- Middle East steel market softens during Eid holidays

- Strong rouble continues pressuring Black Sea exporters

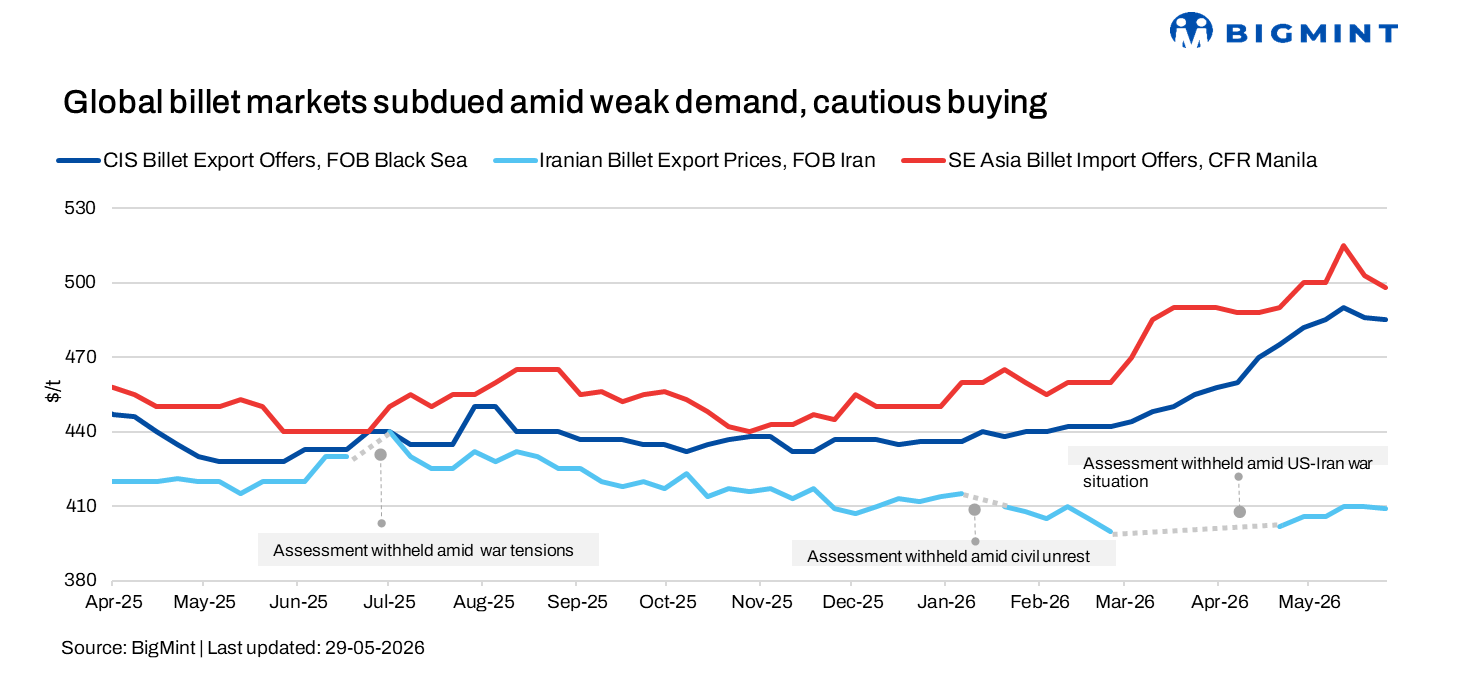

Global billet markets remained subdued during the week ended 30 May 2026, as weak steel demand, cautious buying sentiment, and geopolitical uncertainties weighed on trading activity across Asia, the CIS/Black Sea region, and the Middle East.

Chinese billet export prices softened amid weaker domestic sentiment and sluggish construction activity. CIS/Black Sea billet prices edged lower due to limited Turkish buying interest and a stronger Russian rouble, while Iran’s billet market remained pressured by power shortages, logistical disruptions, and regional tensions despite restricted supply supporting offer levels.

Turkiye’s deep-sea imported scrap market also softened slightly ahead of the Eid al-Adha holidays. Mills delayed bookings despite June cargo requirements, as weak rebar demand, tight liquidity, and a narrow scrap-to-rebar spread of $178-182/t continued to pressure margins. Softer Chinese billet prices, lower freight rates, and a weaker euro further strengthened buyers’ negotiating position.

