- Local sellers reduce pellet offers by INR 200/t

- Poor liquidity, sales pressure weigh on prices

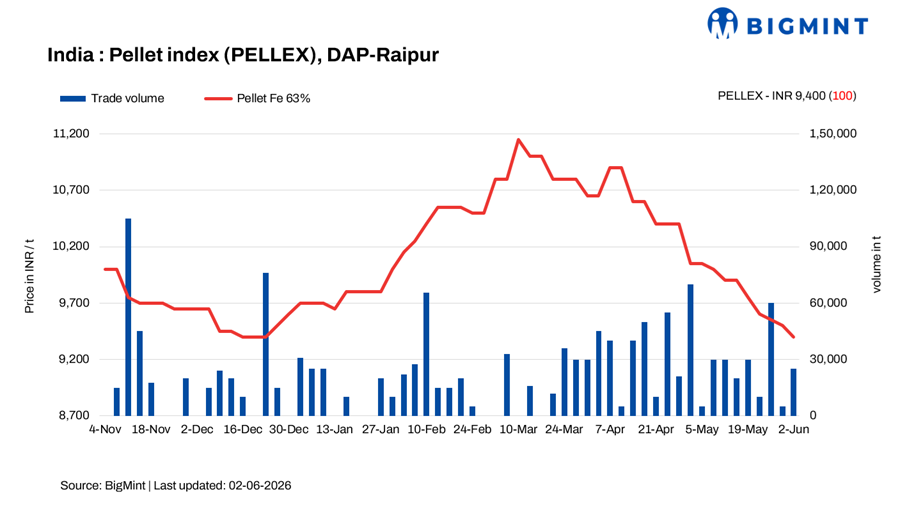

PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, inched down by INR 100/t to INR 9,400/t ($99/t) DAP on 2 June against 29 May. Deals for around 15,000 t of pellets were concluded by local pellet producers at INR 9,200-9,400/t exw in this publishing window.

Raipur pellet prices declined on Tuesday as local pellet producers reduced offers amid mounting sales pressure and subdued buying interest from steelmakers. Market participants attributed the price correction to weak downstream steel demand, declining semi-finished steel prices, and cautious procurement strategies.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- Two (2) deals were recorded in this publishing window, and one was taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Nineteen (19) firm offers, bids, and indicative prices were heard, and fourteen (14) were taken for price calculation and given the balance 50% weightage.

Price movements and offers

Pellet manufacturers in Raipur reduced offers for Fe 62.5/63% (+/-0.5%) grade pellets by INR 200/t ($2/t) to INR 9,200-9,300/t ($97-98/t) exw. Weak market sentiment following the Odisha Mining Corporation (OMC) iron ore auction and a decline in sponge and semi-finished prices led to a drop in pellet offers.

Pellet producers reduced prices after demand remained sluggish at previous offers. The decline was further influenced by falling sponge iron and billet prices, which have weakened the overall steel value chain and increased pressure on raw material markets. Sponge PDRI prices in Raipur dropped by INR 1,050/t m-o-m to INR 25,350/t ($267/t) exw in May.

Market scenario

A pellet producer based in Raipur stated, “Inquiries were limited at earlier offers as steelmakers remained reluctant to build inventories amid weak finished steel margins. The correction was necessary to stimulate buying interest and improve market liquidity.”

Steelmakers echoed similar concerns, noting that deteriorating margins in the finished steel segment have forced them to adopt a conservative procurement approach. A buyer commented, “Liquidity in the market remains tight, and current steel demand does not justify aggressive raw material purchases. Most buyers are procuring only on a need basis.”

Meanwhile, sources said that some pellet producers are exploring export opportunities to manage bulk inventories and diversify sales channels, in an effort to offset weak domestic demand.

Market participants also highlighted a notable disparity between bids and offers. A few trade discussions involving Odisha-based suppliers and Raipur-based buyers were heard during the week; however, most transactions are yet to be finalised as buyers continue to evaluate revised price levels.

Another steelmaker said, “Buyers are largely maintaining a wait-and-watch stance. The market is still assessing the sustainability of the current correction, and many participants are awaiting further signals before committing to larger volumes.”

Attention is now focused on NMDC’s upcoming iron ore price revision for June deliveries, which is expected to provide greater clarity on raw material cost trends. Market participants believe pellet prices may find firmer direction by mid-week, with some need-based transactions likely to conclude at the revised offers.

Key market drivers

- Sponge iron prices fall w-o-w: Sponge PDRI prices dropped by INR 550/t ($6/t) w-o-w to INR 24,450/t ($257/t) exw Raipur on 2 June. Prices fell by INR 200/t d-o-d, with market participants remaining in a wait-and-watch mode amid expectations of further price corrections. Procurement activity was mainly need-based, while bulk bookings remained absent across regions, reflecting cautious buyer sentiment and limited confidence in near-term demand recovery. The finished steel segment also reflected similar weakness, with dull demand and no major bulk bookings.

- Billet prices drop w-o-w: BigMint’s billet index in Raipur fell by INR 500/t ($5/t) w-o-w to INR 38,850/t ($408/t) exw on 2 June. Meanwhile, the index rose by INR 100/t ($1/t) d-o-d. Prices were supported by improved buying activity and an uptick in enquiries in the semi-finished steel segment. Cautious optimism in finished steel demand supported spot offers.

Outlook

As per BigMint’s analysis, pellet prices in Raipur are expected to remain largely stable, with some deals likely to be concluded at current offers.

Leave a Reply