- Large cargo pipeline, monsoon demand risks weigh on market sentiment

- Petcoke economics, inventory drawdown to shape coal demand dynamics

India’s US Northern Appalachian (NAPP) coal market is entering a more challenging phase as falling petcoke prices begin to erode one of the key supports for imported thermal coal demand from the cement sector.

Although inventories at western Indian ports have declined from recent highs, the market remains comfortably supplied. At the same time, a substantial volume of additional US coal is scheduled to arrive during June and July, raising concerns that supply could once again outpace consumption just as the southwest monsoon begins to dampen industrial activity.

The weakening fuel economics come at a sensitive time for India’s cement industry, which is already grappling with higher logistics, packaging and energy costs. As a result, buyers appear increasingly reluctant to build fresh coal inventories, preferring instead to consume existing stocks while monitoring developments in the petcoke market.

Port inventories decline but remain elevated

Consolidated NAPP coal inventories at Kandla and Tuna ports stood at 350,950 t as of 1 June, down from a recent peak of 587,805 t recorded during the week ending 18 May.

The drawdown indicates that material continues to move into the domestic market. However, stock levels remain significant by historical standards and suggest that buyers are not facing any immediate supply constraints.

Market participants note that inventory reductions have largely been driven by routine consumption rather than aggressive restocking activity, with most end-users appearing adequately covered ahead of the monsoon season.

Weekly lifting slows as buyers turn cautious

The softer tone is also evident in weekly lifting data.

Retail lifting of US NAPP coal displayed mixed trends over the past three weeks. Lifting declined by 16% w-o-w to 94,410 t in Week 20, before rebounding sharply by 30% to 122,876 t in Week 21. However, the recovery proved short-lived, with volumes falling again by 19% w-o-w to 99,486 t in Week 22, reflecting cautious buying sentiment and adequate inventory availability among consumers.

The decline suggests that buyers are becoming increasingly selective. Many consumers are already carrying adequate fuel inventories and appear unwilling to commit to large additional purchases while prices of competing fuels continue to soften.

Incoming vessel pipeline limits upside potential

While port inventories have declined, the broader supply picture remains bearish.

Industry estimates suggest that approximately 2.5 million tonnes of US NAPP coal are either floating toward India or scheduled for arrival during June and July. This includes cargoes destined for both the retail market and large industrial consumers.

Several vessels are expected to discharge during June, ensuring a steady flow of replacement supply into the market.

The significance of this supply pipeline is that inventories could rebuild quickly if consumption slows during the monsoon period. With western India already carrying substantial stocks, importers may find themselves competing more aggressively for market share if demand weakens.

As a result, the arrival schedule is likely to remain one of the most closely watched indicators over the coming weeks.

Petcoke becomes increasingly competitive

The most immediate threat to NAPP coal demand is the sharp correction in international petcoke prices.

According to petroleum coke assessments published on 3 June, CFR India 6.5% sulphur petcoke fell to $135.50/t, down from a May monthly index of $148.75/t.

The decline of roughly $13/t in delivered Indian petcoke prices significantly improves its competitiveness against imported coal on an energy-adjusted basis.

For cement producers capable of switching fuel blends, petcoke’s higher calorific value allows operators to reduce fuel consumption per tonne of clinker produced. As the cost differential narrows, buyers are increasingly reassessing their fuel mix strategies.

Market participants across western India report that recent weakness in ex-wharf NAPP coal indications has been directly linked to lower petcoke offers.

Cement sector margins drive fuel purchasing decisions

Developments in the cement industry provide important context for understanding the current market dynamics.

According to recent industry assessments, pan-India cement prices remained broadly flat m-o-m at around INR 353/bag during May. While cement demand continued to grow at a mid-single-digit pace, producers are facing overall cost inflation estimated at INR 350-400/t, driven primarily by fuel, logistics and packaging expenses.

The recent decline in petcoke prices has helped offset part of the increase in diesel costs. However, most cement manufacturers maintain fuel inventories covering approximately 60-90 days of consumption, meaning the benefits of lower fuel costs will only gradually flow through to operating margins.

With profitability expected to face greater pressure during the monsoon-affected second quarter, buyers are showing little urgency to secure additional imported coal volumes at current prices.

Ex-wharf market sentiment softens

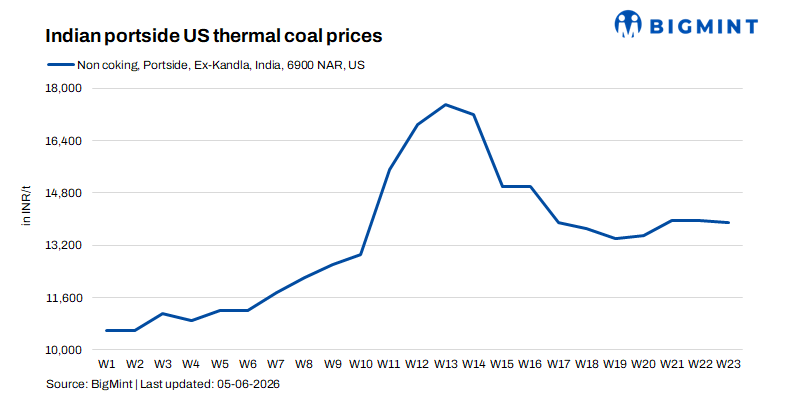

Recent market indications suggest that US NAPP coal prices at Kandla and Tuna have stabilised within a relatively narrow range of approximately INR 13,500-14,000/t.

While replacement costs and freight remain supportive, traders report that ample stock availability and softer petcoke prices are limiting upside momentum.

The market is therefore increasingly characterised by need-based buying rather than speculative inventory accumulation.

Outlook: Monsoon and petcoke remain key risks

Looking ahead, the near-term balance of risks appears tilted to the downside.

The southwest monsoon is expected to advance across key consuming regions during June, traditionally slowing construction activity and reducing cement demand. At the same time, the large incoming pipeline of US coal cargoes will continue to replenish supply.

Unless petcoke prices recover or cement demand proves stronger than expected, buyers are likely to remain cautious.

BigMint view

The Indian US NAPP coal market is moving from a period of tightness toward one of greater supply comfort. Port inventories have declined from their recent peak, but remain sufficient, while additional cargoes scheduled for June and July could quickly rebuild stocks.

The sharper concern for importers is the decline in petcoke prices. With petcoke becoming increasingly competitive on a delivered energy basis, cement producers have less incentive to aggressively replenish coal inventories. As a result, US NAPP coal prices are likely to remain under pressure through the monsoon period, with petcoke economics and the pace of inventory drawdown emerging as the two most important indicators to watch over the coming weeks.

Leave a Reply