- Thermal coal inventories at Indian ports edge up w-o-w

- Sponge iron sentiment weakens

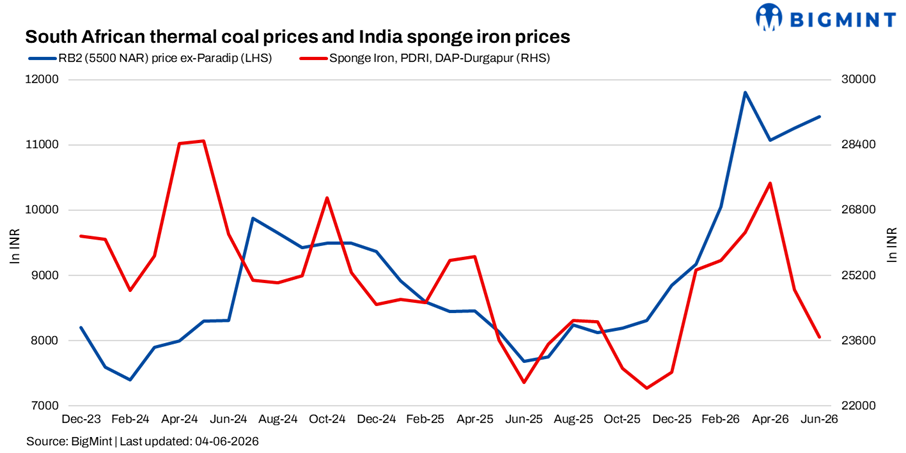

South African thermal coal sentiment remained subdued during the week despite firm global fundamentals and supply-side support. As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) increased by INR 100/t w-o-w to INR 11,500/t, while RB3 (4,800 NAR) also rose by INR 100/t to INR 9,900/t. In contrast, ex-Vizag RB2 declined by INR 150/t w-o-w to INR 11,100/t, while RB3 remained stable at INR 9,800/t.

Market participants attributed the mixed price movement to differing seller strategies. Some traders lowered offers to stimulate buying interest amid a complete absence of enquiries, while others maintained firm offer levels due to high replacement costs and concerns over losses. India’s thermal coal inventories at major ports increased marginally by 0.6% w-o-w to 15.61 mnt in week 22 from 15.53 mnt in week 21, indicating continued comfortable supply conditions despite mixed evacuation trends across ports.

High offers keep buyers away

Participants stated that the gap between buyer bids and seller expectations remained significant. Most industrial consumers continued requirement-based procurement and avoided fresh imported coal purchases due to weak downstream demand and the availability of cheaper domestic alternatives.

At Gangavaram, traders indicated firm offer levels of around INR 12,000/t for RB2 and INR 9,950/t for RB3, supported by higher freight costs, supply constraints and the recent RBCT maintenance shutdown. However, market participants reported virtually no enquiries at these levels.

Similarly, at Mangalore, RB2 offers were heard around INR 11,000/t, while RB3 offers stood near INR 10,000/t. Traders stated that higher coal and pellet costs continued pressuring sponge iron producers, forcing some plants to reduce operating rates.

Domestic coal remains preferred

Domestic coal continued exerting strong pressure on imported cargoes. Market participants reported stable domestic coal availability, supported by regular auctions and adequate supplies across key consuming regions.

Buyers largely preferred domestic coal as imported material remained uneconomical at prevailing prices. Traders noted that procurement decisions continued to focus on immediate operational requirements rather than inventory building.

BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t w-o-w.

Weak sponge iron market weighs on sentiment

Demand from the sponge iron sector remained weak. Market participants stated that current imported coal prices were difficult to absorb given prevailing steel market conditions.

PDRI DAP-Durgapur prices declined by INR 300/t w-o-w to INR 23,650/t, reflecting subdued buying activity and cautious sentiment. The finished and semi-finished steel segments also witnessed weak participation, with buyers largely staying away from fresh bookings.

Participants noted that procurement remained primarily need-based, while uncertainty surrounding steel demand and the onset of the monsoon season continued limiting market confidence.

Outlook

South African coal sentiment is expected to remain subdued in the near term as weak industrial demand and wider bid-offer disparities continue restricting trade activity. While firm FOB prices, elevated freight rates and supply-side constraints may support seller offers, meaningful buying interest is likely to remain limited unless downstream steel and sponge iron demand improves.

Leave a Reply