- Fallling US coal production fails to support prices

- Weak demand, high inventories weigh on market

The US Northern Appalachian (NAPP) thermal coal market is facing increasing competition in India’s cement sector, challenged by a recent decline in petcoke prices.

While US coal production continues to weaken, tightening supply alone is no longer enough to sustain competitiveness in India’s cement industry. Instead, procurement decisions are increasingly being driven by a narrower question: which fuel delivers the best kiln economics?

For Indian cement manufacturers — particularly across western and northern India — the answer has become less clear-cut in recent weeks.

US NAPP coal, prized for its high calorific value and consistent combustion profile, remains a preferred fuel for many cement producers. However, softer petcoke prices are narrowing the economic advantage that had supported stronger NAPP demand over the past year, prompting several plants to reassess fuel blends.

Why NAPP became India’s preferred imported cement fuel

US NAPP coal has carved out a strong position in India’s cement industry over the past decade, particularly after cement producers sought alternatives to expensive or operationally challenging fuels.

Unlike lower-calorific Indonesian thermal coal, NAPP coal imported into India typically offers an energy content of around 6,900 NCV, making it one of the highest-calorific thermal coals regularly consumed in the cement sector. Its superior heat profile, relatively low ash, and lower sulphur content compared with petcoke have made it especially attractive for kiln operations.

For cement manufacturers, fuel selection is not simply a price decision. Stable flame characteristics, kiln temperature management, clinker quality, ash chemistry, and emissions compliance all influence procurement strategies.

In this context, NAPP coal has historically occupied a sweet spot — offering significantly higher energy than conventional thermal coal while avoiding some of the operational challenges associated with high-sulphur petcoke. That positioning, however, is facing renewed pressure.

Petcoke correction reshapes fuel economics

After remaining elevated for much of the year, US Gulf Coast (USGC) petcoke prices have corrected sharply, narrowing the delivered-cost advantage that had previously favoured NAPP coal.

Recent petcoke cargoes into India were reportedly concluded at around $137-145/t CFR India, while fresh offers have eased into the mid-$130s/t range, with buyers seeking levels closer to the low-$130s/t. Meanwhile, US NAPP cargoes for July-September loading are currently being offered at around $90/t FOB Baltimore, with freight to west coast India estimated near $45/t, implying replacement costs close to $135/t CFR India before financing and inland costs.

At first glance, landed prices between the two fuels now appear increasingly comparable. Yet the competition is more complex than headline pricing.

Because petcoke typically carries a calorific value of around 7,500 kcal/kg, it still delivers more energy per tonne than NAPP coal. This means that when price spreads narrow, cement plants often begin increasing petcoke blending ratios to improve fuel efficiency.

However, NAPP coal’s higher operational flexibility and lower sulphur profile mean it is rarely displaced outright. Instead, the market tends to adjust through optimisation.

“Industry is tending more towards petcoke now after the correction in petcoke prices, and US coal needs to correct further if it has to maintain its competitiveness in the cement industry,” a market participant indicated.

The implication is not necessarily a collapse in NAPP demand but rather a rebalancing of fuel mixes, particularly among cost-sensitive cement producers.

India’s retail market points to softer sentiment

Market indications across India suggest the imported US coal market is already beginning to feel pressure from weaker buying interest.

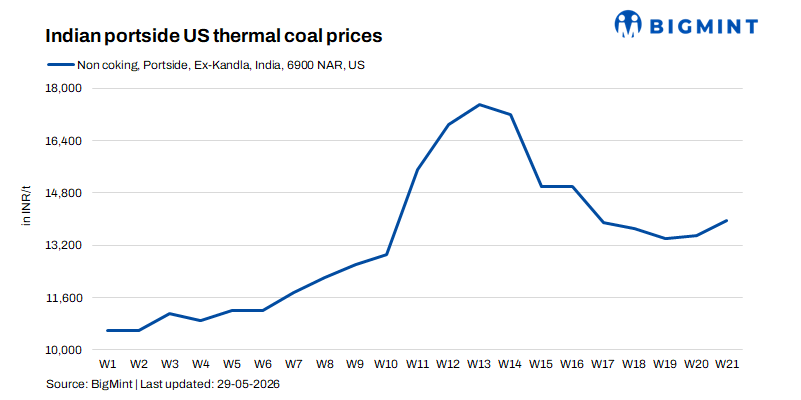

Retail market indications for imported US thermal coal largely hovered around INR 13,200-14,000/t exw during the second half of May, with traders repeatedly pointing to ample availability, subdued demand, and cautious buying interest from industrial consumers. As per BigMint’s assessment of Non coking coal, Portside US (6900 NAR) Kandla rosed by INR 450/t w-o-w to INR 13,950/t.

Several market participants described enquiries as muted amid weak cement demand and rising competition from domestic coal auctions.

Some traders also pointed to an increasingly crowded market, with multiple vessels continuing to discharge into west coast ports even as consumption remained measured.

Stocks remain elevated despite stronger lifting

The physical market continues to reflect signs of comfortable availability.

Port stocks of NAPP coal at Kandla and Tuna stood at around 450,737 t as of 25 May, down from approximately 587,805 t a week earlier, although inventories remain elevated relative to early May levels. Weekly lifting improved to around 122,876 t during Week 21, compared with roughly 94,410 t in Week 20, indicating that buyers have returned selectively as prices softened.

Major importers and distributors continue to hold significant inventory positions, suggesting traders are still working through cargoes booked when delivered economics appeared more favourable.

The rise in lifting offers some encouragement for suppliers, but not enough to signal a decisive market recovery.

Lower US output offers limited support

Ironically, the pressure on NAPP coal in India is emerging despite continued weakness in US coal production. US coal output slipped again in April to around 37-38 mnt, reflecting persistent weakness across Appalachian and Powder River regions and reinforcing the longer-term structural decline in US coal supply. Historically, such tightening would have supported export prices.

But today’s market operates differently. For exporters targeting India, competition is increasingly determined by destination-specific fuel economics rather than supply scarcity alone. Even premium coals such as NAPP must compete not only against seaborne thermal coal, but also against petcoke, domestic linkage coal, auction coal, and alternate kiln fuels.

Outlook

The near-term outlook for US NAPP coal in India will hinge largely on petcoke pricing, freight costs, and cement demand recovery after the monsoon.

If petcoke prices remain in the low-to-mid $130s/t CFR India range, cement producers are likely to continue optimising blends toward higher petcoke usage wherever operationally feasible.

However, NAPP coal’s premium heat value, lower sulphur profile, and kiln-friendly characteristics mean it is unlikely to lose relevance in India’s cement sector.

Leave a Reply