- European scrap prices supported by tight supply

- Weak export activity limits Brazilian market growth

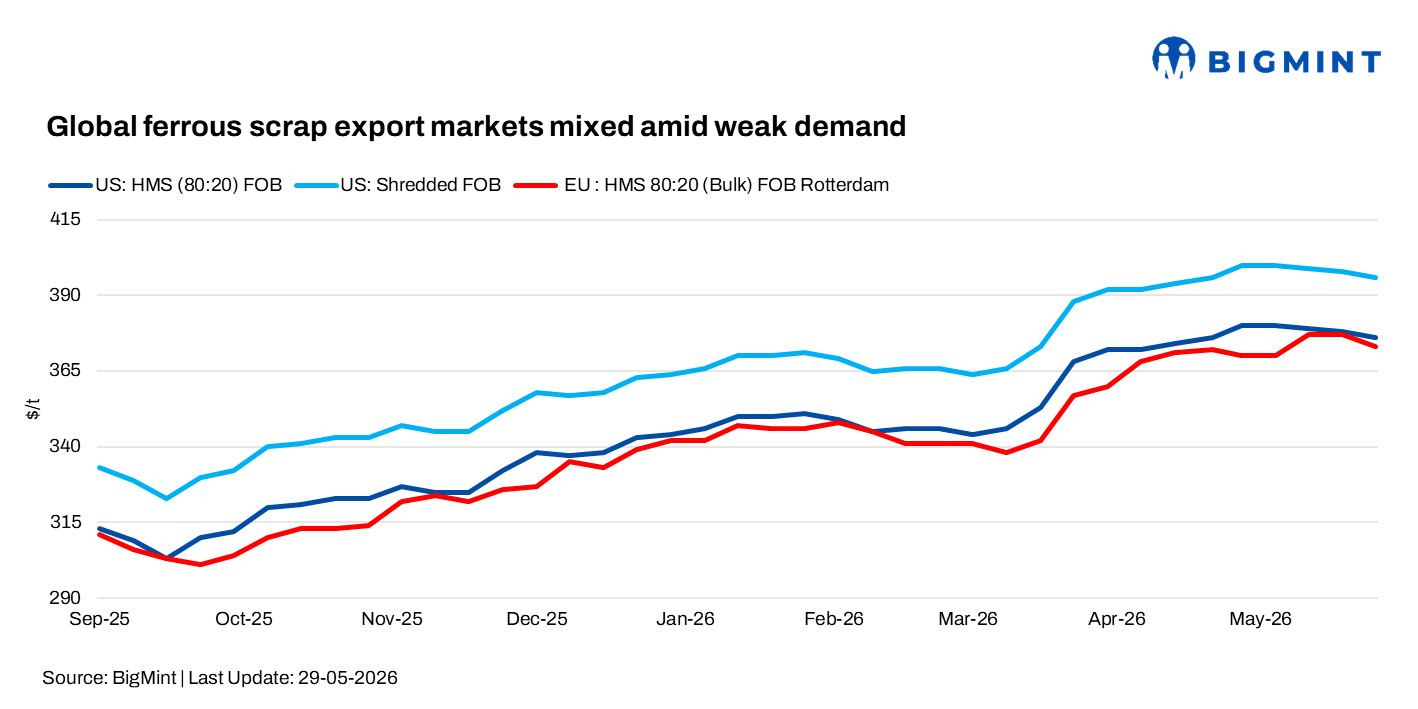

Global ferrous export scrap markets witnessed mixed trends during the week ended on 29 May, as softer export demand and improving scrap availability pressured US obsolete scrap prices, while European markets remained comparatively firm due to tight collection flows, stable mill demand, and ongoing logistics disruptions.

Meanwhile, Brazil’s scrap market stayed largely stable, supported by unchanged steelmaker buying prices despite continued pressure on recycler margins and subdued export activity.

US ferrous scrap markets softened slightly during the week, with export prices for obsolete grades declining modestly. US export HMS 80:20 prices fell to around $376/t FOB, while shredded scrap prices eased to nearly $396/t FOB.

In the domestic market, Midwest shredded scrap prices remained steady around $430/t DAP, while busheling held firm near $460/t DAP amid stronger flat steel demand and elevated pig iron prices. High scrap grades remained supported as mills increasingly substituted costly imported pig iron with busheling, although planned sheet mill outages may slightly pressure June demand.

Export demand remained weak, particularly from Turkiye, where mills struggled to match firm US offer levels amid sluggish rebar demand and continued lira depreciation. As a result, some exporters increasingly shifted focus toward the domestic market.

Higher seasonal scrap generation and abundant obsolete scrap supply restrained upward momentum in HMS and shredded grades. With supply conditions remaining comfortable, market participants expect the US scrap market to witness a slight softening in the coming days.

European ferrous scrap markets remained firm, supported by steady steel mill demand, tight scrap availability, and elevated logistics costs. German E3 (HMS 80:20) scrap prices increased to around Euro 310-315/t ($360-365/t) exw, while Italian scrap prices rose to approximately Euro 340-345/t ($394-400/t) exw.

Market participants noted that high mill utilisation rates and constrained availability of high-grade scrap continued to underpin prices across the region, offsetting the impact of subdued construction-sector demand.

Meanwhile, Benelux dockside HMS 80:20 prices remained stable at around Euro 290-295/t ($336-342/t) DAP. Similarly, UK dockside scrap prices held steady w-o-w at Euro 295-305/t ($342-354/t), supported by balanced domestic conditions. Ongoing logistics challenges, including railway maintenance works, elevated transportation costs, and low river water levels restricting barge movements in Germany, continued to hamper scrap flows across Europe and lend support to market prices.

Looking ahead, market participants expect the European scrap market to remain relatively firm in the near term. However, subdued export demand and improving seasonal scrap collection could temper further price increases.

Brazil‘s ferrous scrap market remained stable during the week, despite recyclers seeking higher prices amid tight collection margins and volatile procurement conditions. Steelmakers largely maintained unchanged purchase prices.

HMS 80:20 held at BRL 845-855/t ($168-170/t) FOT, turnings scrap at BRL 765-770/t ($152-153/t) FOT, and clean steel scrap at BRL 925-930/t ($183-184/t) FOT. Export activity remained subdued, with HMS 80:20 stable at $310-315/t FOB and shredded scrap at $330-335/t FOB. Weak export demand and compressed trading margins continued to limit fresh bookings.

Market participants expect the Brazilian scrap market to remain broadly stable in the coming weeks, supported by tight collection economics but constrained by weak domestic and export demand.

Leave a Reply