- Rupee depreciation, costly cargoes slow import market activity

- Rising inventories, robust domestic supply reduce demand

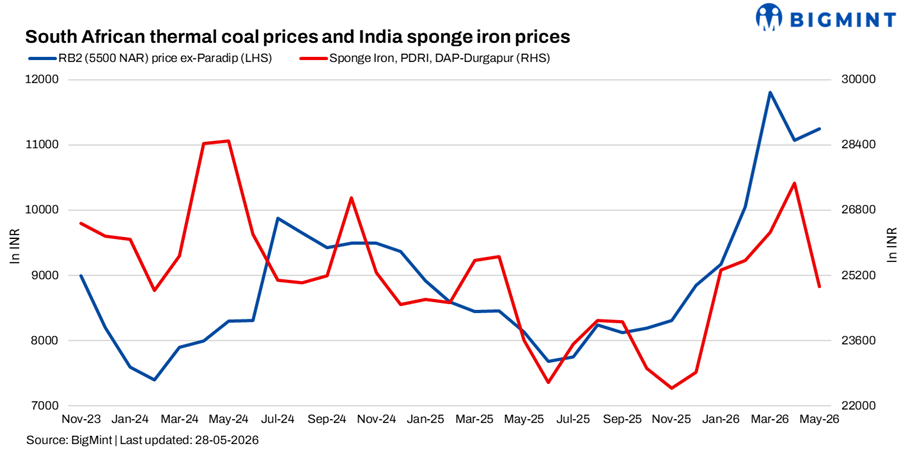

South African thermal coal trade at Indian ports remained sluggish during the week amid limited enquiries, comfortable domestic coal availability, and cautious industrial buying sentiment. Market participants stated that overall activity remained slow, with very few trade conversions. As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) prices remained stable w-o-w at around INR 11,400/t, while RB3 (4,800 NAR) prices were also heard steady near INR 9,800/t. Traders indicated that higher replacement costs of imported cargoes continued to support offers. However, actual buying interest remained weak as domestic coal remained significantly cheaper for industrial consumers.

Bid-offer disparities limit trading activity

Participants stated that the market largely remained at a standstill during the week, with no major movement compared with previous sessions. At Gangavaram, traders indicated offer levels near INR 12,000/t for RB2 cargoes to align with replacement costs, although buyers were unwilling to accept such levels amid subdued downstream demand. Traders also mentioned seeking delivery extensions as movement of imported cargoes remained extremely slow at ports.

“INR has depreciated against the US dollar, and is at $95.9-96.3 levels this week. This has raised the landed cost of imports, making domestic substitutes preferable. Additionally, previous shipments booked at higher prices due to elevated freights are arriving now. Thus, offers remain high; this, coupled with low bids, has limited trade activities,” said a source.

Several market participants stated that there were currently no fresh enquiries in the market and therefore no aggressive offers were being placed. At Vizag port, material availability remained high, and traders continued offering cargoes at similar levels without successful trade conversion. Bid-offer disparities widened further during the week as buyers continued resisting higher imported coal prices while sellers remained reluctant to reduce offers sharply due to elevated procurement costs.

Robust domestic coal supply reduces import demand

Domestic coal availability continued to exert pressure on imported South African coal demand. BigMint assessed domestic 5,000 GCV coal prices stable around INR 5,500/t, while 4,500 GCV coal prices declined by around INR 50/t w-o-w to nearly INR 4,050/t. Frequent domestic coal auctions and comfortable supply availability continued reducing urgency for imported coal bookings across sponge iron and steel sectors.

Portside inventories rise

India’s thermal coal inventories at major ports increased 2.4% w-o-w in Week 21 to 15.53 mnt from 15.16 mnt in Week 20, with fresh cargo arrivals at select western ports despite weak downstream demand conditions. Market participants stated that overall supply remained comfortable as sponge iron, steel and cement sectors continued limiting aggressive procurement activity ahead of the monsoon season.

Sponge iron sentiment improves slightly

Meanwhile, sponge iron market sentiment improved slightly during the week. PDRI DAP-Durgapur prices remained stable w-o-w at INR 23,950/t supported by better buying activity. Participants stated that enquiry levels improved across central and eastern regions, while steelmakers were seen procuring raw materials more actively compared with previous weeks. However, procurement activity largely remained requirement-based amid prevailing market uncertainties.

Outlook

Market participants indicated that unless downstream steel demand improves significantly, imported South African coal trade is likely to remain slow in the near term. Comfortable domestic coal availability, high inventories and cautious industrial sentiment are expected to continue limiting aggressive imported coal procurement across Indian markets.

Leave a Reply