- Gas supply decline supports coal imports

- LNG risks strengthen coal’s role

Bangladesh’s power sector remains heavily dependent on gas, but the foundation of that model is weakening. Domestic gas production has been in structural decline, with early-2026 output falling sharply year-on-year.

The decline has forced greater reliance on LNG imports. But LNG exposes Bangladesh to three risks: price, foreign exchange availability and geopolitics.

Bangladesh strengthens thermal coal procurement

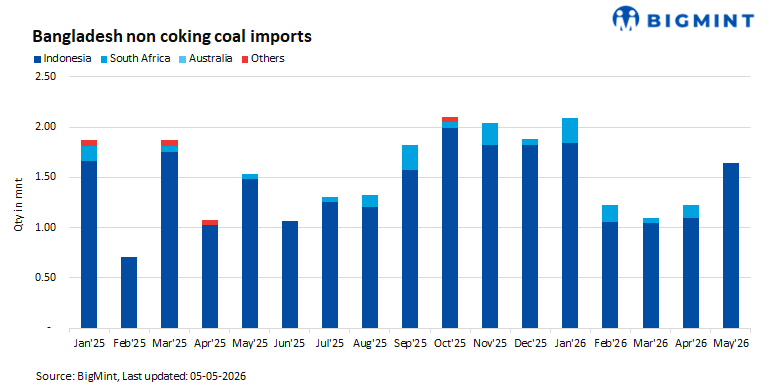

Bangladesh’s non-coking coal imports increased 34.4% m-o-m to 1.64 million tonnes (mnt) in May 2026 from 1.22 mnt in April and a 10.9% year-on-year (y-o-y) increase compared to 1.48 mnt in May 2025, according to the data maintained by BigMint. The growth was primarily driven by higher shipments from Indonesia, which supplied 1.64 mnt during the month against 1.10 mnt in April, marking a 49% m-o-m increase.

Meanwhile, no imports were recorded from South Africa, which had supplied 0.12 mnt in April. The rebound in imports underscores Bangladesh’s continued reliance on imported coal for power generation amid declining domestic gas output and ongoing uncertainty in global LNG markets.

Coal is already filling part of the gap

Coal-fired generation has become increasingly important over the past two years, with monthly coal generation consistently above 2 TWh during much of 2025 and early 2026. Imported coal-based plants such as Payra and Rampal are now key stabilisers for the grid.

Electricity imports from India also remain important, accounting for roughly 15-20% of total requirements during periods of domestic fuel stress.

LNG exposure could lift coal demand

Bangladesh’s LNG supply chain is heavily exposed to Persian Gulf flows. Any escalation in geopolitical risk around the Strait of Hormuz would increase uncertainty around LNG availability and cost.

That does not mean coal demand will spike automatically. But it does mean coal becomes the most scalable fallback fuel if LNG procurement becomes more expensive or less reliable.

Outlook

Bangladesh’s recent rise in coal imports increasingly reflects a structural shift in the country’s energy balance rather than seasonal demand alone. Domestic gas production continues declining while electricity demand rises steadily, increasing reliance on imported LNG, coal, and cross-border electricity purchases from India. However, LNG remains vulnerable to global price volatility, foreign exchange pressures, and geopolitical risks surrounding key shipping routes such as the Strait of Hormuz.

Coal is therefore emerging as a relatively more secure baseload fuel within Bangladesh’s power mix. Existing imported-coal plants such as Payra and Rampal are expected to remain critical, particularly if domestic gas shortages persist. Unlike LNG, coal can be stockpiled and sourced under longer-term contracts, improving supply security.

Going forward, Bangladesh’s thermal coal demand is likely to be driven increasingly by fuel substitution rather than purely economic growth. Indonesia is expected to retain its dominance in Bangladesh’s import basket due to freight advantages and established supply chains. Unless domestic gas production improves materially or renewable deployment accelerates sharply, Bangladesh’s coal market is likely to remain supported by long-term energy security concerns.

Leave a Reply