- India’s imports unviable due to weak steel demand

- Post-Eid slowdown limits South Asian scrap trading

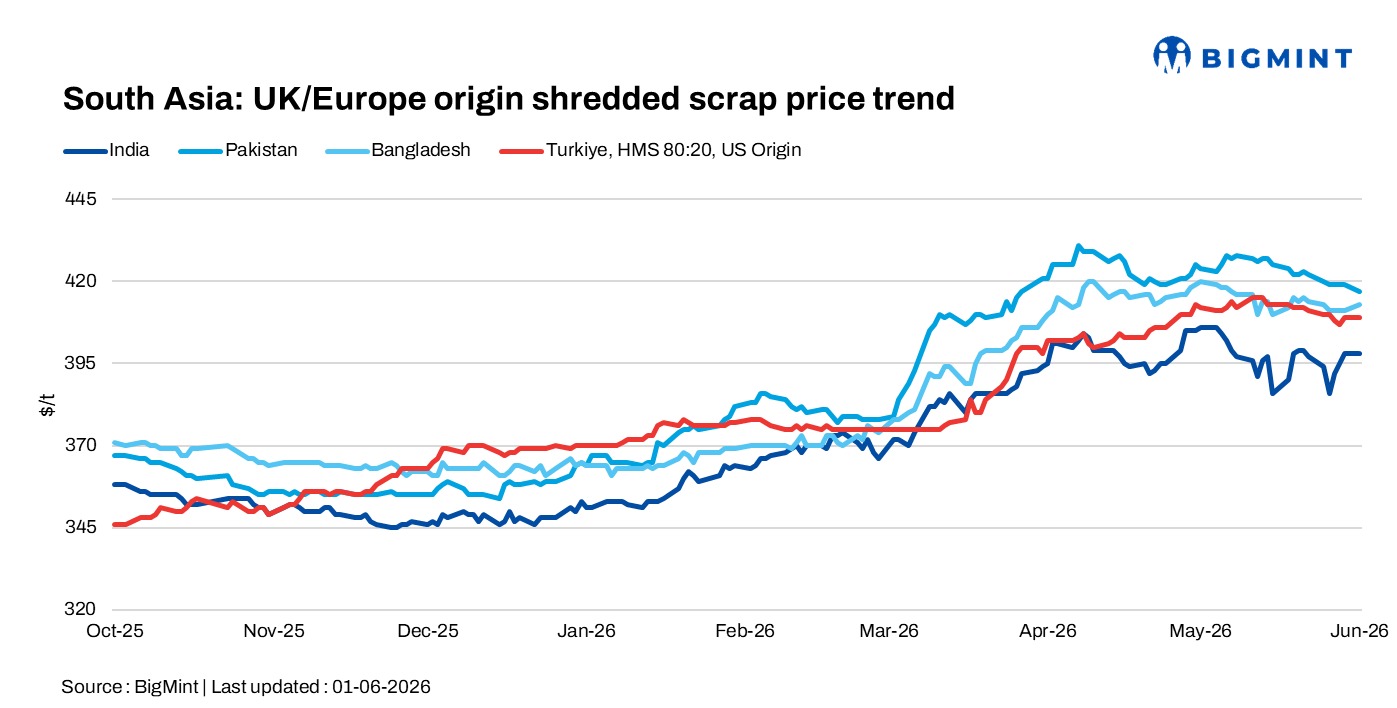

South Asian imported scrap markets remained subdued on 1 June, with weak steel demand, poor import viability, and post-Eid slowdowns continuing to limit buying activity across India, Pakistan, and Bangladesh.

India: India’s imported ferrous scrap market remained weak d-o-d, with poor steel demand and reduced mill operating rates, particularly in south India, continuing to limit buying interest. Market participants noted that imported scrap remained unviable against cheaper domestic scrap and sponge iron, while rupee depreciation further increased import costs and discouraged fresh bookings.

Trading activity remained limited, although a 500 t Brazil-origin HMS 80:20 cargo was heard booked at around $330/t CFR India. Brazil-origin HMS offers were heard at $350-355/t CFR, while UK/EU-origin HMS 80:20 offers stood near $360/t CFR and above but bids remain low, with some deals reportedly concluded below these levels. Imported shredded scrap continued to attract little buying interest due to unfavorable import economics.

Pakistan: Imported scrap prices remained largely subdued following the Eid holidays, with buying activity yet to recover meaningfully. UK-origin shredded scrap offers were heard at $420-422/t CFR, while UK/EU-origin shredded offers were indicated near $415/t CFR Pakistan. Market participants reported limited trading activity as buyers remained cautious amid weak post-holiday demand.

Bangladesh: Imported scrap market sentiment in Bangladesh remained weak as market participants gradually returned after the Eid holidays. Offer levels were heard at $415/t CFR for UK-origin shredded scrap and $385/t CFR for HMS 80:20, with no significant fresh booking activity reported.

Turkiye: Deep-sea import scrap market remained largely stable d-o-d at $408/t CFR d-o-d, as trading activity continued to be subdued during the Eid al-Adha holidays. Most mills remained absent from the market, resulting in limited fresh bookings and muted price discovery.

Turkish mills reportedly bidding at relatively low levels and market participants closely monitoring post-holiday demand. While some sources suggested that weaker Turkish buying could pressure European scrap prices in June, suppliers remained reluctant to conclude deals below $400/t CFR, helping to keep deep-sea scrap prices broadly stable.

Leave a Reply