- Turkish demand weak during the Eid holiday period

- Freight challenges continue disrupting Iranian billet shipments

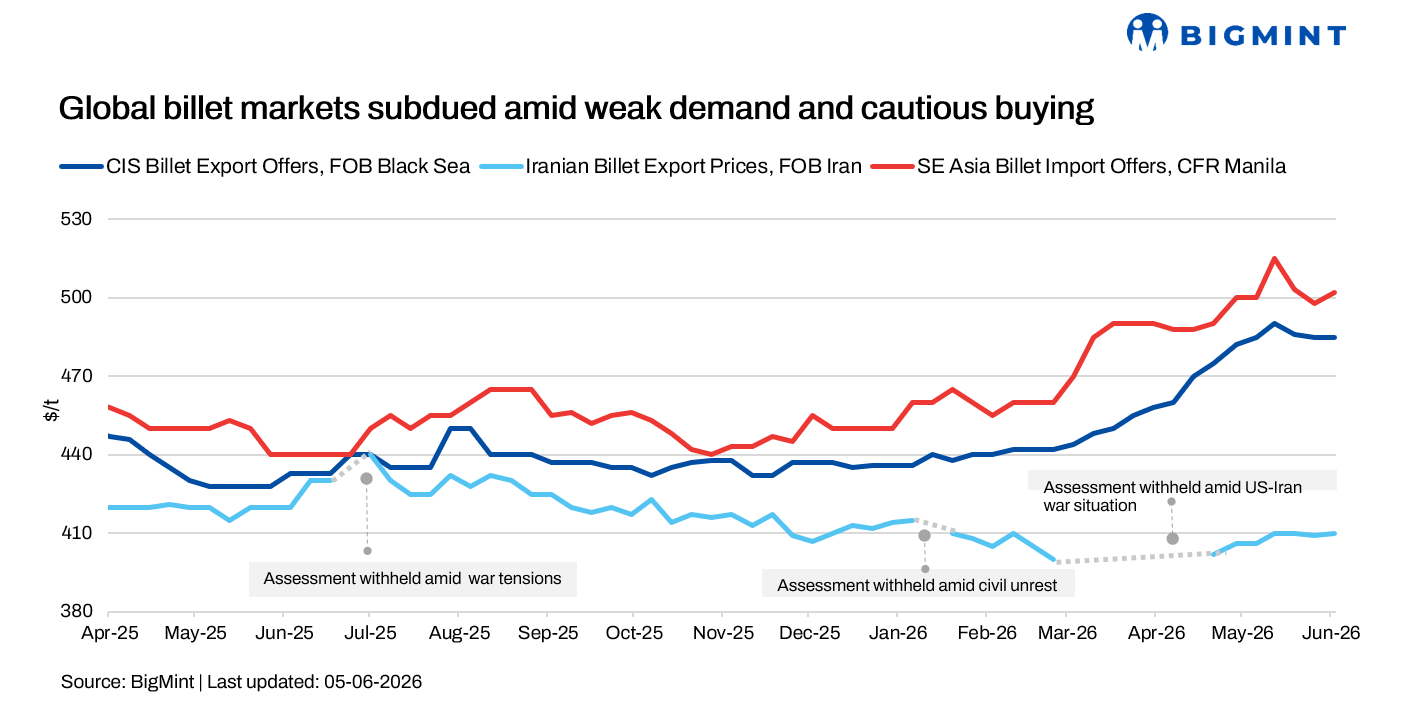

The global billet market remained under pressure during week 23, with weak steel demand, cautious buying sentiment, and seasonal factors weighing on trade activity across key regions. While higher raw material costs provided some support, sluggish downstream consumption and limited buying interest kept trading activity subdued.

In Asia, demand remained weak amid seasonal slowdowns, while the CIS market continued to face pressure from a stronger Russian rouble and muted Turkish demand. Across the Middle East region, Saudi Arabia increased its reliance on imported feedstock, Egypt’s buying activity remained subdued, and Iranian exports continued to be affected by logistical challenges and energy restrictions.

Meanwhile, the Turkish imported scrap market sentiment remained cautious, with the scrap-to-rebar spread at around $180-183/t continuing to pressure mill margins.

Export rebar offers were stable at around $590/t FOB, while billet export prices were heard at approximately $545/t FOB.

Asian billet market

Asian billet markets remained under pressure during the week amid weak steel demand, softer offers, and cautious buying activity across Southeast Asia. The onset of the rainy season in southern China further weighed on construction activity and steel consumption.

