- Strait of Hormuz closure slows exports, improving domestic scrap availability

- UAE-Oman logistics integration expected to strengthen regional steel trade

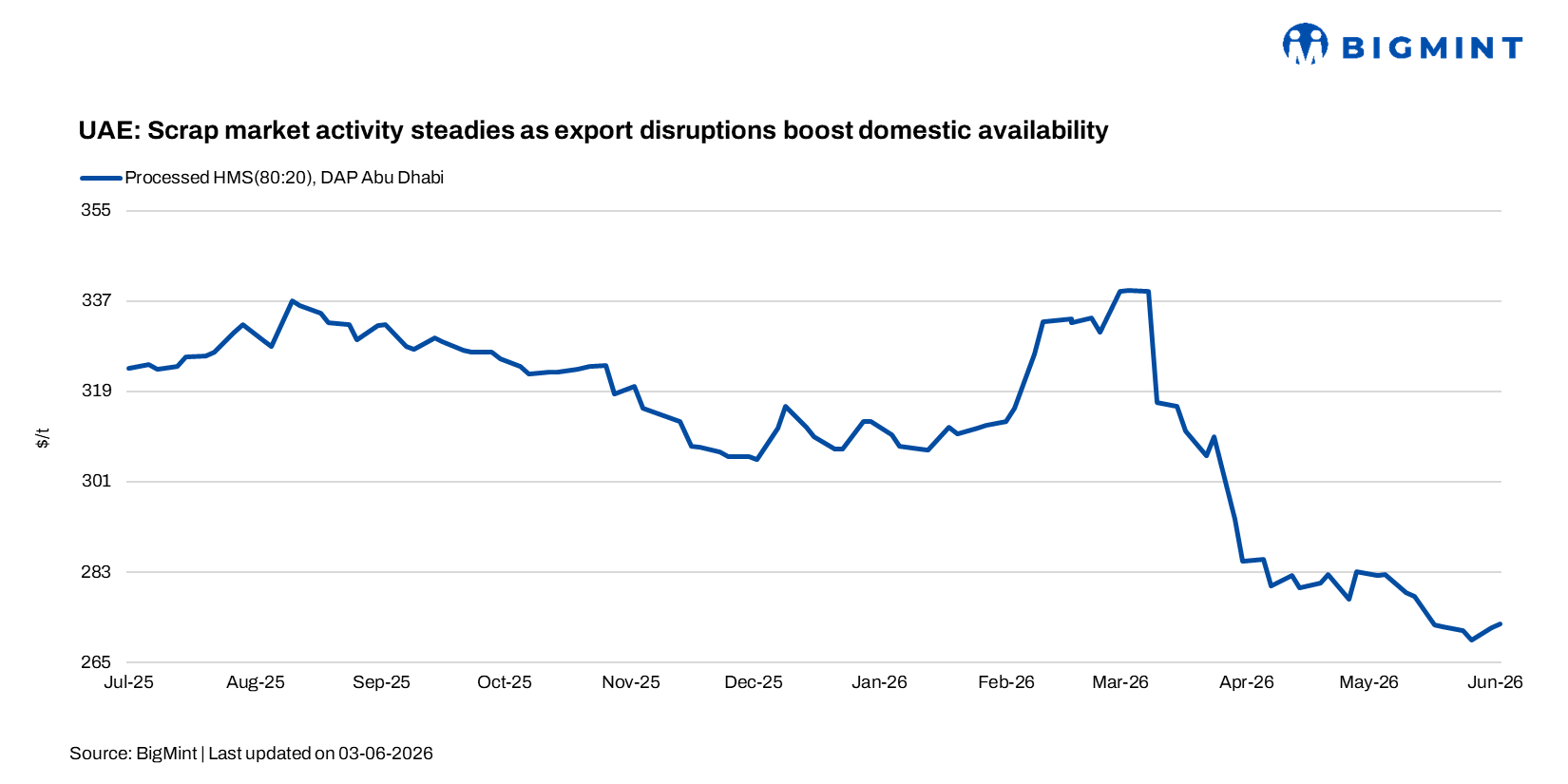

The UAE ferrous scrap market largely stabilised in the week ended 5 Jun’26 as supply and demand moved into balance following a sharp slowdown in export activity. Despite the softer export environment, domestic prices remained firm. BigMint assessed HMS (80:20) processed scrap at AED 1,002/t ($273/t) DAP Abu Dhabi, up AED 12/t ($3/t) w-o-w.

Market participants attributed the stabilisation to disruptions in regional trade flows following the closure of the Strait of Hormuz, which significantly curtailed outbound shipments and left more material available within the domestic market. The increase in local availability helped ease concerns over raw material supply and supported a more balanced trading environment.

Although some export business continued during the week, overall activity remained limited. A UAE-origin HMS cargo of 500 t was booked at $420/t CFR Qasim, while 750 t of Germany-origin loaded shredded scrap changed hands at $430/t CFR Qasim. Meanwhile, fresh offers for UAE-origin fabrication scrap were heard at $435/t CFR Qasim for 750 t cargoes with a 21-day shipment schedule.

“The export market has almost come to a standstill. Material that would normally move overseas is now being absorbed domestically, which has helped balance the market,” a UAE-based scrap trader told BigMint.

Market participants noted that domestic consumers continued to procure material regularly, helping absorb additional volumes that would otherwise have been directed towards export markets. As a result, scrap prices remained supported despite ongoing uncertainty surrounding regional shipping routes and logistics.

Delivered prices (DAP Abu Dhabi), excluding 5% VAT and based on one-week payment terms, were assessed at AED 700-740/t ($191-202/t) for LMS, AED 900-920/t ($245-251/t) for HMS (80:20), and AED 950-970/t ($259-264/t) for HMS Super.

