- Tuna port inventories surge sharply w-o-w

- Freight volatility impacts import sentiment

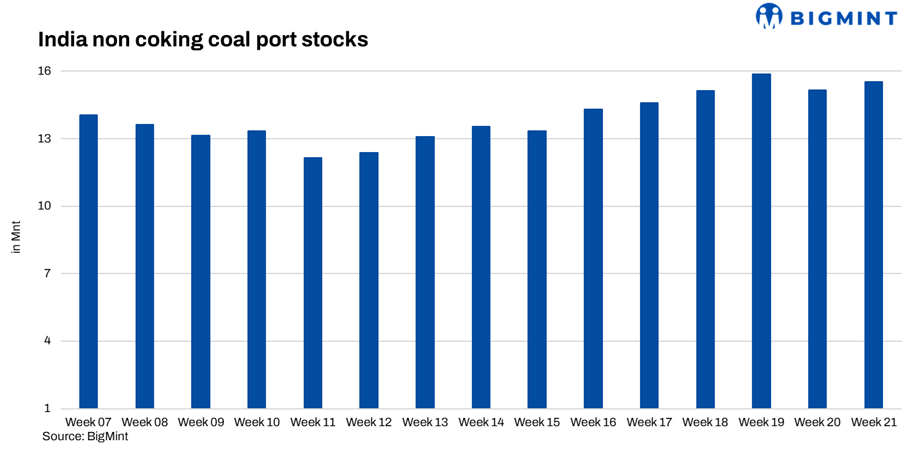

India’s thermal coal inventories at major ports increased 2.4% w-o-w in Week 21 to 15.53 mnt from 15.16 mnt in Week 20, reflecting fresh cargo arrivals at select western ports despite continued weak downstream demand. Market participants stated that overall supply conditions remained comfortable as sponge iron, steel and cement sectors continued limiting aggressive procurement activity ahead of the monsoon season. Buyers largely preferred requirement-based purchases while traders avoided building large inventory positions amid subdued industrial sentiment.

Portside inventories witnessed mixed movement during the week, reflecting selective cargo positioning and uneven regional evacuation trends. Significant stock increases were recorded at Tuna, Kandla, Haldia and Kakinada, indicating fresh arrivals and slower evacuation at some locations. Meanwhile, inventories at Krishnapatnam, Pipavav, Dhamra and Vizag declined, reflecting improved cargo movement and lower inflows at these ports.

Hazira continued holding the highest thermal coal inventory position at 2.43 mnt, increasing 4.7% w-o-w, followed by Mundra at 1.72 mnt, up 8.9%. Paradip inventories declined 5.2% to 1.48 mnt, while Dhamra stocks dropped sharply by 12.7% to 1.13 mnt. Participants stated that inventory movement currently depended more on regional cargo positioning, vessel arrivals and evacuation patterns rather than any meaningful recovery in industrial coal demand.

Buyer-wise inventory positioning remained largely stable during the week, indicating cautious procurement behaviour across major traders and consumers. Adani Enterprise continued holding the largest inventory position at 3.91 mnt, up 3.2% w-o-w, while Agarwal Coal inventories increased marginally by 1.1% to 0.80 mnt.

Imported coal sentiment remains weak

Imported coal market sentiment remained subdued during the week despite firm international coal prices and elevated freight costs. South African coal buyers largely resisted higher landed offers as sponge iron margins stayed under pressure and downstream steel demand remained weak. Buyers from central India were largely absent from the market, while most procurement continued only for immediate operational requirements.

Market participants stated that widening bid-offer disparities continued restricting trade activity across imported coal markets. FOB offers for South African 5,500 NAR coal were heard around $96-97/t, while freight from RBCT to India remained elevated near $22-24/t. However, buyers remained reluctant due to weak finished steel demand and comfortable domestic coal availability.

Indonesian coal sentiment remained comparatively firmer due to tighter cargo availability, strong Chinese demand and uncertainty surrounding proposed export policy reforms. However, Indian buyers continued resisting aggressive spot bookings due to comfortable inventories and cautious downstream demand outlook. Participants stated that imported coal movement may remain slow unless steel and sponge iron demand improves meaningfully over the coming weeks.

Domestic coal keeps market comfortable

Domestic coal availability continued remaining comfortable due to regular CIL auctions and lower premiums in recent SECL and MCL auctions. Market participants stated that weaker sponge iron and steel demand continued limiting fresh procurement interest across regions. Buyers largely restricted purchases to immediate requirements amid expectations of slower industrial activity during the approaching monsoon period.

Domestic coal prices also remained under pressure during the week. BigMint assessed 5,000 GCV coal prices lower by around INR 500/t w-o-w, while 4,500 GCV material declined around INR 200/t to nearly INR 4,100/t. Comfortable domestic supply availability continued reducing urgency for imported coal bookings across key industrial sectors.

Coal alternatives continue influencing demand

US-origin NAPP coal continued attracting cement sector buyers due to better delivered-cost economics compared with imported petcoke. Cement producers increasingly preferred flexible coal blends amid weak cement demand and expectations of softer fuel consumption during the monsoon season. Meanwhile, imported petcoke demand remained subdued as buyers continued favouring cheaper coal alternatives and maintaining cautious procurement strategies.

Outlook

India’s thermal coal market sentiment is expected to remain cautious in the near term amid comfortable inventories, weak sponge iron and steel demand, and sufficient domestic coal supply. Although freight costs and international coal prices may continue supporting imported coal offers, buyers are likely to maintain requirement-based procurement strategies until downstream industrial demand improves meaningfully.

Leave a Reply