- Q1 copper surplus jumps to 0.39 mnt

- Weak demand outweighs global supply risks

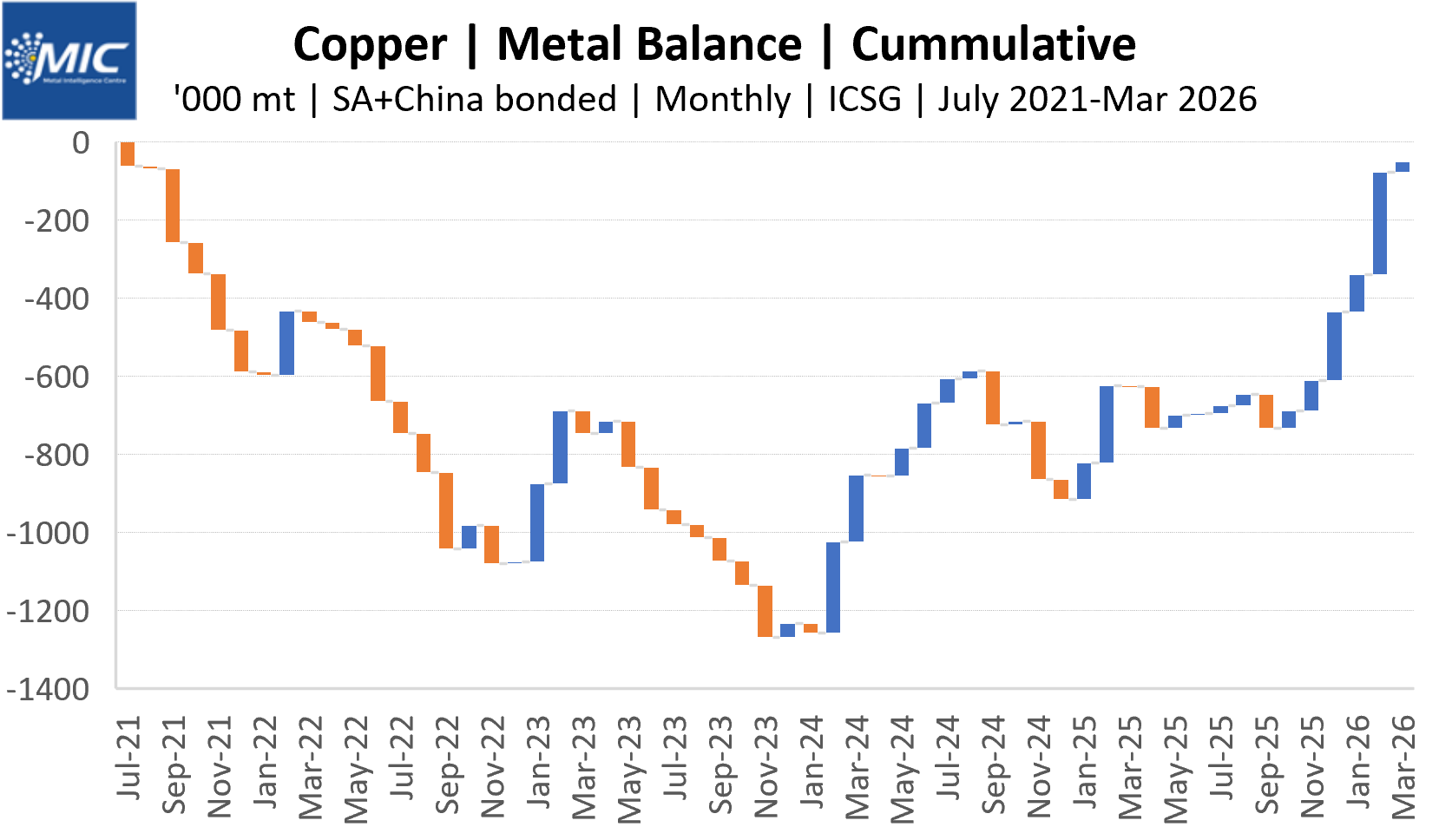

Metal Intelligence Centre: The global copper market continued to register a surplus in recent years, challenging widespread expectations of a prolonged supply deficit driven by the energy transition, rapid growth in data center investments, and disruptions across major mining regions.

According to the International Copper Study Group (ICSG), the global refined copper market recorded a surplus of 30,000 t in March 2026, marking the sixth consecutive monthly surplus. The market balance has remained largely positive since February 2024, indicating that refined copper production has consistently outpaced consumption despite concerns over tightening mine supply.

Supply disruptions fail to tighten market

Interestingly, the surplus persisted even amid significant disruptions on the supply side. Indonesia’s Grasberg copper mine, one of the world’s largest copper operations, suffered a major underground incident in September 2025, forcing operator Freeport-McMoRan to suspend operations and declare force majeure. The disruption raised concerns over potential shortages, given Grasberg’s contribution of around 3-4% of global mined copper output.

At the same time, the conflict in the Gulf has sharply increased sulphuric acid prices and disrupted sulphur shipments from the region. Since SX-EW copper production relies heavily on acid availability, concerns have emerged over potential output constraints at several African and South American operations.

Demand growth remains below expectations

Despite these supply-side challenges, the world continued to add more refined copper to the market. The primary reason has been weaker-than-anticipated demand growth, particularly from China.

Demand from China’s property and construction sectors has slowed considerably over the past few years. While investments linked to renewable energy, electric vehicles and artificial intelligence-driven data centers continue to support copper consumption, these emerging sectors have not been sufficient to offset weakness in traditional copper-consuming industries.

Surplus material

The imbalance between refined supply and demand has resulted in a steady accumulation of inventories. As a result, the market has effectively offset much of the deficit accumulated during the 2021-2023 period. Between February 2024 and March 2026, the sustained surplus environment helped rebalance the market far faster than many industry participants had anticipated.

Outlook

Looking ahead, the ICSG expects the surplus trend to continue. The group projects the global refined copper market to remain in surplus by around 96,000 t in 2026, with the surplus expected to widen further to approximately 377,000 t in 2027.

Despite ongoing supply risks and long-term demand support from the energy transition, elevated inventories and subdued consumption growth are likely to keep the copper market adequately supplied in the near term.

Note: This article has been published as part of a content partnership between MIC and BigMint.

Leave a Reply