In China, billet prices remained largely stable at RMB 3,020/t ($448/t), while SHFE rebar futures rose to RMB 3,189/t ($472/t), supported by firmer raw material prices. Chinese mills largely maintained 3sp/4sp billet export offers at $474-475/t FOB, with limited pressure to reduce prices due to most export cargoes being held by traders.

Import billet offers to Indonesia were heard at $490-495/t CFR for 3sp-grade material, while open-origin 5sp billet offers remained at $500-505/t CFR. Buyers across the region continued to indicate workable levels around $490-495/t CFR amid weak steel demand.

In the Philippines, deals for 5sp billet were reported at $498-500/t CFR Manila, while seller offers remained at $502-505/t CFR. Indian induction furnace billet also emerged at around $492/t CFR, increasing competition in the market.

Meanwhile, a major Indonesian steelmaker maintained its October shipment billet offers at $485-490/t FOB. Reports also emerged of Russian billet re-entering Taiwan at around $495-498/t CFR, although available volumes were said to be limited.

Adding to the bearish sentiment, a leading Vietnamese producer reduced rebar and wire rod offers by around $10-12/t during the week. Overall, buyers continued to adopt a wait-and-watch approach amid expectations of further price corrections and subdued regional demand.

CIS billet market

The CIS billet market remained subdued during the week as the strong Russian rouble continued to restrict exporters’ pricing flexibility. Russian square billet offers for July shipment were largely stable at $485-490/t FOB Black Sea, while most mills maintained offer levels at $495-500/t FOB. Higher offers of $505-510/t FOB were also heard, although market participants indicated that tradable levels were closer to $490-492/t FOB.

Despite some weakening of the rouble during the week, Russian suppliers remained reluctant to lower prices. However, market sources noted that a further depreciation of the currency could increase pressure on mills to reduce export offers.

Demand from Turkiye remained weak following the Eid holidays, resulting in limited trading activity and largely nominal import offers. Turkish buyers continued to indicate workable billet import levels at $510-512/t CFR, equivalent to around $475-480/t FOB Black Sea, but these levels failed to attract supplier interest. Market participants noted that firm bids of $480-482/t FOB could potentially trigger sales if market conditions soften.

Trading activity in Turkiye’s billet market remained slow even after the holidays. Local producers were reported to have sold only limited volumes of semis, while import offers remained mostly nominal. Market participants indicated that only Iranian billet offers were approaching levels acceptable to Turkish buyers.

Meanwhile, Turkish domestic billet offers increased to $560-565/t exw, compared with $540-560/t exw before the holidays.

No major billet transactions were reported during the week, leaving market sentiment subdued. Market participants expect activity to improve gradually as buyers return to the market, while Turkish demand and movements in the Russian rouble remain the key factors influencing billet trade.

Gulf billet market

The Gulf billet market remained subdued during the week, with Saudi Arabia’s growing reliance on imported feedstock contrasting with weak demand in Egypt and ongoing supply constraints in Iran.

Saudi steelmakers continued to increase billet and scrap imports amid limited domestic scrap availability. India’s RINL reportedly sold 50,000-60,000 t of 3sp and 4sp billet for July shipment at $475-478/t FOB, while some producers explored scrap purchases from Europe. In the UAE, buyers continued to diversify sourcing channels, with Chinese billet imports reaching 165,000-170,000 t in Jan-Apr’26, already surpassing total 2025 volumes following new ECAS approvals for Chinese suppliers.

Egypt’s billet market remained quiet, with no fresh deals reported. Russian billet offers were stable at $482-485/t CFR, while weak downstream demand pushed domestic rebar prices down to EGP 32,000-40,000/t ($617-771/t) exw, down from EGP 35,000-40,000/t ($675-771/t) exw. Mills continued to focus on exports, with rebar offers heard at around $590/t FOB.

Meanwhile, Iran’s billet export market remained under pressure from logistics disruptions, weak regional demand, energy restrictions, and freight rates to Oman rising by nearly 50%. Export billet offers for July shipment were heard at $410-420/t FOB, while trader offers stood at $400-405/t exw. Small-volume sales to Iraq and Afghanistan were reported at $395-400/t exw. Domestic billet prices stood at 609,500 rials/kg, while EAF- and induction furnace-based billets were offered at $485-490/t DAP and $470-475/t DAP, respectively. A market participant noted that limited Iranian billet availability continued to restrict buying opportunities.

Leave a Reply