- Eid holidays slow fresh imported scrap bookings in Pakistan

- Weak rebar demand limits Turkish deep-sea scrap bookings

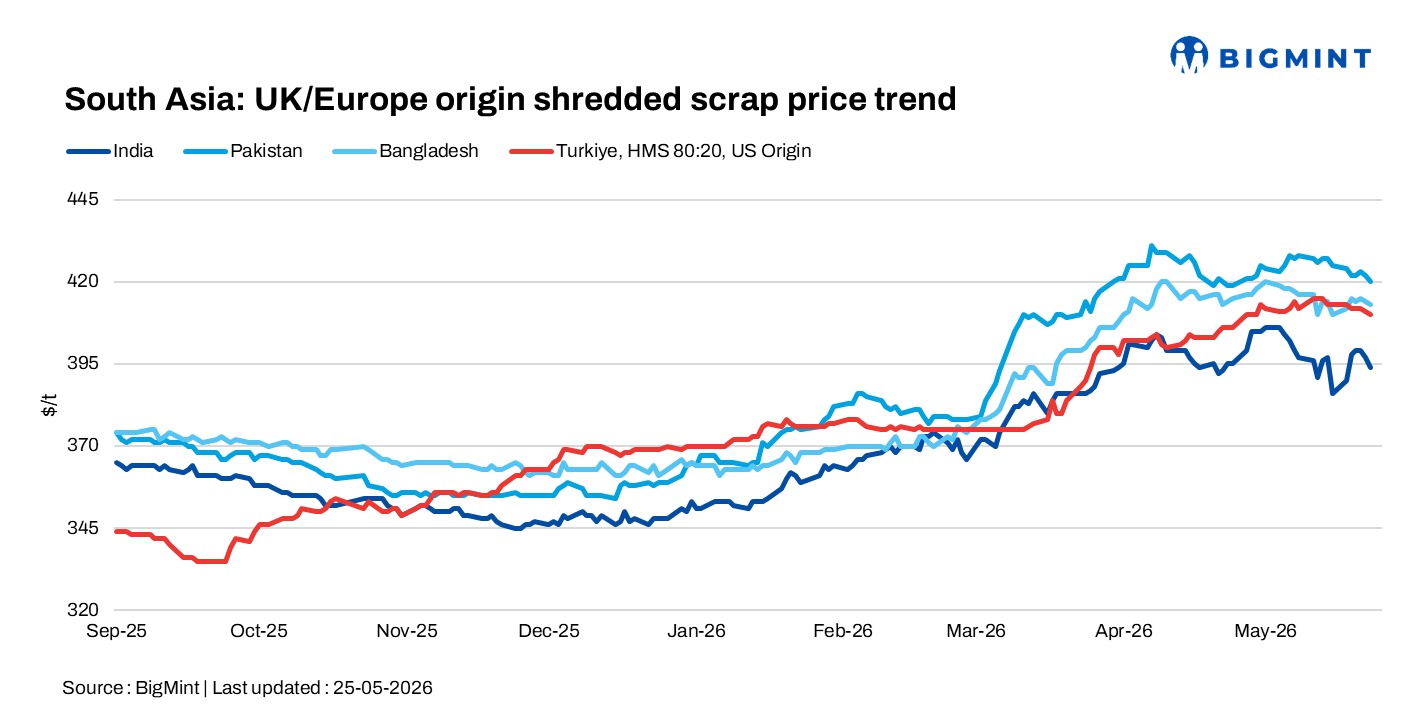

South Asian imported scrap markets remained largely subdued d-o-d on 25 May amid cautious buying sentiment, poor import price viability, and slower activity ahead of Eid holidays. Meanwhile, Turkish deep-sea scrap trade stayed quiet with mills targeting lower price levels amid weak rebar demand and delayed bookings.

India: The imported scrap market remained weak d-o-d, with Indian buyers largely staying away from fresh bookings amid poor import price viability, cost pressure from the depreciation of the rupee, and sluggish steel demand. Market participants noted that buying activity was only taking place selectively in pockets, while HMS prices sharply declined from around $375/t earlier to nearly $335-345/t CFR depending on origin. UK/EU-origin HMS 80:20 offers were heard at around $335/t CFR Nhava Sheva, Mundra, and Chennai, while South Africa-origin turnings were heard near $315/t CFR.

Higher-grade imported scrap offers continued facing resistance, with UK-origin shredded scrap heard at $405-408/t CFR and US-origin shredded offers lower at $400-402/t CFR, typically trading around $5/t below UK-origin cargoes. Meanwhile, US-origin HMS 80:20 bulk offers were heard near $380/t CFR Kandla, while Africa and East-origin LMS offers stood around $320/t CFR and HMS near $340-345/t CFR India.

Pakistan: The imported scrap market remained slow, with trading activity largely halted ahead of the extended Eid holidays as the domestic market is expected to remain closed for nearly 10 days. Market participants noted that no major transactions were heard, while workable shredded scrap indications remained near $415/t CFR. Fresh offers were also limited as the EU and UK markets remained closed, while both the Bangladesh and Pakistan markets stayed extremely slow ahead of the Eid break.

Bangladesh: Bangladesh’s imported scrap market remained largely subdued as buyers preferred domestic feedstock over imports amid geopolitical uncertainty, the depreciation of the taka, and the upcoming Eid slowdown. Active shipbreaking operations and steady sponge iron supplies from West Bengal continued supporting local availability, while imported shredded scrap offers were heard around $410/t CFR, HMS near $385/t CFR, and PNS at $400-405/t CFR Bangladesh.

Turkiye: Deep-sea import scrap prices remained largely stable on 22 May, although trading activity stayed quiet amid limited mill buying interest and delayed bookings. Turkish mills were largely targeting around $400-405/t CFR for US-origin HMS 80:20, while weak domestic and export rebar demand, along with repeated public holidays in Turkiye, continued to slow overall market activity. However, some market participants expect scrap prices to recover after the holidays if mills return simultaneously to secure cargoes.

Leave a Reply