- Shrinking mill margins prompt switch over to pellets

- Sellers maintain export offers for upcoming deals

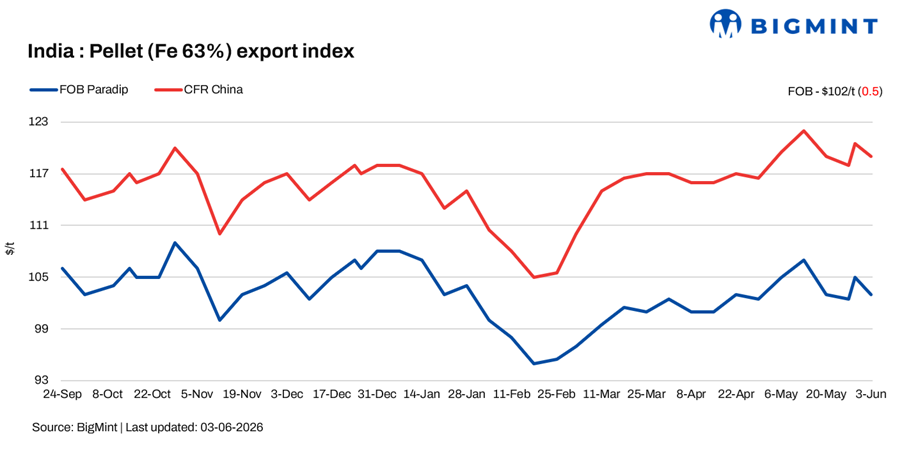

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index declined slightly by $0.5/t w-o-w to $102/t FOB east coast on 3 June against $102.5/t on 27 May 2026. However, prices declined by $3/t against the last assessment on 29 May’26. The export market witnessed active offers, with market participants attempting to capitalise on a slight decline in Chinese raw material inventories.

Weakness in the global iron ore fines market continued to weigh on overall sentiment. The recent decline in Chinese pellet inventories has maintained a window of opportunity for Indian exporters, particularly at a time when buyers are increasingly preferring pellets over iron ore fines.

Meanwhile, Chinese pellet inventories across 34 major ports stood at around 6.87 mnt, down by 0.14 mnt against 7.01 mnt recorded a week ago.

A tender was floated for high-grade pellet (Fe 66+%, Al2O3<1.5%) which received bids at $118/t FOB but sellers didn’t accept due to higher price expectations.

Rationale6

- Zero confirmed deal from India’s east coast was recorded in this publishing window for T1 trade, and, therefore, this category was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Fifteen (15) indicative prices were received, and nine (9) were considered for the calculation of the index and given a balance 100% weightage.

Market updates

Many transactions were concluded over the past two weeks, while some deals are still under negotiation with offers currently heard at around $120-122/t CFR China. Market participants said that narrowing steel mill margins and rising coke costs in China have shifted preference towards pellets, which help mills improve efficiency and maintain operating margins.

Sources informed BigMint that iron ore fines demand in the seaborne market is weak due to higher cost implications for mills, while pellets continue to attract buying interest. Sellers stated that exports are currently being used as a channel to bridge excess inventories amid limited domestic offtake.

Meanwhile, subdued conditions in India’s semi-finished steel market continued to pressure pellet makers, prompting them to actively explore overseas opportunities over the past two weeks. This has led to aggressive deal closures and sustained export enquiries.

Market participants noted that the export market has not cooled off yet, as overseas buyers continue to show interest in pellet cargoes amid weak iron ore fines demand and pressure on Chinese steel mill profitability.

Another trader said, “The recent mine accident in China has prompted a chain of coke price hikes, which in turn will curb mill margins. Thus buyers are looking to procure pellets directly over fines.”

A seller informed BigMint that pellet exports are currently helping producers liquidate inventories at a time when domestic demand remains weak.

However, buyers are currently looking bids at $116-118/t CFR level to procure normal grade Indian pellets.

Domestic vs export market

The price gap between export and domestic realisations recorded at INR 150/t this week. Export realisations (Fe 63%) were recorded at INR 7,650/t ($80.5/t) in May, reflecting a stability w-o-w amid a wider spread between the INR and the USD. Domestic realisations (Fe 62.5%) rose by INR 150/t ($1.5/t) m-o-m to INR 7,800/t ($82/t) exw.

Factors impacting pellet exports

Chinese iron ore fines prices steady w-o-w: The benchmark iron ore fines Fe 61% index remained rangebound w-o-w at $105/dmt CFR China on 2 June. Substantial stockpiles at major ports in Shandong and Tangshan reduced traders’ appetite for additional seaborne purchases. Weak import margins and lower turnaround rates further discouraged buying activity. In addition, the proposed fifth round of domestic coke price increases is expected to further squeeze steel mill margins, limiting support for higher-grade iron ore products.

DCE iron ore futures edge down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract settled at RMB 782.5/t ($116/t) on 3 June, largely rangebound w-o-w.

Vessel freights rise w-o-w: Iron ore freights increased by around $0.5/dmt w-o-w to $16/dmt on 3 June. Vessel availability on the India-China route remained tight, although fixture activity was healthy.

Outlook

Leave a Reply