- Weak demand persists, buyers delay purchases

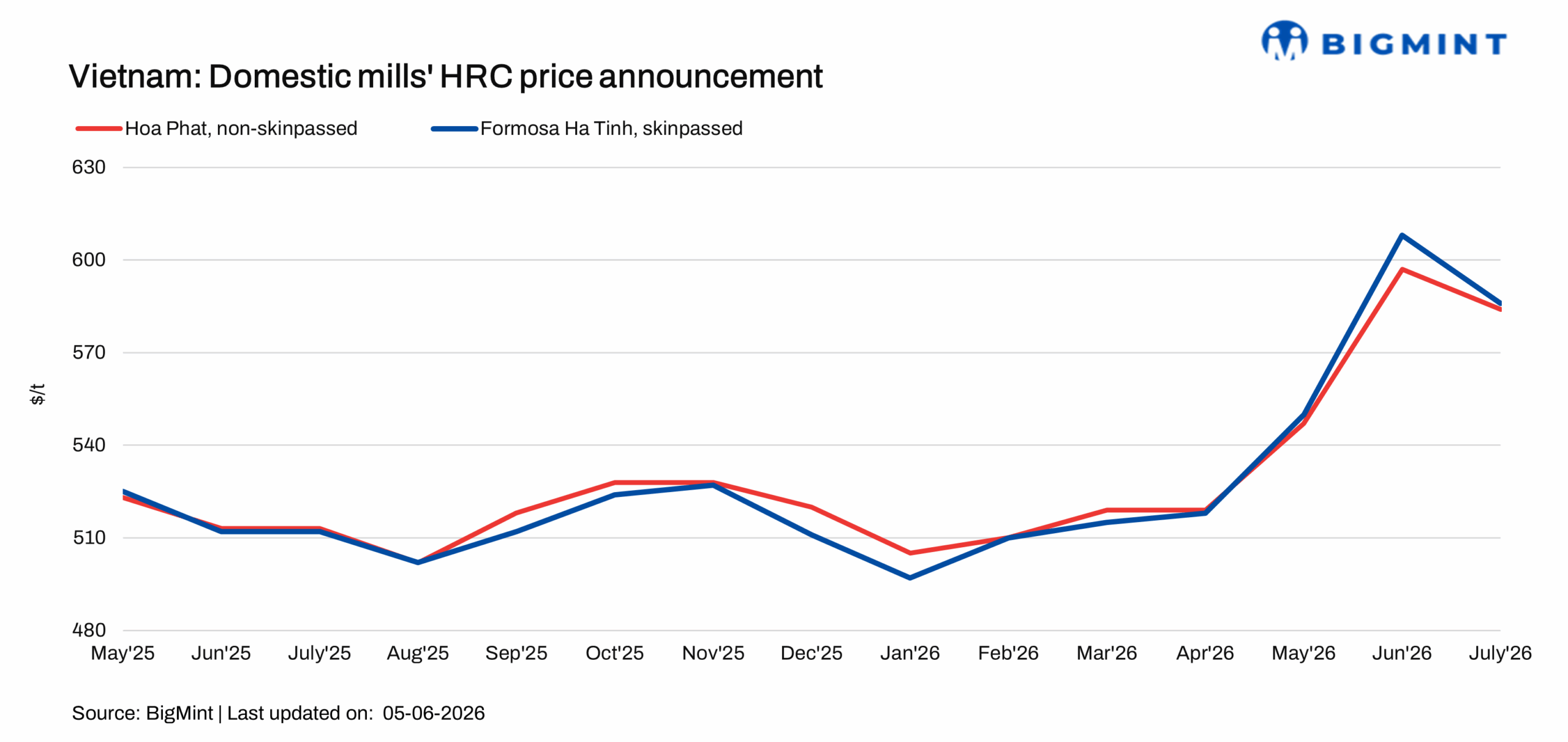

- Hoa Phat trims HRC prices m-o-m for July sales

Major Vietnamese steel producer, Formosa Ha Tinh (FHS), has reduced its hot-rolled coil (HRC) prices by around $23/t (605,237 VND/t) m-o-m for July-August 2026 shipments. Following the adjustment, FHS’s SAE1006 skin-passed HRC is now priced at approximately $585/t (VND 15,396,443/t) Ho Chi Minh City (HCMC), compared with $608/t (VND 16,001,773/t) for June 2026 sales.

Market updates

1. Hoa Phat lowers HRC prices m-o-m for July sales:

Vietnamese steel major, Hoa Phat Group, has reduced its HRC (SAE1006, non-skin-passed) prices by $13/t (VND 473,836/t) m-o-m for July 2026 sales. Following the revision, prices in the southern region were set at around $584/t (VND 15,373,336/t), excluding VAT. The price reduction was primarily driven by lower import offers in the region, which exerted downward pressure on domestic pricing. Indian HRC export offers to the region stood at around $583/t in May, with a booking of around 30,000 tonnes (t) reported at $580-585/t CFR Ho Chi Minh City for June shipment.

2. Domestic market overview:

Vietnam’s domestic HRC market remained subdued this week, as weak downstream demand and expectations of further price declines continued to weigh on buying sentiment. Overall transaction activity was limited, with buyers largely adopting a wait-and-see approach ahead of the latest monthly HRC price announcements from major domestic producers. Sluggish order inflows, cautious inventory management by traders, and muted demand from end-user sectors further dampened market sentiment, restricting overall restocking activity.

2. Vietnam’s steel imports:

Vietnam imported 1.45 mnt of steel in March, up 0.58 mnt m-o-m from 0.87 mnt in February. On a y-o-y basis, total steel imports increased by 0.22 mnt from 1.23 mnt in March. China was the largest supplier, accounting for 0.06 mnt, followed by South Korea (0.04 mnt), Australia (0.03 mnt), Indonesia (0.02 mnt), and India (0.02 mnt), while the balance was imported from other countries.

Outlook

Vietnam’s HRC market is expected to remain under pressure in the coming week as weak downstream demand and cautious purchasing sentiment continue to weigh on market sentiment. Recent price reductions by Formosa Ha Tinh and Hoa Phat are likely to reinforce buyers’ wait-and-see approach, limiting immediate restocking interest.

While lower domestic prices may improve competitiveness against imports, overall trading activity is expected to remain subdued unless demand from manufacturing and construction sectors shows a meaningful recovery. Market participants are likely to closely monitor domestic order inflows, import offer trends, and downstream consumption patterns for clearer price direction.

Leave a Reply