- PAT jumps 11% on strong operational efficiencies

- Rail connectivity improvements strengthen logistics backbone

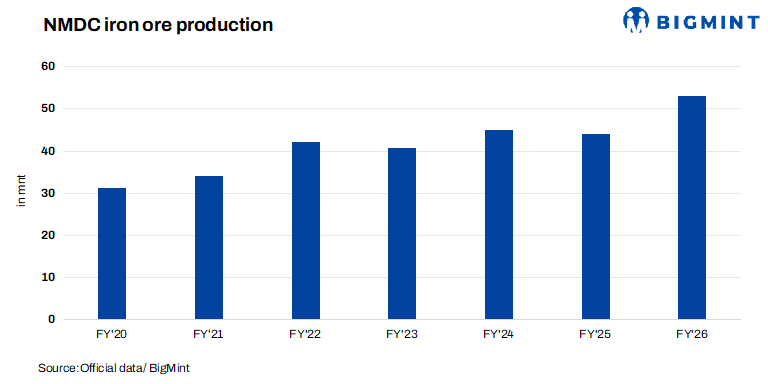

NMDC, India’s largest iron ore producer, has announced its Q4FY’26 (January-March 2026) and FY’26 results, with a robust 20% production growth in in the last fiscal year. The miner expects production in FY’27 to rise further to around 60 million tonnes (mnt).

Performance highlights

- Iron ore production rises in FY’26: The company reported FY’26 production at 53 mnt, up by 20% y-o-y against 44 mnt in FY’25. Meanwhile, iron ore production in Q4FY’26 increased by 22% y-o-y to 16.27 mnt, driven by strong operational performance across its mining complexes.

- Sales climb up in FY’26: Total iron ore sales rose by 13% to 50 mnt in FY’26. Meanwhile, sales increased by 21% y-o-y in Q4FY’26 to 15.29 mnt, demonstrating strong offtake in both domestic and export markets.

- Sales realisations increase: Average sales realisations were recorded at INR 4,921/t in FY’26, down by 4% y-o-y from INR 5,135/t in FY’25.

- EBITDA rises 9% y-o-y: The company’s EBIDTA was recorded at INR 10,737 crore in FY’26, up against INR 9,807 crore in FY’25.

- PAT increase 11% y-o-y: NMDC’s profit after tax (PAT) jumped by 11% y-o-y to INR 7,421 crore in FY’26 compared to INR 6,693 crore in FY’25, driven by operational efficiencies, steady margins, and lower input costs.

Highlights from investors’ call

- Company becomes eligible for Maharatna status: Management stated that NMDC now meets all the financial and operational criteria required for Maharatna status, reflecting its growing scale and strategic importance among Indian PSUs.

- FY27 iron ore production target set at 60 mnt: NMDC has guided for 60 mnt of iron ore production in FY’27, implying an increase of around 7 mnt over FY’26 levels through capacity enhancements and new mine additions.

- Deposit-4 expected to become a key growth driver: Commercial production from Deposit-4 is expected to begin in July 2026. Management has guided for approximately 1 mnt of production in FY’27, increasing to around 2 mnt in FY’28. Over the medium term, the mine is expected to ramp up to its rated capacity of 7 mnt/year, making it one of the company’s major production centres.

- Deposit-13 likely to commence operations during FY’27: NMDC expects to receive the remaining statutory approvals required for Deposit-13 during FY’27. Initial production is expected at around 0.5 mnt, increasing to approximately 2 mnt in the following year.

- Coal mining operations set to contribute from FY’27: NMDC’s diversification into coal mining is entering the execution phase. At the Tokisud thermal coal block in Jharkhand, overburden removal is progressing rapidly, and management expects coal extraction to begin during Q2FY’27. Production guidance for FY’27 stands at 0.75-1 mnt, opening a new revenue stream for the company.

- Rohne coking coal block to strengthen diversification strategy: Development work is underway at the Rohne coking coal block in Jharkhand, but commercial production is unlikely during FY’27 due to regulatory approvals and initial mine development requirements. Total capacity of the mine is around 8 mnt.

- Rare earth and critical minerals business gains momentum: To capitalise on India’s strategic focus on critical mineral security, NMDC has established a dedicated subsidiary focused exclusively on rare earth elements and critical minerals. Management indicated that several opportunities are being evaluated both domestically and internationally, with the objective of creating a diversified mineral portfolio beyond iron ore.

- Vizag blending hub could transform India’s iron ore market: NMDC plans to invest around INR 3,000 crore in a large-scale blending facility at Visakhapatnam. The project aims to produce standardised, branded iron ore products with consistent chemical composition.

- Railway doubling project nearing completion: The company reported substantial progress on railway infrastructure projects critical for ore evacuation. Most sections of the doubling project have already been completed, with the remaining stretches expected to be commissioned by December 2026. This will significantly improve logistics efficiency and support future production growth.

- Slurry pipeline commissioning imminent: The associated slurry pipeline network is currently undergoing pre-commissioning trials. Management expects commercial commissioning by June-July 2026, which will strengthen NMDC’s downstream value-added product portfolio. A pellet plant is also in the planning phase, but its capacity has not been decided yet.

- KIOCL targeting premium DR-grade pellet production: NMDC is working towards producing 67% Fe direct reduction (DR) grade pellets through its pellet operations. The company has already achieved 66.5% Fe quality and expects to reach DR-grade specifications shortly. Such pellets command significant premiums in international markets and can enhance profitability. KIOCL’s pellet plant produced around 2.4-2.6 mnt in FY’26 and is expected to achieve around 3-3.3 mnt in FY’27.

Leave a Reply