- Most Pakistani mills remain shut due to labour shortages during the Eid holidays

- New ship recycling legislation may strengthen Pakistan’s long-term scrap ecosystem

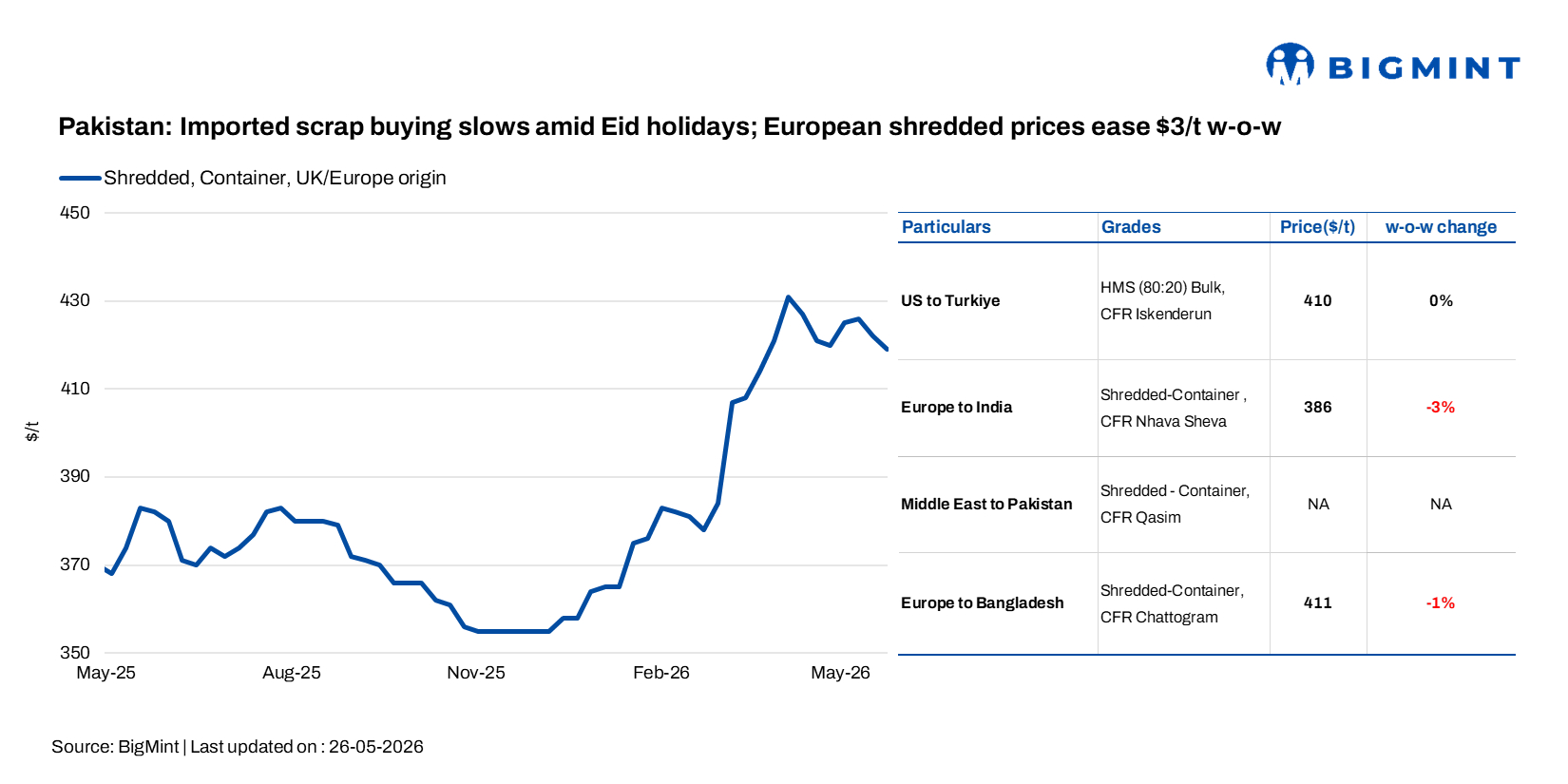

Import ferrous scrap trading activity across Pakistan slowed sharply in the week ending on 26 May as Eid holidays disrupted market operations, while BigMint assessed Europe-origin shredded scrap at around $419/t CFR, inched down $3/t w-o-w.

