- Firm freights continue to restrict fresh bookings

- Weak steel demand limits aggressive procurement

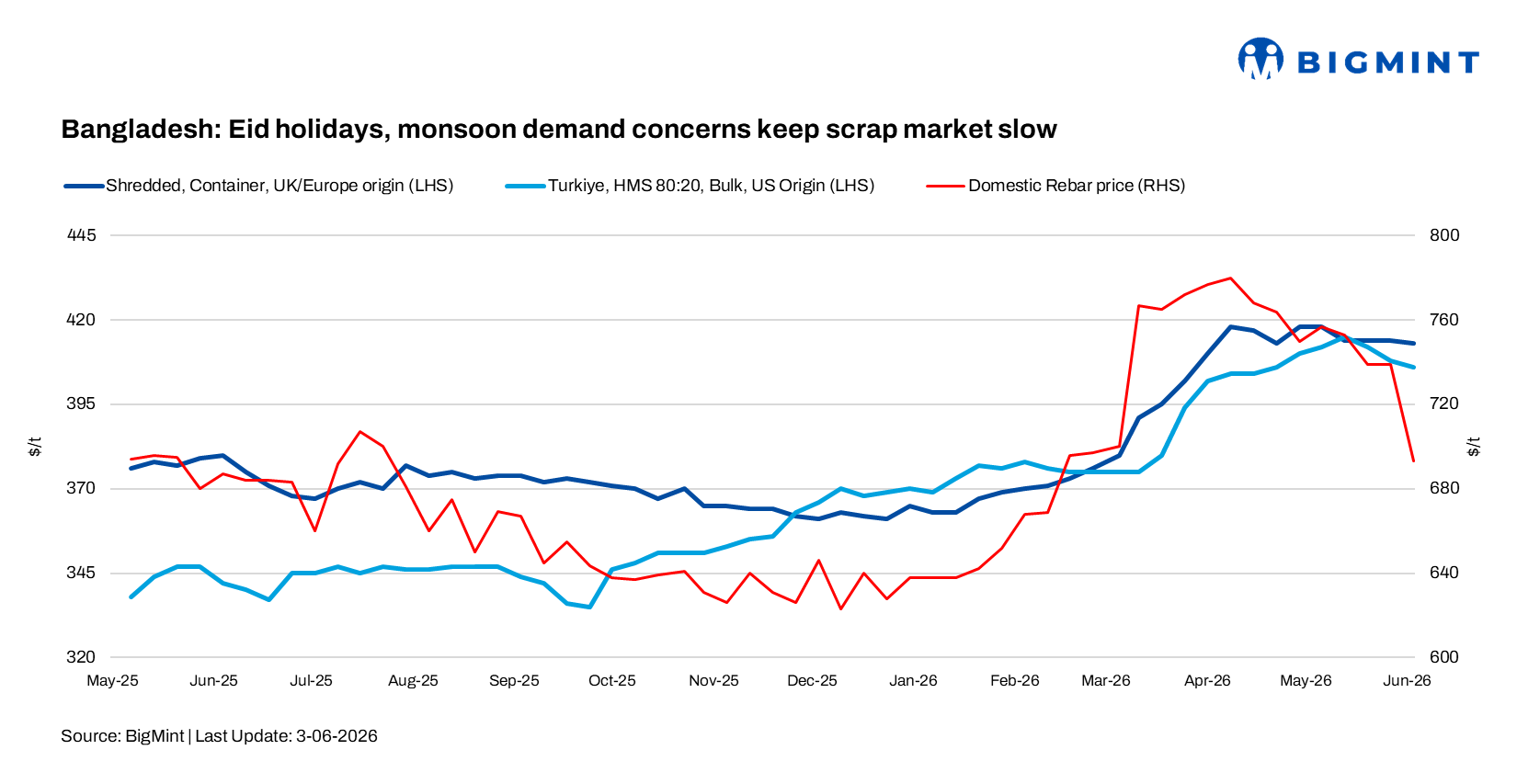

Bangladesh’s imported ferrous scrap market remained subdued during the week as buying activity slowed amid Eid al-Adha holidays, the approaching monsoon slowdown in demand, and weak downstream steel operations. Market participants noted that demand from Bangladesh remained limited during the holiday period, while mills continued purchasing only on a need-based basis.

BigMint’s weekly assessments, CFR Chattogram

- European-origin containerised HMS (80:20): $384/t down $1/t w-o-w

- European-origin containerised shredded: $413/t, stable w-o-w

- Japanese-origin bulk H2: $415/t, up by $10/t w-o-w

- US-origin bulk HMS (80:20): $412/t, up by $2/t w-o-w

Imported scrap offers remained largely stable. Australia/New Zealand-origin HMS 90:10 was heard at $405/t CFR Chattogram, while UK-origin HMS offers were heard at above $385-390/t CFR, while Japan-origin H2 scrap offers were heard at $420-425/t CFR Chattogram, while bids remain around $403-408/t.

Philippines-origin GI bundle offers were heard at $345/t CFR Chattogram, though overall fresh buying activity remained limited.

Limited deals were heard during the week. Around 2,000 t of US-origin shredded scrap were reportedly sold at $410/t CFR Chattogram, while approximately 1,000 t of Denmark-origin HMS 80:20 were booked at $390/t CFR.

Market comments

A Chattogram-based trader said, “Demand remains slow due to the Eid holidays and the upcoming monsoon season. Buyers are focusing only on prompt cargoes and workable prices.”

A Dhaka-based market participant noted, “Freight rates remain elevated, making it difficult to conclude large-volume transactions despite stable offer levels.”

Domestic market

Domestic market conditions remained soft. Local scrap prices in Dhaka were reported around BDT 49,000-51,000/t ($399-415/t). Rebar prices were heard at BDT 79,000-80,000/t ($644-652/t) in Dhaka and BDT 85,000-86,000/t ($693-701/t) in Chattogram. Market participants indicated that weak construction activity and cautious steel demand continued to weigh on mill margins.

Outlook

Bangladesh’s imported scrap market is expected to remain slow in the coming days as monsoon-related disruptions, weak steel demand, and cautious post-Eid buying sentiment continue to limit fresh bookings. While stable offer levels and firm freight rates may support prices, mills are likely to continue purchasing selectively for immediate requirements.

Leave a Reply