unlike previous rallies that were concentrated in benchmark premium hard coking coal, the current move has broadened across the metallurgical coal complex. Chinese steel mills and traders are actively securing a wider range of coal qualities as rising domestic coking coal prices, tighter mine supply, and successive coke price increases fuel concerns over coke quality and raw material availability.

Deal flow points to rapid market repricing

Transactions concluded between 2-5 June show how quickly the market has moved.

The progression is particularly striking in LVHCC.

Carborough Downs traded at $190/t FOB Australia on 2 June. Within three days, Curragh was sold at $215/t FOB, while Daunia moved from $201.50/t FOB to $205/t FOB in a subsequent end-user transaction.

Even allowing for quality differences, the market clearly repriced higher over the course of the week.

LVHCC leads the rally

The standout feature of the current market is the outperformance of LVHCC relative to benchmark PHCC.

While benchmark PHCC prices have strengthened, buyers are increasingly pursuing lower-volatility coals capable of improving coke strength after reaction (CSR). Market participants report that Chinese mills are actively seeking higher-quality blending coals, with demand broadening beyond traditional premium grades.

This helps explain why LVHCC, PCI, and Canadian coals have all appreciated alongside benchmark Australian PHCC.

Chinese domestic fundamentals remain supportive

The seaborne rally is being underpinned by a strengthening domestic Chinese market.

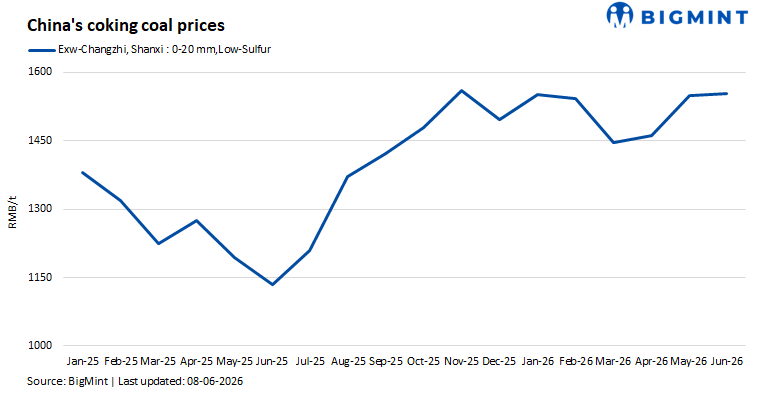

Premium low-vol coking coal prices in Shanxi’s Anze region rose by RMB 185-200/t between mid-May and the end of May amid tighter supply conditions. Market participants continue to cite stricter mine safety inspections, slower production growth and tighter availability as supporting factors.

At the same time, Chinese coke producers have already implemented five rounds of coke price increases since March and have proposed a sixth increase of RMB 50-55/t.

The importance of the coke market should not be overlooked. Rising coking coal costs are increasingly being transmitted downstream rather than absorbed entirely by coke producers, reinforcing confidence in the sustainability of current coal prices.

This trend is visible outside China as well. BigMint’s assessment of Indonesian-origin BF-grade metallurgical coke (65/63 CSR) increased by $4/t w-o-w to around $313/t CFR India, supported by firmer FOB offers, rising freight rates and strengthening replacement costs.

PCI, Canadian coals gain traction

Strength is no longer confined to premium hard coking coal.

Poitrel mid-vol PCI was traded at $168/t FOB Australia, while Russian low-vol PCI and Russian mid-vol PCI changed hands at $165/t CFR China and $155/t CFR China, respectively.

At the same time, an 85,000-t Conuma cargo was sold at $207/t FOB Canada, highlighting China’s growing willingness to source coal from alternative origins when Australian availability tightens.

The broadening of demand across LVHCC, PCI, and Canadian coals is one of the clearest signs that the rally is being driven by genuine procurement needs rather than speculative buying.

India remains on the sidelines

Perhaps the most striking feature of the rally is who is not participating.

Indian steelmakers remain cautious despite the sharp gains recorded in FOB Australia and CFR China markets. BigMint’s PHCC Index was assessed at $269/t CNF Paradip on 5 June, up only $1/t w-o-w.

Meanwhile, major Indian steelmakers rolled over June flat steel prices amid subdued market activity and cautious buying sentiment.

The contrast is stark. While LVHCC FOB Australia gained roughly $27/t within three days, the Indian delivered benchmark increased by only $1/t over the week.

India’s absence has effectively left China as the sole price-setter in the seaborne market.

Outlook

The current rally is increasingly becoming a CSR, coke, and blend-quality story.

China’s search for higher-quality coal blends, rising domestic coking coal prices, and successive coke price increases have broadened demand across PHCC, LVHCC, and PCI markets. The fact that low-vol hard coking coal, PCI, and metallurgical coke are all strengthening simultaneously suggests that the rally is being supported by conditions across the metallurgical value chain rather than by speculative coal buying alone.

The principal downside risk remains steel mill profitability. If rising raw material costs begin to force production cuts, buying activity could cool quickly. However, as long as Chinese mills continue to absorb higher coke and coal costs, the market is likely to remain well supported.

For now, China remains firmly in control of price discovery across the seaborne metallurgical coal market.

Leave a Reply