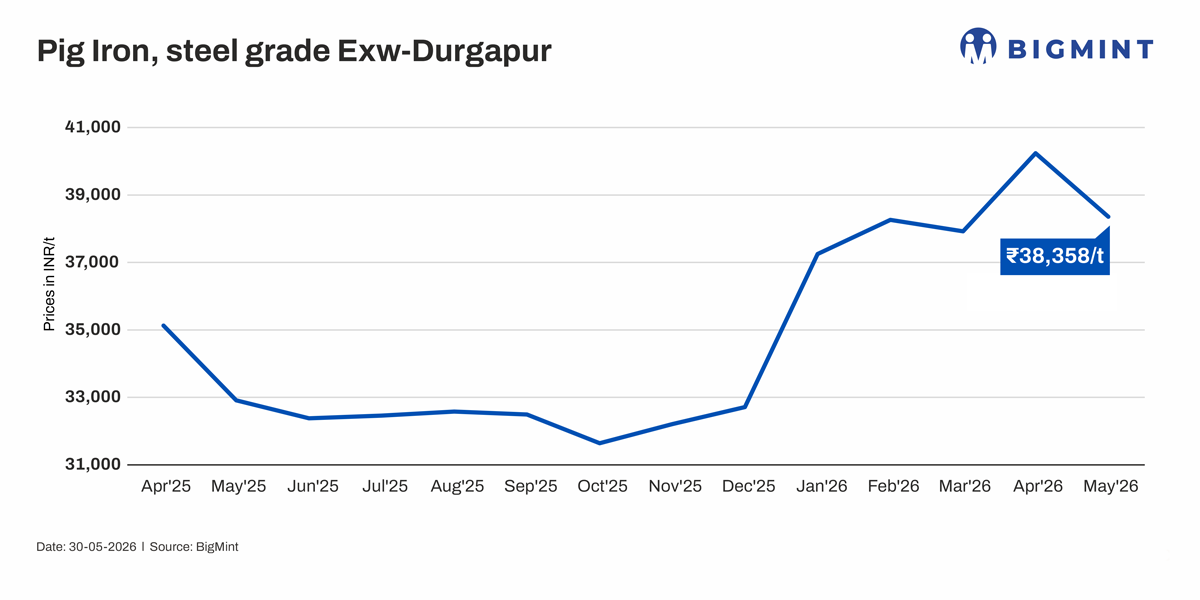

- Durgapur pig iron prices falls nearly 5% m-o-m

- Exports and supply tightness supported market fundamental

- Softer substitutes weigh on buying sentiment

India’s pig iron market remained under pressure in May 2026, with prices correcting across key regions amid weak downstream steel demand and cautious procurement activity. However, the decline remained measured as supply-side constraints, export commitments, and elevated production costs prevented a steeper fall.

The BigMint Durgapur steel-grade pig iron prices declined by around 4.7% m-o-m to INR 38,348/t from INR 40,240/t in April. Market sentiment remained subdued throughout the month as buyers restricted purchases to immediate requirements, while increasing adoption of alternative metallics further weighed on demand.

Raw material costs cushion downside

Input costs remained on higher side which keep pressure in pig iron prices although weakness in the finished steel segment. Premium hard coking coal prices increased by around $9/t m-o-m to $264/t CNF Paradip, while merchant BF-grade met coke prices rose by approximately INR 230/t to INR 36,550/t ex-Jajpur.

The increase in key raw material costs continued to exert pressure on producer margins and provided a cost floor to pig iron prices. As a result, despite weak demand fundamentals, producers remained reluctant to offer aggressive discounts, limiting the extent of price correction during the month.

Softer substitutes pressure consumption

Pig iron continued to face competition from substitute metallics. End-cutting scrap prices in Mandi Gobindgarh declined by around 3.3% m-o-m to INR 38,415/t, while Durgapur sponge iron prices witnessed a sharper correction of nearly 9.5%, falling to INR 24,851/t.

The decline in substitute prices improved their cost competitiveness and encouraged steelmakers to optimise metallic charge mixes. Consequently, pig iron procurement remained largely need-based, with buyers preferring lower-cost alternatives wherever feasible.

Auction prices reflect weakening sentiment

Auction trends mirrored the softer market conditions. The month began on a relatively firm note, with a major eastern producer’s auction clearing at around INR 40,350/t. However, realizations gradually declined as buyer participation weakened and procurement remained restricted to immediate requirements.

By month-end, auction prices had fallen to around INR 36,500/t, representing a decline of nearly INR 3,850/t from peak levels seen during the month. Increasing unsold quantities across several auctions highlighted growing buyer resistance and expectations of further corrections amid subdued consumption from foundries and steelmakers.

Exports and supply tightness support market

Export activity continued to provide crucial support to the pig iron market during May month despite subdued domestic demand. Multiple eastern-region producers concluded sizeable export transactions to the US, Türkiye, and Europe, tightening spot availability of pig iron in the domestic market. A prominent eastern India-based supplier reportedly booked around 65,000 t of steel-grade pig iron to Türkiye, while another major producer concluded nearly 55,000 t for the US market.

Robust export bookings during the March-May period helped absorb domestic volumes, restricted inventory build-up, and prevented a sharper correction in pig iron prices despite weak consumption from domestic steelmakers and foundries.

Regional market trends

Eastern India remained relatively stable compared to expectations, with prices largely holding within the INR 38,000-38,700/t range despite weak buying interest. Export commitments and restricted deliveries supported the market.

Central India witnessed relatively sharper corrections as consumers increasingly shifted toward scrap and sponge iron. However, limited availability from eastern suppliers prevented steeper declines.

Northern markets remained comparatively firm due to logistical constraints and restricted local availability. Material inflows from eastern India helped meet demand requirements and maintained market balance.

Outlook

The pig iron market is expected to remain under mild pressure in the near term as demand from steelmakers and foundries continues to remain subdued. Lower-priced substitute metallics and cautious procurement strategies are likely to weigh on buying sentiment.

However, elevated raw material costs, ongoing export commitments, and relatively balanced supply conditions are expected to restrict sharp price declines. As a result, pig iron prices are likely to remain range-bound with a slightly bearish undertone through June.

Leave a Reply