- Dock levels down on weak buying inquiries

- Anti-dumping measures support Brazilian sentiment

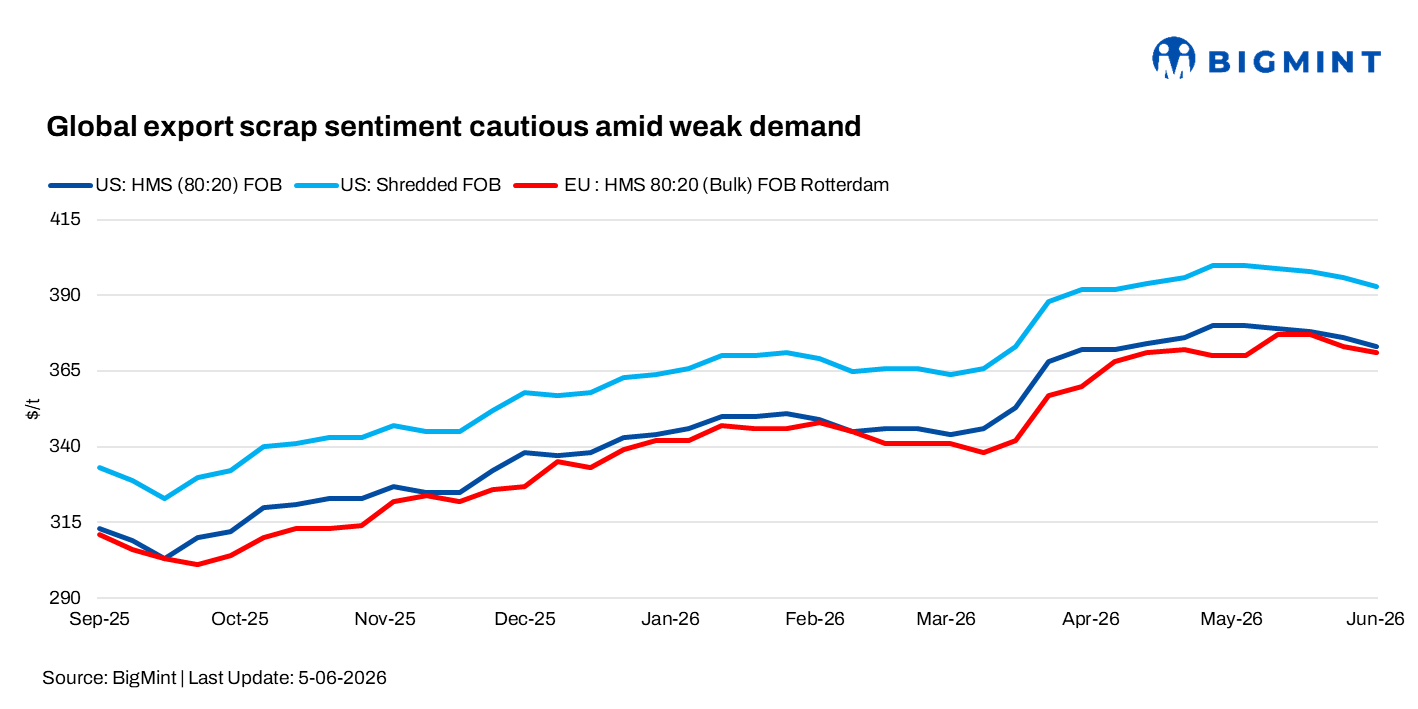

Global ferrous export scrap markets remained largely cautious during the week ending on 5 June. The US and Mexico were mostly stable amid ample supply and subdued demand, while Brazil witnessed firmer prices supported by stronger steelmaker buying.

In Europe, scrap prices remained under pressure due to weak Turkish demand and abundant material availability. Overall, cautious procurement and uncertain steel market conditions continued to influence sentiment across key regions.

US ferrous scrap market sentiment remained largely stable this week, with June settlements concluding mostly unchanged across major regions. Busheling held steady at $455-460/t DAP in both the Midwest and Southeast, while shredded scrap remained at $425-430/t DAP, plate and structural scrap at $400-405/t DAP, and HMS at $370-375/t DAP. In the export market, HMS 80:20 prices declined to $373/t FOB, while shredded scrap also softened to $393/t FOB.

Ample scrap availability and improved logistics continued to weigh on sentiment, while several mills issued cancellation notices for secondary grades amid oversupply concerns. Despite stable scrap prices, strong domestic steel fundamentals supported the market, with Midwest HRC prices reaching $1,110-1,120/t. However, rising transportation costs and weaker export demand, particularly from Turkiye, limited upside potential.

Mexico’s ferrous scrap market remained stable during the week, supported by low scrap generation despite weak steel demand. Buying interest stayed subdued, particularly in northern Mexico, where long-product mills faced slower sales and order cancellations.

Market participants said that Mexican scrap prices continue to trade at a premium to comparable US levels. In comparison, busheling in Houston was last assessed at $410/t (approximately MXN 7,083/t), resulting in a price spread of nearly MXN 900/t ($52/t).

While government infrastructure spending may support steel demand later this year, its impact is yet to be seen. Market sentiment remained cautious, with participants warning of potential price pressure if steel demand does not improve in June.

Brazil’s ferrous scrap market strengthened this week amid improved steelmaker demand and higher buying prices. HMS prices increased by BRL 50-55/t to BRL 900/t ($178/t) FOT, clean steel scrap rose by BRL 50/t to BRL 975/t ($193/t) FOT, and turnings scrap gained BRL 35/t to BRL 800/t ($158/t) FOT.

Firmer sentiment was supported by stronger steel sales following anti-dumping measures on Chinese steel imports and lower import volumes. However, the near-term outlook remained mixed amid ongoing market uncertainty.

EU scrap export prices remained under pressure on weak Turkish buying interest and abundant scrap availability. HMS 80:20 export prices softened by $2/t w-o-w to $371/t FOB, while Italian domestic/export indications were heard at EUR 330-350/t FOB for HMS 80:20 and EUR 365/t FOB for shredded scrap.

Meanwhile, dock trade levels were heard at EUR 300/t ($348/t) with workable levels at Euro 290-300/t ($336-348/t), reflecting continued pressure on collection prices. Market participants continued to monitor Turkish mills’ low bids and limited booking activity, which weighed on overall sentiment.

Leave a Reply