Processed grades continued to command premiums, with HMS Sheared at AED 1,000-1,005/t ($272-274/t), HMS Shredded at AED 1,010-1,020/t ($275-278/t), and PNS Processed at AED 1,040-1,050/t ($283-286/t). Fabrication scrap was assessed at AED 1,050-1,070/t ($286-292/t) DAP Abu Dhabi.

EMSTEEL expands ES600 usage across construction sector

Supportive construction activity continues to bolster UAE steel demand, with EMSTEEL expanding the use of its ES600 high-strength rebar across residential, infrastructure, and mixed-use projects. Confirmed supply volumes have exceeded 200,000 t. According to the company, ES600 can reduce steel consumption by 18-24%, lower transportation requirements by around 15%, and cut CO₂ emissions by approximately 390 kg/t compared with conventional rebar grades. EMSTEEL CEO Saeed Ghumran Al Remeithi said the product supports the UAE’s shift towards higher-value manufacturing and advanced engineering solutions.

UAE-Oman logistics integration gains momentum

The UAE and Oman are strengthening logistics connectivity through new cargo transport incentives. Sharjah authorities have exempted trucks arriving from Oman via the Khatmat Malaha and Al Madam border crossings from toll gate fees, aiming to reduce transport costs and improve cargo movement efficiency.

The initiative is significant for the steel sector, given Khatmat Malaha’s proximity to Sohar Port, a key regional hub for steel, metallics, and raw materials. However, market participants noted that Omani producers continue to prioritise domestic demand before allocating volumes to export markets. “Domestic demand comes first. Export sales are important, but local customers remain the priority,” an Oman-based market participant said.

Outlook

UAE scrap prices are expected to remain under pressure in the coming weeks, supported by balanced domestic supply-demand fundamentals and improved local scrap availability following weaker export activity. Construction-led steel demand and ongoing infrastructure projects are likely to sustain scrap consumption, while market participants continue to monitor developments in regional logistics and trade flows.

Leave a Reply