As per market insiders, Bangladesh and Pakistan markets have turned extremely slow ahead of the Eid break. Pakistan’s domestic market is effectively closed and is expected to remain shut for nearly 7 to 10 days, with almost no transactions taking place.

3 to 4 imported scrap trades were heard during the early part of the second half of last week, including around 1,000 t of UK-origin PNS booked at $440/t CFR Qasim, nearly 500 t of UK-origin shredded scrap traded at $423/t CFR Qasim, and another 500 t of UK-origin skull scrap concluded at $333/t CFR Qasim.

Market Comments

A UK-based recycler commented, “The imported scrap market in Pakistan remained largely inactive as Eid holidays started across the country. Trading activity is very limited, and no major fresh buying inquiries were heard during this period. Imported shredded scrap into Pakistan was indicated at around $415-420/t CFR, but currently there are no fresh offers available in the market.”

A Karachi-based trader said, “Malaysia is currently offering LMS bundles at around $355/t CFR to both Pakistan and India, mainly because freight rates are almost similar at nearly $950/container. Malaysian Turnings are being offered near $330/t CFR, but no deals have been concluded so far.”

Domestic market indicators remained relatively stable, with billet prices heard at PKR 212,000-215,000/t ($762-773/t), Grade 60 rebar at PKR 245,000-250,000/t ($880-898/t), local scrap at PKR 145,000-150,000/t ($521-539/t), and Bala at PKR 190,000-195,000/t ($683-701/t).

Freight pressure weighs on regional imports

Prior to the slowdown, Pakistani buyers remained comparatively active, booking Malaysian busheling at $430-435/t CFR and GI bundles at $355-360/t CFR. Market participants also reported purchases of shredded scrap, LMS, HMS, and Hong Kong-origin bundled HMS cargoes. UK-origin shredded scrap deals were concluded at $425/t CFR during the week, up slightly from previous levels.

Traders noted that vessel space constraints and rising freight rates from Hong Kong are expected to further pressure import economics in the coming weeks. An international trader stated that freight rates on the Hong Kong-Pakistan route are likely to rise further next week due to increasing competition for vessel space.

In contrast, Indian import demand remained subdued as mills increasingly shifted towards domestic scrap and sponge iron amid high imported scrap offers and rupee weakness. An Indian longs producer noted that Indian mills were increasingly blending local scrap and sponge iron instead of relying on imported material, highlighting the continued cost pressure on containerised scrap imports.

Ship recycling reforms may support domestic scrap generation

Meanwhile, Pakistan approved new maritime legislation aligned with the Hong Kong Convention for safe and environmentally compliant ship recycling, supporting the long-term expansion of its shipbreaking industry. The new law introduces mandatory inspections and certification for hazardous materials on ships entering Pakistani recycling yards, while also tightening environmental and worker safety standards. Officials noted that Pakistan already accounts for nearly one-third of global ship recycling activity, making it one of the world’s key shipbreaking hubs.

The government expects shipbreaking activity at Gadani to increase further amid ongoing geopolitical disruptions and changing global trade flows. Earlier estimates suggested nearly 400 ships could potentially move to Pakistani yards for dismantling.

Separately, authorities proposed creating a “steel corridor” linking Karachi shipyard operations with Pakistan Steel Mills (PSM), allowing scrap recovered from shipbreaking activities to support domestic steel production and the potential revival of the idle steel complex.

Outlook

Regional import scrap trading activity is expected to remain weak in the coming days due to Eid holidays, limited buying inquiries, and rising freight uncertainties across Asian routes. Pakistani buyers may return gradually after the holiday break, although higher container freight and firm overseas offers could continue restricting aggressive bookings.

Leave a Reply