- Rice prices rose across most East African markets during April

- Uganda and Rwanda see gains, in Tanzania prices soften on fresh supplies

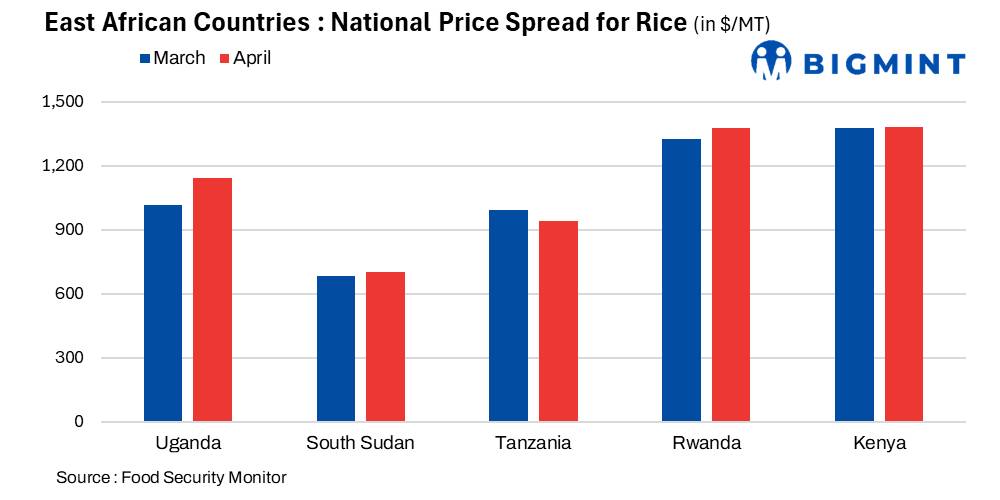

Rice markets across East Africa remained largely firm during April 2026, with most countries recording higher m-o-m prices amid tightening domestic supplies, rising freight costs, fuel inflation, currency weakness, and continued dependence on imported Asian rice from India, Pakistan, Thailand, and Vietnam. Kenya and Rwanda remained the highest-priced markets in the region, while Uganda recorded the sharpest monthly increase. Tanzania, however, witnessed a decline due to fresh harvest arrivals and easing supply pressure.

Uganda records strongest monthly rise

Uganda witnessed the sharpest increase among the tracked markets, with average rice prices rising from around $1,014/tonne (t) in March to nearly $1,142/t in April, up about 13% m-o-m. The rise was driven by tightening domestic supplies, strong regional demand, and higher transportation costs. Rising fuel prices further increased inland logistics and distribution expenses. Uganda’s Kaiso rice variety also gained around 14.6% over three months and more than 21% over six months, reflecting sustained supply-side pressure.

Rwanda prices remain structurally high

Rwanda continued to remain among East Africa’s costliest rice markets, with prices increasing from around $1,323/t to nearly $1,376/t during April. The increase was supported by localized supply tightness, high transport costs, and heavy dependence on imported rice. Limited domestic production capacity has kept Rwanda vulnerable to international price fluctuations and freight volatility. Prices also rose nearly 25.5% over six months and more than 33% y-o-y, indicating persistent inflationary pressure.

Kenya remains highest-priced market

Kenya’s rice prices edged up slightly from around $1,376/t to nearly $1,382/t during April. Although the increase was marginal, prices remained elevated due to import dependence, rising fuel prices, expensive inland logistics, and currency pressure. Strong consumer demand and relatively tight inventories also prevented any major price correction despite ongoing imports.

Tanzania prices soften on improved supplies

Unlike neighbouring markets, Tanzania recorded a decline in rice prices, falling from nearly $992/t in March to around $939/t in April, down about 5%. Improved domestic availability following fresh harvest arrivals and favourable crop conditions helped ease market pressure and improve wholesale supply. However, prices remain supported over the medium term due to active cross-border demand from neighboring deficit markets.

South Sudan prices supported by logistics constraints

South Sudan witnessed a moderate increase in rice prices, rising from around $685/t to nearly $702/t during April. High transaction costs, logistical bottlenecks, and dependence on imports from Uganda and Sudan continued to support prices despite relatively weak purchasing power.

Fuel, freight and import dependence drive prices

Higher crude oil prices, fuel inflation, elevated trucking costs, and expensive container movement significantly increased rice import and distribution costs across East Africa. Weaker local currencies against the US dollar further raised landed rice prices.

The region remains highly dependent on imported rice, particularly from India, Pakistan, Thailand, and Vietnam. As a result, fluctuations in Asian FOB prices, freight movement, export policy, and currency trends continue to directly influence East African rice markets. India remains the dominant supplier due to competitive pricing in non-basmati, parboiled, and broken rice segments.

Outlook

Rice prices across East Africa are expected to remain firm in the near term, especially in structurally deficit markets such as Kenya, Rwanda, and Uganda. Market direction will depend on fresh harvest arrivals, Asian import flows, freight rates, fuel prices, and currency stability. While improved supplies in Tanzania may provide temporary regional relief, continued import dependence and high logistics costs are likely to keep markets sensitive to global price volatility.

Leave a Reply