Asian billet market

Asian billet markets remained under pressure during the week, with Chinese export billet prices declining amid weaker domestic sentiment, sluggish downstream steel demand, and cautious buying interest across key import markets.

Chinese 3sp billet export offers eased to around $472/t FOB for July-August shipments, down by $4-5/t w-o-w. In the finished steel segment, Asian rebar markets remained subdued, with softer Chinese export offers, weak construction activity, and adverse weather conditions continuing to weigh on demand across the region.

Chinese domestic billet prices fell to RMB 3,010/t ($444/t) amid weak downstream demand and slow inventory digestion. However, SHFE rebar futures edged up to RMB 3,157/t ($466/t), supported by cost-side strength despite subdued steel market fundamentals.

Market participants noted that most buyers adopted a wait-and-watch approach, delaying purchases in anticipation of further price corrections and clearer market direction. Export trading activity remained limited, with bids scarce across major Southeast Asian destinations.

In Southeast Asia, billet offers continued to soften, with open-origin 5sp billet heard at $500-505/t CFR. Chinese 5sp billet offers to the Philippines declined to $495-498/t CFR, while 3sp billet offers to Taiwan slipped to $495-500/t CFR. Buyers in Taiwan indicated workable levels closer to $490-495/t CFR, with no fresh deals reported.

Meanwhile, Indonesia’s major steel mill maintained billet offers at $490-495/t FOB for September shipment, although trading activity remained limited due to weak finished steel demand and sufficient buyer inventories.

In contrast to the weaker billet market, Taiwan’s scrap segment remained relatively firm, with containerised US-origin HMS 80:20 bookings concluded at $360-365/t CFR, slightly higher w-o-w.

CIS/Black Sea billet market

CIS/Black Sea billet prices softened during the week amid weak buying interest from Turkiye and limited trading activity. Export billet offers were heard around $485-488/t FOB Black Sea (equivalent to $515-520/t CFR Turkiye), while buyers targeted lower workable levels near $475-480/t FOB or $505-510/t CFR Turkiye.

Market participants noted that the continued strength of the Russian rouble and elevated production costs constrained exporters’ ability to offer discounts. Several suppliers indicated that current market conditions made sales above $490-492/t FOB Black Sea difficult, despite some mills targeting higher price levels.

Market participants noted that mill target prices of around $500/t FOB Black Sea remained difficult to achieve under prevailing demand conditions. Limited offer availability was also reported as exporters struggled with reduced margins due to the stronger rouble.

Meanwhile, Chinese billet offers to Turkiye softened by around $10-15/t w-o-w to $525-530/t CFR for July-August shipment, adding further pressure to CIS-origin material.

Turkish import billet prices were assessed around $510-515/t CFR, while CIS export billet prices were heard near $488-490/t FOB Black Sea, both declining slightly w-o-w amid subdued demand and cautious buyer sentiment.

Iran/MENA billet market

Iran’s billet market remained under pressure during the week amid ongoing geopolitical tensions, logistics disruptions, electricity shortages, and weak domestic demand. Export billet offers were largely stable at $409-410/t FOB, supported by constrained supply despite cautious buying activity ahead of the Eid holiday period.

Market participants noted that power restrictions continued limiting steel production, helping mills maintain firm offer levels. DRI offers were reported near $240/t FOB Bandar Abbas, while currency volatility and ongoing uncertainty surrounding the Strait of Hormuz continued disrupting trade flows and payment channels.

Despite current challenges, Iran maintained a diversified export presence, exporting more than 1.8 million tonnes of billet during the Persian year 2025-26. The Middle East remained the largest destination with 0.98 mnt, followed by Africa with 0.44 mnt shipped to Ghana, while exports to Afghanistan reached 0.24 mnt and shipments to Turkiye exceeded 0.1 mnt.

Market participants expect Iranian billet prices to remain broadly stable in the coming weeks, supported by supply constraints and electricity-related production disruptions, although weak demand and ongoing geopolitical risks are likely to limit trading activity.

Leave a Reply