- Rainy season, extreme heat weighs on Vietnamese steel demand

- Demand from Bangladesh to slow during Eid holiday period

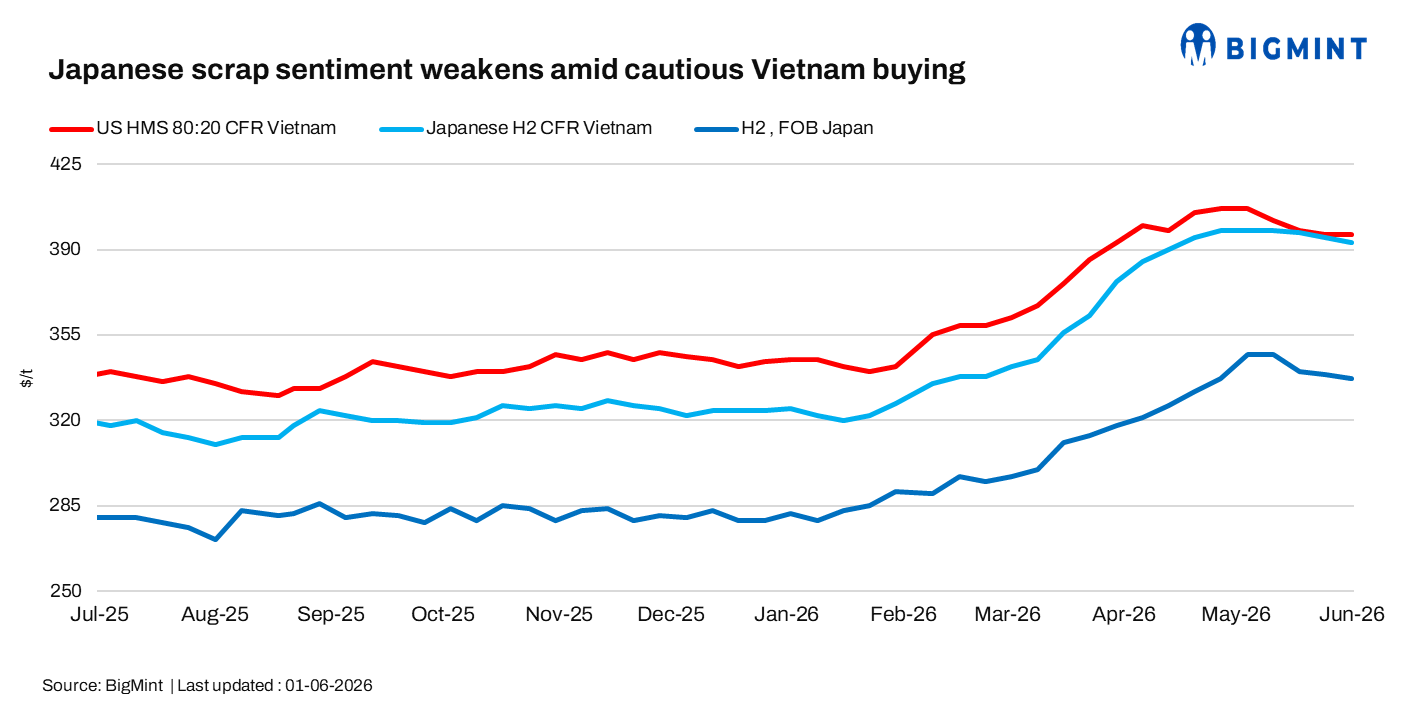

East Asian ferrous scrap markets remained slightly weaker during the week ended 1 June as cautious Vietnamese buying, a seasonal slowdown, and comfortable inventories continued pressuring import sentiment. However, Japanese domestic collection prices remained relatively stable, limiting sharper declines in export offers.

Weekly assessments

- Japanese H2 scrap was at $393/t CFR Vietnam, down by $2/t w-o-w.

- Japanese H2 scrap was at JPY 53,800/t ($337/t) FOB Tokyo Bay, down by JPY 100/t ($1/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $396/t CFR Vietnam, stable w-o-w.

Japan

Japanese scrap export sentiment softened during the week as Vietnamese buyers stayed cautious amid weak rainy-season steel demand. H2 offers to Vietnam were heard at $396-402/t CFR, with the lowest offers down around $2/t w-o-w.

Heavy rains and extreme heat in Vietnam continued to weigh on construction activity and steel demand, keeping buyers cautious amid weak rebar margins and expectations of further price declines. Meanwhile, a wide bid-offer gap persisted, with Japanese H2 scrap bids heard at $375-390/t CFR Vietnam, well below prevailing offers.

Meanwhile, Japan’s domestic market remained relatively stable, supported by firm collection prices. H2 FAS collection prices were heard steady at JPY 54,000-55,000/t ($339-345/t), while H2 export prices were assessed at JPY 53,800/t ($337/t) FOB Tokyo Bay, down JPY 100/t ($1/t) w-o-w.

Sources also noted that Japan’s export market may face additional pressure in the upcoming days due to slower buying activity from Bangladesh during the Eid holiday period, potentially affecting regional pricing sentiment.

Vietnam

Vietnamese mills remained cautious during the week as several buyers had already secured sufficient bulk scrap cargoes for upcoming shipment requirements. Weak downstream steel demand, comfortable inventories, and seasonal weather disruptions continued limiting fresh import activity.

Deep-sea scrap prices remained largely stable. US-origin and Australian-origin HMS 80:20 offers were both heard at around $400/t CFR Vietnam, unchanged w-o-w, while bids were heard near $395/t CFR.

Buyers continued preferring smaller Japan-origin cargoes while monitoring market direction and waiting for additional price corrections before returning to the market aggressively.

Outlook

BigMint expects East Asian scrap markets to remain under mild pressure in the upcoming days amid cautious Vietnamese procurement, seasonal slowdown during the rainy season, and sufficient inventory levels. However, relatively firm Japanese domestic collection prices and stable deep-sea offers are likely to prevent any sharp decline in export prices.

Leave a Reply