- Benchmark prices inch down by INR 100/t w-o-w

- Purchases limited to urgent requirements

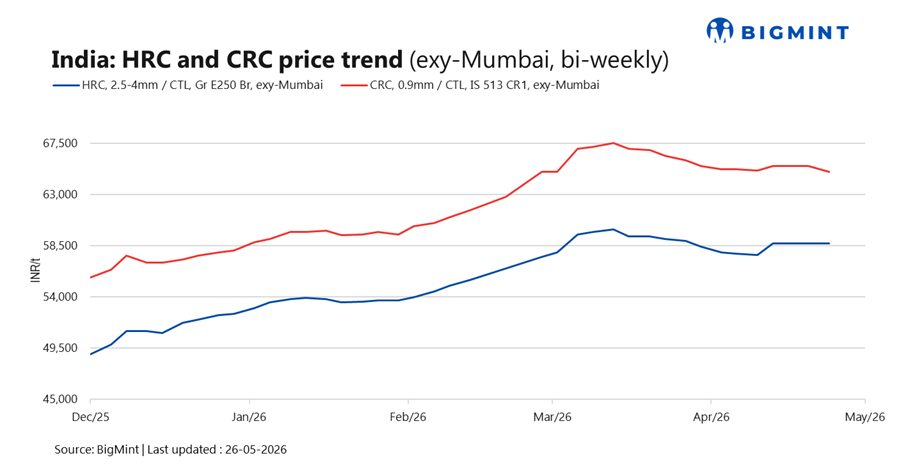

Trade-level prices of hot-rolled coils (HRC) in India remained range-bound in the week ending 26 May, with HRC prices assessed in the range of INR 56,500-59,500/t ($591-622/t) and cold-rolled coil (CRC) prices assessed at INR 61,000-68,000/t ($638-711/t). Demand remained weak, restricting buying to need-based requirements.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.58 mm/CTL) inch down by INR 100/t ($1/t) w-o-w to INR 58,600/t ($613/t) as of 26 May against INR 58,700/t ($614/t), a week ago.

However, CRC (IS513, Gr O, 0.9 mm/CTL) prices held stable w-o-w at INR 66,000/t ($690/t) on 26 May. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market update

Trade-level HRC prices remained largely stable during the week ending on 26 May, although “some distributors attempted to push offer prices up marginally in Ludhiana”, sources informed BigMint. However, demand continues to remain subdued, with buying activity restricted primarily to immediate, need-based requirements. Market participants noted that, “end-user consumption has yet to recover meaningfully”, resulting in limited acceptance of higher offers.

The overall market tone remains cautious and weak as industry participants are largely waiting for clearer signs of price stability before resuming active procurement. Meanwhile, a distributor in North informed BigMint, “mills are reportedly focusing on liquidating stockyard inventories to move material in market”. Overall, participants expect demand-side improvement to be the key factor determining the market’s direction in the coming weeks.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 307,885 t as on 22 May. Around 133,411 t of additional cargoes are expected by mid-June.

Export volumes: India’s bulk exports of HRCs touched 141,466 t as on 22 May. Around 69,950 t of additional cargoes are expected to be shipped.

Outlook

India’s flat steel market is expected to remain range-bound over the next 4-5 days amid subdued demand and cautious procurement activity. With buying largely limited to immediate requirements, mills may opt for order rollovers to sustain bookings. Market participants are expected to maintain a wait-and-watch stance until clearer signs of demand recovery emerge as any upward price movement is unlikely to be sustained in the absence of stronger underlying consumption, keeping overall sentiment cautious.

Leave a Reply